The ads are enticing: “Make $35/hour driving with us!” or“You could make $800 a week or more!”

|Ridesharing services, or transportation network companies(TNCs), are everywhere. Uber alone signs up an estimated 20,000 drivers each month worldwide. The service isparticularly popular with millennials who appreciate the lowertransportation costs and how easy it is to use the app from theirphones.

|You have a nice car and could use extra cash. You sign up to bea driver, install the app and soon you are driving people aroundand making money. Is it too good to be true?

|Not if you consider these five factors before driving into thepassenger service frenzy.

||

Photo: Mahathir MohdYasin/Shutterstock

|1) It isn’t “ridesharing”

|The term “ridesharing” is a misnomer. Ridesharing is “the act oran instance of sharing motor vehicle transportation with another orothers, especially among commuters,” which sounds more likecarpooling. This arrangement doesn’t involve a fee or contract.

|TNCs use apps to connect a driver with a passenger for a fee.This is one definition of “livery.” Livery or for-hire companiestypically charge a fee and some sort of employment contract existsbetween the company and driver.

|The definitions and usage of a personal vehicle are importantwhen determining insurance coverage and even more important in theevent of an accident.

|On December 31, 2013, six-year-old Sofia Liu, her mother and herbrother were crossing the street in San Francisco when SyedMuzzafar struck them in a crosswalk, killing Sofia. Muzzafaridentified himself as an Uber driver and indicated that he wasdriving around awaiting a new transaction when the accidentoccurred.

|Uber released a statement saying that the driver was “not providing services onthe system at the time of the incident.” A $20 million wrongfuldeath suit was filed by the family of Sofia Liu, naming Uber andMuzzafar as defendants. In a legal filing in May 2014, the company denied coverageunder their own liability policy since the driver wasn’t engaged ina transaction at the time of the accident. It is unclear whetherMuzzafar’s personal insurance has also denied coverage.

||

Photo: alexskopje/Shutterstock

|2) How much does TNC coverage reallyprotect?

|According to most TNCs, automobile liability insurance coverageis offered to drivers. Coverage carried by TNCs may change without notice.

|As a driver, these policies allegedly become your insurancepolicies from the moment you get a fare until the transaction isclosed, where coverage presumably reverts back to your personalauto insurance policy.

|What does your personal auto insurance carrier say aboutthis?

|Related: Uh oh…Uber has some coverage issues

||

Photo: Itan1409/Shutterstock

|3) Your own insurance probably won’t protectyou

|TNCs require that drivers provide license, registration, and acopy of a current personal auto insurance policy. Some TNCs requirebackground checks while others don’t. You may believe yourinsurance policy offers some protection while you are working for aridesharing service. This is usually not the case.

|Typical personal automobile liability policies exclude coveragefor business conducted via personal vehicle.

|Most insurance companies now include an additional questionduring the application or renewal process: Are you currentlyworking with, or have you in the past worked with any ridesharingservices?

|The best way to know if your insurance carrier covers you whileyou are working is to ask your agent, preferably before you sign upwith a TNC.

||

Photo: R Images/Shutterstock

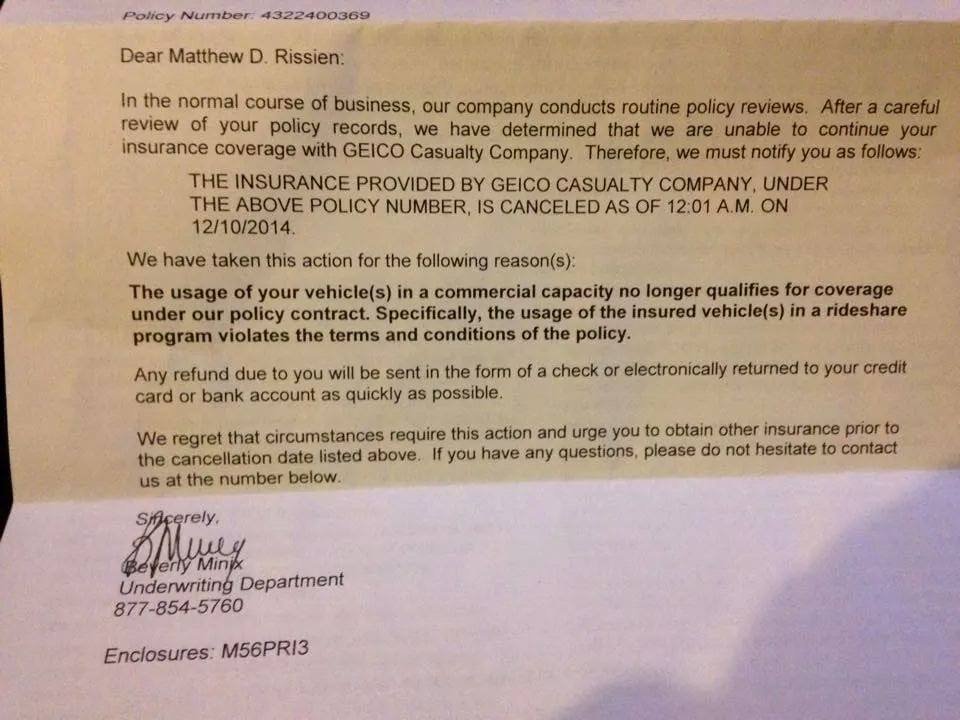

|4) Don’t ask, don’t tell

|Last fall on a rideshare driver forum a user asked: “Does your insurancecompany know you Uber?” The answer was a resounding “no!”

|An Uber driver posted a video of himselfcalling his insurance carrier to find out if the company wouldcancel a driver if they found out he was working for a TNC. Theagent said these matters were handled on a case-by-case basis, butmay be referred to a commercial auto insurance company forcoverage. The driver’s advice? “Don’t tell them.”

|Don’t ask, don’t tell just might work if you don’t have anaccident. If you do, you could lose your personal auto policycoverage for several reasons:

- Failure to disclose. Nearly every autoinsurance application includes a warranty just above the applicantsignature line that reads similar to this: “I/We understand andagree that any misstatement of warranty or fact on thisapplication shall be considered a violation of coverage affordedunder any policy issued on the basis of thisapplication. I/We understand and agree that thisapplication shall form part of any policy issued.” If you answer“no” when the truth is “yes,” this is material misrepresentation.

- Usage is important. When applying for autoinsurance, your agent will ask how many miles driven per month andthe usage of your vehicle. Driving for a TNC changes not only theusage description of your vehicle, but also your exposure toaccidents. Driving back and forth to work is significantly lessexposure than driving around town for fares all day.

The possibility of having your coverage cancelled by yourpersonal auto insurance carrier is real. TNC drivers have providedevidence of coverage being cancelled due to business usage of their personal vehicle forrideshares.

||

Photo: MarynaPleshkun/Shutterstock

|5) Make money or lose your shirt?

|Inc.com did research on the time and effort required to earn a living wage working for a ridesharing service. Theyfound that once you factored in insurance, fuel and maintenancecharges, it takes a lot of rides to earn a solid wage.

|But these costs don’t take accidents into consideration. Anaccident while driving for a ridesharing company can reach deepinto your wallet.

|You are a rideshare driver. You have a fare and are involved inan accident. The $1,000,000 company liability policy pays thedamage to the other vehicle and the medical bills for yourpassenger. Consider these scenarios:

- The damage to the other vehicle as well as the damage to thepassenger’s belongings and the passenger’s medical bills exceed$1,000,000 (as in the case of Mr. Muzzafar). You are on thehook for anything exceeding the $1,000,000 threshold. Your personalauto policy will likely deny coverage under the no passengers for afee exclusion (and cancel your policy).

- Your vehicle is badly damaged in the accident. The TNC offersphysical damage coverage for your vehicle, but usually only afteryour personal auto policy denies the claim (and cancels yourpolicy).

- You are badly injured in the accident. Because you are a 1099contract employee, there is no workers’ compensation policy tocover injury or disability. You are responsible for purchasingdisability and/or life insurance on your own, as well as a medicalinsurance policy that covers you while on the job, many don’t.Failure to carry correct medical insurance coverage means yourmedical bills come out of your pocket.

- Your injury and the injury for your passenger(s) may notqualify for the Personal Injury Protection (PIP) portion of yourpolicy (if applicable), since the coverage is excluded.

Aside from medical bills and lost wages, an accident can havelarge financial consequences. Replacing cancelled coveragecan be difficult and expensive with increased premiums lastingyears into the future. These costs should be considered whendetermining how much you can really make.

|Related: Insurance requirements may be on the way for ridesharing companiesin Florida

||

Photo: Maridav/Shutterstock

|To drive or not to drive?

|There are many pending insurance issues involving TNCs.California (among other states) as well as Germany, Thailand andother countries have issued cease and desist orders based onsituations where TNCs have avoided taking responsibility for casesthat involved injury, rape and death.

|TNCs have positioned themselves as transportation disruptors taking advantage of the sharing economy. Local andstate governments are scrambling to determine how to regulate these businesses.

|The insurance industry is also trying to catch up, but in themeantime there are huge gaps in coverage for TNC drivers. Until ahybrid or multi-use policy rolls out nationwide, drivers risk theirpersonal auto insurance coverage and financial ruin well into theirfuture every time they pick up a passenger.

|TNCs haven’t yet taken responsibility for insurance in certaincases of serious injury, rape or death. The sharing economy isstill in its infancy and changing every day. Current andprospective TNC drivers must be wary of the assumption that thesecompanies provide coverage.

|You may wonder how much you could make as a driver, but how muchcan you afford to lose?

|Galen Hayes is president of Hayes Insurance,which focuses on hard to place risks and is a full-servicecommercial insurance brokerage and risk management firm, servingclients across the country by providing access to over 200insurance carriers.

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- All PropertyCasualty360.com news coverage, best practices, and in-depth analysis.

- Educational webcasts, resources from industry leaders, and informative newsletters.

- Other award-winning websites including BenefitsPRO.com and ThinkAdvisor.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

{kind=link}