The recent growth spurt among captives opting to domiciledomestically can be attributed to lower establishment costs, morestreamlined capitalization requirements and state governmentsoffering increasingly creative incentives.

|Another factor: more location options. The Captive InsuranceCompanies Association (CICA) reports that Florida and New Jerseywill be the newest states open for business, effective thisJuly.

| The Vermont insurance market—oneof the oldest in the U.S.—is still the No. 1 domicile in thecountry with 30-40 percent of Fortune 500 companies owninga captive in the Green Mountain State. But other states are takingsteps to make themselves more attractive and to catch up.

The Vermont insurance market—oneof the oldest in the U.S.—is still the No. 1 domicile in thecountry with 30-40 percent of Fortune 500 companies owninga captive in the Green Mountain State. But other states are takingsteps to make themselves more attractive and to catch up.

These efforts are beginning to pay off. Utah, Kentucky, Montanaand Delaware, for example, have each experienced double-digitgrowth in business between 2010 and 2011, according to CICA's lastdomestic industry report.

|Oregon is allotting a portion of its budget to hire 18 captiveregulators; South Carolina's Insurance Funding Program is helpingthe state's Jobs-Economic Development Authority financespecial-purpose captives through state-controlled surplus bonds;and Nevada is reducing compliance expenses by simplifying insurers'applications and reporting processes.

|Newcomer Florida is promoting a simplified and low-costapplication process to encourage captive formation and woo thoseseeking re-domestication. Gov. Rick Scott recently signed a lawallowing single-parent, special-purpose, industrial and captivereinsurance companies to exist within the state. Licensees must paya $1,500 application and $1,000 annual renewal fee. Oregon, anotherdomestic newbie, requires a $5,000 annual fee in place of premiumtaxes.

|Other states are trying to stand out by offering niches for suchrisk-retention groups as those dealing in Cyber Liability or HealthCare.

|In 2011, Maine revived its captives market and became a havenfor Workers' Compensation when it became the first state to allowcaptives to offer health insurance—an increasingly popular positionas the health-care bill pushes companies to offer specializedwellness programs.

|ECONOMIC ADVANTAGES SWEETEN THE POT

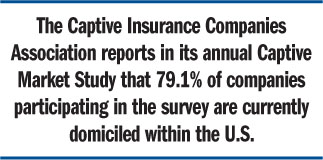

|In the last decade, this shift by states to a morecaptive-friendly environment has spurred 52 percent of new captivesto choose a U.S. jurisdiction as their domicile, whereas between1991 and 2000, only 35 percent of captives were domestic, accordingto Marsh's 2012 Captive Benchmarking Report.

|“States view captives as a way to keep their fingers on thepulse of business formation,” says Arthur Koritzinsky,  Marsh's North American captiveadvisory leader.

Marsh's North American captiveadvisory leader.

Updates about state efforts to fertilize captive formation arecropping up in real time on Web sites such as CICA's, and agenciessuch as Marsh annually monitor the captives industry in surveyswhich are readily available online. The State of Vermont even hasan interactive questionnaire available online offering direct helpfor businesspeople seeking a tailored consultation for a potentialcaptives business.

|“With Internet visibility, industry pressure and sales pressurecoming from state regulators, it's no shock that I'm predicting10,000 captives to exist within the next three years,” says AndrewBarile, an insurance consultant and author of two publications onthe worldwide captives market (see p. 34).

|“One of the issues driving the captives marketright now is that you don't have to be a salesman to sell theconcept [to companies],” he continues. “And all the states nowrecognize that it's a great source of revenue, and they can makemoney off of captives through fees and premium taxes.”

| For his part, Koritzinskyidentifies a couple of reasons why the practice of domiciling inthe U.S. is gaining popularity. “Firstly, income-tax rules forcaptives owned by U.S. companies are largely the same now whetheronshore or offshore.

For his part, Koritzinskyidentifies a couple of reasons why the practice of domiciling inthe U.S. is gaining popularity. “Firstly, income-tax rules forcaptives owned by U.S. companies are largely the same now whetheronshore or offshore.

“And when a new captive market opens up,” Koritzinsky continues,“there are businesses within that state willing to keep theircaptives close.”

|Another factor helping to encourage domestic captives is theNonadmitted and Reinsurance Reform Act of 2010, which helpsin-state companies reduce their procurement taxes. Small captivesmust elect to be U.S. taxpayers in order to take advantage of thewealth-accumulation options and tax benefits allotted them by theInternal Revenue Service Code, says Koritzinsky.

|And with the global risk of terrorism ever present, the federalbackstop of the Terrorism Risk Insurance Act provides coverage fromterrorism-caused biological, nuclear, chemical and radiologicalperils and is not available internationally.

|Additionally, Sanford Elsass, chairman of the National RiskRetention Association, points out that the Patriot Act putsstringent due diligence on banking and cash flows in and out of thecountry. “If you're a little captive, those changes and expensescould cause you to stay onshore,” he says. “The [biggest] factorsaren't only the costs of doing business offshore but also the costof travel, because if you're an offshore captive you can't haveboard meetings onshore.”

|Although onshore captives have expanded greatly since Coloradobecame the first American state to allow captives in the 1970s,followed by Vermont and Tennessee, the day may never come whencaptives are welcomed in each jurisdiction.

|“I doubt we will ever get to a position where all 50 states havecaptives laws,” says Koritzinsky. “For example, California andTexas have a bias against captives.

|“It's a question of control,” he explains. “Regulators oftenhave a hard time keeping their hands off of business.”

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- All PropertyCasualty360.com news coverage, best practices, and in-depth analysis.

- Educational webcasts, resources from industry leaders, and informative newsletters.

- Other award-winning websites including BenefitsPRO.com and ThinkAdvisor.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.