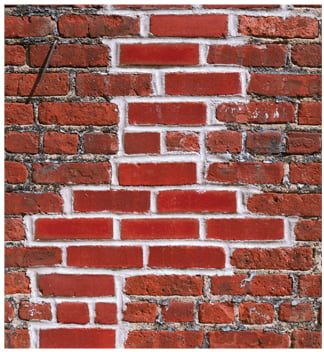

One of the most common questions I receive regards matching. Typically what happens is there is a loss on the premises that affects a portion of the roof, carpeting, flooring, siding, or other material, and the carrier wants to replace only the damaged section. This is acceptable if matching components can be found. However, it is not uncommon for that particular type of shingle or carpeting to be discontinued so an exact or even close match is unable to be made.

One of the most common questions I receive regards matching. Typically what happens is there is a loss on the premises that affects a portion of the roof, carpeting, flooring, siding, or other material, and the carrier wants to replace only the damaged section. This is acceptable if matching components can be found. However, it is not uncommon for that particular type of shingle or carpeting to be discontinued so an exact or even close match is unable to be made.

Often the carrier wants only to replace the damaged section of roof or carpeting, while the insured wants to be restored to what he or she had before—namely, a matching roof or carpet. The carrier bases its argument on a few sections of policy language. The first is under Section I: Perils Insured Against, where the policy states that "we insure against direct physical loss." The second part of language is under the loss-settlement section of the ISO homeowners' policy, where it refers to "that part of the damaged building." Certain carriers maintain that these two sections of language indicate that only the damaged portion needs to be replaced, thereby excluding any undamaged portions that would make the property match.

Settlement OptionsAnother section of language in the loss-settlement options is where the policy pays the lesser amount of policy limits—either the amount actually spent to repair or replace the property, or the replacement cost of that part of the building damaged with material of like kind or quality. Again, carriers use this section to pay for only the damaged portion of the building. However, the like kind and quality statement does present an issue. For instance, if the type of shingles or carpet is no longer available, then it is impossible to replace just the damaged section with "like kind and quality."

Recommended For You

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Breaking insurance news and analysis, on-site and via our newsletters and custom alerts

- Weekly Insurance Speak podcast featuring exclusive interviews with industry leaders

- Educational webcasts, white papers, and ebooks from industry thought leaders

- Critical converage of the employee benefits and financial advisory markets on our other ALM sites, BenefitsPRO and ThinkAdvisor

Already have an account? Sign In Now

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.