Editor's Note: This article has been contributed byChristopher Tidball, an executive claims consultant, speaker andauthor of multiple books.

Editor's Note: This article has been contributed byChristopher Tidball, an executive claims consultant, speaker andauthor of multiple books.

We see it time and time again: Stacks of papers piling up onclaims adjusters' desks in the form of bodily injury (BI) demandsfrom attorneys for injuries supposedly sustained as the result ofan auto accident. Of course, the attorney's client is never atfault, and most certainly the alleged injuries are always theresult of your insured's negligence. Sound familiar?

|Like a game of cat and mouse, some attorneys will try to takeadvantage of busy adjusters to maximize settlements for theirclients, at times garnering far more than the claim may actually beworth. It should be said, however, that the tables can be turned,as attorneys are equally as busy, often necessitating the use ofassociates, or negotiators, to push through an even greater volumeof work. Fortunately, this latter bit of information can be ofinvaluable assistance when evaluating and negotiating injuryclaims.

|The truth of the matter is that attorneys get paid based uponhow much they collect. Their contingency fee is often one third ofthe settlement value, and perhaps 40 percent if a lawsuit is filed.The same cannot be said of adjusters, whose obligation is toconduct a thorough investigation in order to arrive at a fair valuebased upon the facts and evidence presented. Herein lies thechallenge for organizations trying to intersect accuracy withperfection.

|Core Claims Skills

As is so often thecase, success stems from a fundamental execution of basic blockingand tackling of claims skills. While there are many importantaspects to a claims investigation, the two most critical areliability and damages, as the claim would not exist withoutboth.

Liability – Which driver was at-fault for theaccident? There are only three possible outcomes: a.) the insuredwas at fault; b.) another party was at fault; or c.) there was shared fault among two or more parties. Far too oftenclaims adjusters select either option “A” or “B.” Meanwhile juries,more often than not, choose “C” and apportion liabilityaccordingly.

|Damages – What were the economic andnon-economic losses from the accident? Again, there are threepossible outcomes:

- There are damages and they are related to the accident.

- There are no damages.

- There are damages, but some or all of them are unrelated to theaccident.

Like liability, the path of least resistance often yieldsthe wrong answer, as claimed injuries are not always related to theaccident. The challenge to insurers is ensuring that both liabilityand damages are investigated concurrently. Commonly one or both areeither overlooked or incomplete, thereby adversely impactingoutcomes.

Like liability, the path of least resistance often yieldsthe wrong answer, as claimed injuries are not always related to theaccident. The challenge to insurers is ensuring that both liabilityand damages are investigated concurrently. Commonly one or both areeither overlooked or incomplete, thereby adversely impactingoutcomes.

Consider that, on average, comparative negligence by insurers nationwide is assessed onsomewhere between 3 and 5 percent of all claims. Let's alsoconsider the fact that research on jury verdicts indicates thataround 55 percent of all claims adjudicated involve scenarios otherthan clear liability. These may include intersection accidents,sideswipes, slip-and-fall accidents, and liquor liability. In otherwords, myriad opportunities exist to improve basic blocking andtackling skills in the comparative negligence arena.

|Prudent Investigations

Inaddition to liability, there are immense opportunities forimproving the accuracy and efficiency of claims investigations,evaluations, and negotiation strategies. At the outset of anyclaim, all involved parties should be contacted, including thosewho are claiming injury. If they are represented, then a requestfor a statement should be made through legal counsel, even thoughthe request may not be granted. It is an important aspect of claimshandling to document when and why this request was made. Theattorney needs to understand early on that you have an obligationto thoroughly investigate injury causation as well as the frequencyand duration of treatment.

There should be due diligence regarding the mechanism forinjury, as well as a thorough investigation of potentialpre-existing conditions or intervening causes. Index information,hospital checks, and public records searches provide a wealth ofinformation, as do friends, neighbors, witnesses, and particularlyex-spouses. Taking the time to seek out those who may be able toshed light on the existence of pre-existing conditions orintervening causes can prove invaluable in settlement negotiations,arbitration, or litigation. Most importantly, this doesn't need tobe burdensome on adjusters who rely on networks of key businesspartners to do the heavy lifting.

|Quantifying BodilyInjury

Another keycomponent of the BI demand are the medical specials, which may beinflated, and at times, unrelated, to the claim. Justbecause the attorney says it is so, doesn't make it so. In manyinstances, there are varying degrees of subjectivity in findings.There are also numerous opportunities for billing errors, or evenworse, intentional billing fraud. Claims adjusters today realizethere is a high probability that medical bills contained in a BIdemand are upcoded or unbundled. It is also possible there are issuespertaining to causation, duration, and frequency of treatment.

While adjusters generally aren't medical professionals, they dohave the requisite training to identify questionable billingpractices or treatment patterns. Thus it is the job of the adjusterto identify these issues and raise questions, often documented withthe assistance of third-party medical billing review software, suchas Mitchell International's DecisionPoint, to identify potentialfraud, billing errors or improper edits.

|By further leveraging medical experts or those fluent in billingand coding, a tremendous amount of medical inflation could beavoided. By coupling this knowledge with proper liabilityassessment, the benefit to the insurers and the consumer issignificant. Furthermore, by paying the right amount, insurersimmediately gain a tremendous competitive advantage in anincreasingly challenging marketplace.

|When the BI demand is received, the adjuster should review allcontents to ensure that they include the necessary documentation tocomplete the injury evaluation. There should also be anotation of any time limit demand requirements with the appropriateaction taken to ensure a timely response. Generally, thisrequirement is met by either tendering an offer (when warranted) ornotifying the attorney, in writing, of additional documentationnecessary to complete the injury evaluation.

|10 Pieces of Critical Information

Whenreviewing the bodily injury demand, it is important to look at avariety of critical information:

- The police report. Was there any mention ofany injury at the scene? Was the injured party transported to amedical facility? Was there any mention of contributing factorsagainst the claimant? Were any witnesses identified?

- Vehicle photographs (auto claims). Does thedamage match? Are there paint transfers? What is the directionalforce of impact? Is the damage such that the injury being claimedmay be related?

- The accident scene. Are there any otherpotential tortfeasors? Overgrown bushes, signal outages, missing orblocked signage, absentee third parties, and similar factors shouldalways be investigated.

- Emergency room records. What was said to theEMT's at the scene and during transport? What does the ER admissionstatement say? What type of pain was related to thetreating physician? Was there a mention of symptoms other than whatmay be related to the accident? Is there any indication of drug oralcohol usage that may have contributed to the loss?

- Medical treatment patterns. How soon didtreatment begin? Were there gaps in treatment? Was treatmentprovided on evenings and/or weekends? Were you able to verifytreating physician office hours?

- Provider type. Was the claimant seen by achiropractor or medical doctor? If the latter, then what was his orher specialty, such as neurology, orthopedics, and so on? What arethe medical professional's credentials? Is his or her licensurecurrent? Are there any prior or pending disciplinary actions withthe current state, or in prior states?

- The duration and frequency. When did treatmentstart? How long did it last? Was it active or passive? Was itlonger than an anticipated expected recovery date among the generalpopulation for a similar complaint?

- Objectivity. Where there objective findings,such as those from an x-ray, MRI, or CT scan? Were the records andfilms obtained and reviewed by an independent medicalexpert?

- Pain management. Did the doctor prescribemedication to ease the complaints of pain? If so, then what type(analgesics, prescriptions, injections)?

- SOAP notes. Does the treatment being providedand billed match the medical providers SOAP (subjective, objective,assessment, plan) notes which can be a great indicator of not onlywhat treatment really occurred, but also a red flag for CPT codingand modifier abuse.

While just touching on some of the key components of the properinvestigation, it becomes easier to visualize just how complex therole of the casualty adjuster can be. However, the BI evaluation isjust part of the equation, as there must be an effectivenegotiation strategy to bring the claim to closure.

|The job of the adjuster is to recognizeimpediments to the case being presented. For example, if theclaimant is saying his or her lower back hurts but they weresideswiped, where is the mechanism for injury? Similarly, be sureto look for red flags, such as a claimant stating he or she was“rear-ended yet thrown forward,” thereby defying the laws ofphysics.

|It is this attention to detail that allows for a case to bebuilt to most accurately support and settle the pending claim. Byfurther leveraging tools to identify potential fraud or billing errors, the adjuster notonly increases productivity but also gathers the proof necessary tosupport contentions gathered during the investigativephase.

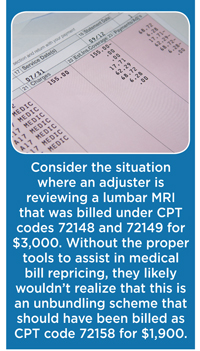

|Consider the situation where an adjuster is reviewing a lumbarMRI that was billed under CPT codes 72148 and 72149 for $3,000.Without the proper tools to assist in medical bill repricing, theylikely wouldn't realize that this is an unbundling scheme thatshould have been billed as CPT code 72158 for $1,900.

|A further review of the medical records may show CPT codesbilled as multiple regions, yet the SOAP notes indicate only oneregion. This is a red flag for upcoding. Or, perhaps a modifier of“93” was used, which denotes interpreter services. Who is theinterpreter, and why were they needed? This is another basicquestion that should be asked but is too often overlooked duringthe course of the BI evaluation.

|According to the office of the inspector general (OIG),modifiers 25 and 59 are used improperly more than 40 percent of thetime, resulting in significant medical inflation. Modifier 59 isused to distinguish procedures that are not normally reportedtogether, while modifier 25 identifies significant, separatelyidentifiable evaluation and management services conducted on thesame day.

|In some instances, the modifiers are used as a provider solutionto get bills paid. However, it is important to recognize thatimprover usage can be considered abusive and can amount tofraudulent billing at times. Again, knowledge of coding is criticalto identify bundling and unbundling scenarios.

|When performed properly, BI claims investigations, evaluations,and settlements require significant amount of time, knowledge, andexpertise. They require painstaking attention to detail and afundamental understanding of biomechanics, medicine and medicalbill coding. The most effective BI reviews incorporate a variety ofprocesses to leverage the expertise of others with a higher degreeof proficiency in these same areas. This in turn bolsters theadjuster's case while dramatically improving outcome accuracy. Theresult is an optimized process that increases productivity whilereducing severities, a benefit for carrier and consumeralike.

|In the end there is a quantifiable correlation to best-in-classservice, quality, and optimal outcomes that separate theextraordinary from the ordinary.

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- All PropertyCasualty360.com news coverage, best practices, and in-depth analysis.

- Educational webcasts, resources from industry leaders, and informative newsletters.

- Other award-winning websites including BenefitsPRO.com and ThinkAdvisor.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.