If you know what “bumbershoot” is, you're ahead of thecurve.

|If not, a little background in the difference between InlandMarine and Ocean Marine coverage might be in order, beforeexamining the state of both markets and whether producers mightseek to do more business in them.

|While it's tempting to simply refer to Inland Marine asinsurance solutions for anything transported across brown water andOcean Marine as coverage for that which moves over blue water, thetruth is, these two types of cover are far more complicated.

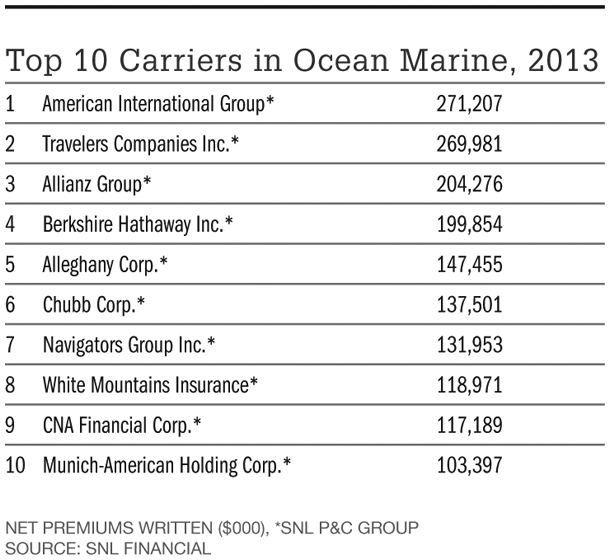

|Broadly speaking, “marine” risks do not lend themselves to beadequately covered under a property policy. Ocean Marine cover,perhaps the world's oldest type of insurance, does includeindemnity for losses that occur primarily on international voyages,but also can cover any losses suffered while goods are a mileoffshore. Ocean Marine overage primarily includes coverage for thevessel or hull of a ship; the cargo; the freight revenue to bereceived by the ship's owner; and legal liability for anynegligence by the shipper or the carrier.

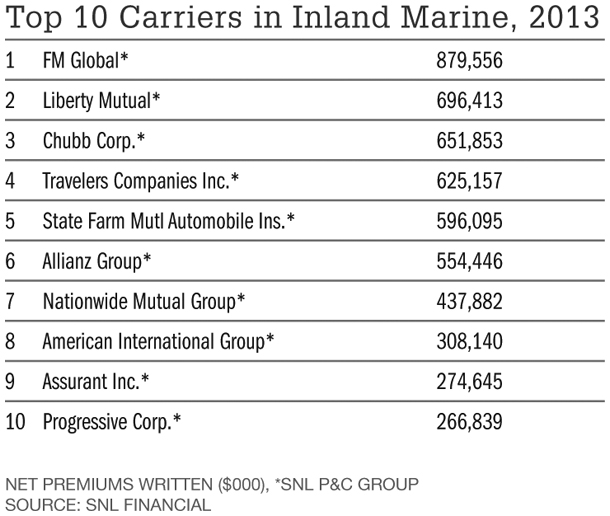

|Inland Marine, meanwhile, includes far more types of cover thanone might expect. These include but are not limited to builders'risk, fine arts, guns, museums, all goods that move on land, motortruck cargo, contractors' equipment, musical instruments, mobilemedical equipment, exhibitions and the like. It's helpful to thinkof Inland Marine risks as property cover for property that is notfixed in one place: If it can be moved, whether it's a crane or adiamond necklace, it's likely to fall under the classification ofInland Marine. Construction and transportation account for thelion's share of Inland premiums (about 60%).

|That said, executives in both lines will tell you there's a lowbarrier for entry (meaning that not as much capital is requiredthan in other types of cover) and there's less regulatory oversightand filing than in other P&C lines. What's more, with a fewnotable exceptions (Superstorm Sandy being one of them), the losshistory for both lines is historically quite good. It's notuncommon for the combined ratio for marine risks to outperform therest of the P&C segment by at least 10 points. It's goodbusiness to write, which attracts many players and a lot ofcapacity—which can make it a tough business at times to get ratein.

|Differentiation in service, therefore, is especially key whenwriting marine risks, along with solutions carefully crafted withthe client. Don Harrell, who heads marine and exploration &production businesses in the U.S. and Latin America for LibertyInternational Underwriters as senior vice president/Marine, citesthree key components vital to his business: claims, engineering andloss control. Continued investment in all three departments, hestresses, is essential.

|“It's a highly specialized and technical line of business,”Harrell says. “You need your claims department to be heavilyinvolved in the process not only to determine how our portfolio istrending, but how we're responding to the customer. You need to beactively involved with clients to give them an extra set of eyes totheir risks.”

|“At the heart of it, [Ocean Marine cover is] a world in whichthe carrier can customize coverage to the customer's needs,” saysBill Queen, president of Ocean Marine for Travelers. The carrier'scargo agency, hull agency and general agents spend a lot of timeexplaining coverage to clients, he says. “In the cargo world, youneed to know where the cargo is going and who's responsible for itat different points. Am I covering it when it gets to dock? On theship? If the ship goes down, what's going to happen to thatproduct? Do you want your customer's product to be scrapped if itgets damaged, or will it be sold off at a discount? The [customer]doesn't want to be surprised when there's a loss.”

|Bigger Vessels, Greater Exposure

| Losses in the Ocean Marine segment of latehave been driven by the emergence of much larger cargo vessels thanever before. Triple-E cargo ships (the largest in the world) cancarry as many as 18,000 containers, at insured cargo values of upto $2 billion—and when one of those vessels sinks, the potentialfor loss is significant. The MOL Comfort container ship, forexample, racked up an estimated $300 to $400 million in claims lastyear when it cracked in two and sank off the coast of Yemen.

Losses in the Ocean Marine segment of latehave been driven by the emergence of much larger cargo vessels thanever before. Triple-E cargo ships (the largest in the world) cancarry as many as 18,000 containers, at insured cargo values of upto $2 billion—and when one of those vessels sinks, the potentialfor loss is significant. The MOL Comfort container ship, forexample, racked up an estimated $300 to $400 million in claims lastyear when it cracked in two and sank off the coast of Yemen.

“The complexities in costs there have a huge impact on thefinancials and balance sheets, but also from a claims-handlingperspective when you're dealing with a loss in internationalwaters,” says Patrick Hickey, senior vice president, Ocean Marineportfolio leader for Zurich Global Corporate in North America.

|“Exposures continue to grow with vessel size,” agrees RichDeSimone, president of North America Ocean and Inland Marine forXL, citing examples such as the Mary Maersk, a huge cargo ship thatdeparted Algeciras, Spain, on July 21 with a world-record cargo of17,603 twenty-foot equivalent units—the most ever carried by asingle vessel.

|While frequency may be down in the number of incidents, he adds,the severity of maritime accidents like the wreck of the CostaConcordia and a federal judge's recent ruling that oil giant BP Plcwas “grossly negligent” for its role in the 2010 Deepwater Horizonspill in the Gulf of Mexico illustrate the severity of theaccidents that do happen.

|According to AllianzGlobal Corporate & Specialty SE's (AGCS) second annualSafety and Shipping Review 2014, which analyzes reportedshipping losses of over 100 gross tons, more than a third of 2013'stotal losses were concentrated in two maritime regions. The SouthChina, Indo China, Indonesia and Philippines regions saw thehighest number of losses (18 ships), followed by the seas aroundJapan, Korea and North China (17 ships).

| Which is concerning, given that goods producedin Asia are so critical to many U.S. supply chains. “The globaleconomy has changed how we view the exposures as underwriters,”says Kevin Wolfe, Allianz's marine regional head for the Northeast.These days, he explains, it's far more top-of-mind for U.S.manufacturers to have insurance solutions in place for keysuppliers in the Far East or Africa: “Now they want to know whathappens if a supplier has an explosion, and business is lostbecause goods won't reach customers.”

Which is concerning, given that goods producedin Asia are so critical to many U.S. supply chains. “The globaleconomy has changed how we view the exposures as underwriters,”says Kevin Wolfe, Allianz's marine regional head for the Northeast.These days, he explains, it's far more top-of-mind for U.S.manufacturers to have insurance solutions in place for keysuppliers in the Far East or Africa: “Now they want to know whathappens if a supplier has an explosion, and business is lostbecause goods won't reach customers.”

Wolfe concurs that larger vessels are a concern for insurers.“As container ships get larger, the values are jumping almostexponentially,” he says. “On normal container ships, you have anidea as an insurance carrier what the exposure is, but with largerships that's more difficult to determine.”

|Indeed, one of the biggest challenges in underwriting OceanMarine, some executives say, is the limited amount of loss dataavailable. Port aggregations are hard to measure, DeSimone says, asthere's less collecting and sharing of data captured. As such, attimes it's virtually impossible for certain underwriters todetermine what their precise exposures are in a given area.

|The challenge is there's not enough claims data on any onecompany to predict exactly how the business is performing, Harrelladds. Bill Queen at Travelers agrees: “There's no one body thatcollects that data,” he noted, adding that with less claims data togo on than in other lines, “gut underwriting” often figures intothe equation.

|Construction Concerns, Cargo Theft

| The current story in Inland Marine, meanwhile,mirrors the economy in that construction is on the upswing, withmore projects in motion than in previous years and previouslystalled sites humming again. Yet with that growth come some growingpains, says Joe Tracy, president of Inland Marine forTravelers.

The current story in Inland Marine, meanwhile,mirrors the economy in that construction is on the upswing, withmore projects in motion than in previous years and previouslystalled sites humming again. Yet with that growth come some growingpains, says Joe Tracy, president of Inland Marine forTravelers.

“Is there enough skilled labor for those projects?” he asks.“Can construction forms keep current with changes in constructionmethods?” What's more, he points out, there are more fixtures beinginstalled in buildings and houses than ever before, and lot moreplastic tubing is being used in place of more expensive materialslike copper or pipe. “Those new materials can impact the building;what's the life cycle of those products?” he ponders. “We don'tknow the answers, as that's still evolving.”

|Building to green standards is another complicated discussionbeing had around various construction projects, says Bob Opitz,worldwide Inland Marine manager for the Chubb Group of InsuranceCos. The valuation of some new structures, he explains, includesadditional expenses that go into obtaining green certification;with a construction project, that can include such issues on sitesas segregation of waste and waste removal, and highly specificsourcing of green-certified wood and other materials. Violation of,or errors made in, any of those endeavors can lead to defaults.

|The handling of construction claims, says Tracy, has changed:Generalists cannot handle those claims, as costs can quicklyescalate. Expertise among those who specialize in Builders' Riskmust be brought to the table, both in claims handling and generalclient service. The difference between the men and the boys, hesays, lies in “how you deliver the expertise. It has to betangible. It has to be real. You develop as custom a product as youcan to address coverage needs, and then do what you can to decrease[the client's] loss history and severity.”

|Truckers, for example, are moving more goods than ever, Tracypoints out. Travelers' “sting trailer” is often employed in workingwith local law enforcement to counter hijackings and theft incertain areas of the country (see sidebar). High concentrations ofgoods being transported on land, especially aboard trucks, canspell greater losses if a load vanishes in transit.

|Hickey at Zurich notes that cybercrime has extended to thetrucking space via thieves who obtain information on when goods areto be moved, intercept the load, and make off with it. “A criminalposes as a trucker and takes data off a truck board, shows up at alocation with falsified info and steals the cargo without everhaving to lift a gun,” he says. “The full scope of those risks isnot always contemplated when [clients] are looking at theirforecasts. But it very much should be.”

|Producer Opportunity: Existing Clients' MarineNeeds

|There's good news for those agents and brokers looking to breakinto Inland and Ocean Marine: Many of your existing clients havecoverage needs in those lines that you're probably not aware of orpreviously haven't considered.

|“Every single agent, I don't care if you're a storefront agencyor otherwise, has some kind of Inland and Ocean Marine exposureamong their clients,” says Rich DeSimone at XL. “Every one of themhas someone having something built, or who are moving goods frompoint A to point B. It's a matter of developing a sensitivity tothat,” he adds. “Otherwise, someone else is going to get in on thatbusiness.”

|Kevin Wolfe at Allianz offers similar advice, suggesting thatproducers take a closer look at their current list of insureds.“They would probably find more opportunities from existingclients,” he says. “Transportation exposure is a big one thatclients miss. All they have to do is ask their clients how theyinsure their goods in transit.

|“Most marine insurance companies' underwriters are more thancapable of working with brokers and taking them through theprocess. There's a big opportunity for brokers to increase marinebusiness, and I think they should.”

|“Most of the people in this industry come from a maritimebackground, and they have a language that's unique to thatenvironment,” notes Queen at Travelers. He suggests that agentsinquire through their middle-market reps about instructionalclasses offered by carriers, through which they learn some of thelingo involved. “Recognize that the laws and language and jargonare different in Ocean, but experts can help with that,” he says.For example, he adds, “Bumbershoot is marine umbrella.

|“On day one, it's very difficult to learn that jargon. Don't beintimidated by that. Get an expert to help you; that's the key. Youcan learn it, but it takes time to get credibility on the sea.”

|Busted! The “Sting Trailer”

| Travelers recently learned of a new cargotheft ring operating between Pennsylvania and New Jersey that poseda threat to one of its clients in the area. In response, Travelersoffered the Pennsylvania State Police Auto Theft Task Force Central(CATFF) the use of its “sting trailer” to help catch the gang.

Travelers recently learned of a new cargotheft ring operating between Pennsylvania and New Jersey that poseda threat to one of its clients in the area. In response, Travelersoffered the Pennsylvania State Police Auto Theft Task Force Central(CATFF) the use of its “sting trailer” to help catch the gang.

The trailer was loaded with consumer electronics and parked at atruck stop near Harrisburg, where it was monitored by officers withCATTFF. The trailer was stolen within 24 hours and was escorted toNew Jersey by an accomplice driving an SUV, where the it was thenparked in a lot of a big box store. The subjects, both of whom werearrested by the New Jersey State Police, had extensive criminalhistories.

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- All PropertyCasualty360.com news coverage, best practices, and in-depth analysis.

- Educational webcasts, resources from industry leaders, and informative newsletters.

- Other award-winning websites including BenefitsPRO.com and ThinkAdvisor.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.