In such an eventful year, with dozens of compelling stories asstrong contenders, determining the Top 10 of 2011 was no easy task.But, after a lot of labor—and internal debate—we feel the finallist we've put together successfully captures the essential news ofthe past 12 months.

|Of the hundred or so specific insurance lines we've writtenabout since January, two really stood out in 2011: One is a majorcomponent of the commercial business, and it had a rough year withsome worrisome trends. The other line is relatively new to thescene, but it made a strong bid this year to situate itself as akey part of any risk-management portfolio.

|Speaking of risk managers, one concept that helps elevate theirposition in the corporate hierarchy continues to catch on in boardrooms and C-suites across the nation.

|And as it has been for the past decade—and likely will be for atleast the next 10 years—technology was a critical coverage area allyear, as vendors introduced powerful new products—and earlyadopters in the insurance field embraced them. Another old,reliable source of stories was the nation's capital, withindustry-impacting events seeming to emerge fromWashingtonby thehour.

|Three individual companies created enough of a stir in 2011 tomerit their own place on the list: One was hotly pursued as anacquisition target by a number of well-known suitors; one made achange to its core product that sent out shockwaves that affectedeveryone from reinsurers to risk managers; and the third is anindustry giant (and household name) that generated big headlinesthroughout the year.

|Our top two stories? You'll have to click through the slideshowto see, but these two topics so dominated the year's conversationthat you might already have a good idea.

|Click next to begin the slideshow.

||

#10 Workers' Comp Injury Claims on the Rise for First TimeSince 1997

|

Times are tough for the American worker, whether at the officeor on the assembly line—and conditions are at least equallychallenged for those underwriters that offer workers' compensationinsurance to the country's employers.

|This year's "State of the Line" study from the National Councilon Compensation Insurance (NCCI) paints a gloomy picture, withperhaps the most surprising and disturbing statistic: thenationwide lost-time claim frequency increased 3 percent—the firstincrease since 1997.

| Net-written premium for workers'comp private carriers declined 1.3 percent in 2010, according tothe NCCI report, and the line produced a 1 percent pre-taxoperating loss—the first such loss since 2002. The workers' compline is one of the largest in the U.S. property-and-casualtyindustry and among the largest commercial lines. It makes up nearly8 percent of total industry premium volume and accounted for about16 percent of all commercial-lines premium in 2010, according toA.M. Best.

Net-written premium for workers'comp private carriers declined 1.3 percent in 2010, according tothe NCCI report, and the line produced a 1 percent pre-taxoperating loss—the first such loss since 2002. The workers' compline is one of the largest in the U.S. property-and-casualtyindustry and among the largest commercial lines. It makes up nearly8 percent of total industry premium volume and accounted for about16 percent of all commercial-lines premium in 2010, according toA.M. Best.

Results for the workers' comp line deteriorated sharply in 2010,A.M. Best noted. The calendar-year combined ratio increased nearlyseven points to 118.1—the highest level since 2000, when thecombined ratio was 121. The line's results have worsened eachconsecutive year since 2006, when the combined ratio was 98.5.

|One of the biggest challenges facing workers' comp is risingmedical costs, which represent almost 60 percent of the benefitdollar—even higher in some states. The average cost of medicalcosts is rising at about 6 percent per year, NCCI reports.

|Current economic conditions are also a factor in the line'sperformance, with claims—fraudulent or not—often seeing a spike inrecessionary times.

|The fact that the American workforce in general is growingolder—and more obese—only adds to the WC challenges faced by bothemployers and carriers.

|Despite this rather dismal state of WC affairs, NU wasable to find some bright spots amid all these dark data clouds. Thethree winners of our Excellence in Workers' Comp Risk Managementawards (August 22/29 issue), for example, were each able to developunique approaches to their programs that yielded substantialsavings. Kennametal Inc., through a focus on loss prevention, theclaims-administration process, effective return-to-work tactics anda corporate culture of safety, reduced its WC costs from $2.8million in fiscal year 2008 to $1 million in fiscal year 2011—and,bucking the trend, it cut its number of claims from 293 to 125 overthe same period.

|#9 Agents &Technology: 2011 Proves a Watershed Year for Adopting NewTools

|

Mobile apps from indie agents. Real-time processing—not only ofpersonal-lines business, but also of midsize commercial accounts.Social media as a marketing essential. Cloud computing. The past 12months saw a number of game-changing tech trends that are rapidlyaltering how agents and brokers do business.

|Though these latest tools have hardly achieved 100-percentpenetration, they have become the norm for a growing roster ofproducers. Real-time technology use, for example, is definitely onthe rise—and for agents competing for personal business againstdirect carriers, such instant quoting capability is a do-or-dieissue.

| A recent survey released by theReal Time/Download Campaign said that of the 3,100 insurance agentsand brokers surveyed, the number of agents using real-time tech isup six points to 63 percent of agency-management-system users forpersonal lines. Stu Durland, the Real Time/Download campaign'sco-chair, calls this an encouraging sign—and one "critical to thefuture viability of the independent agency system."

A recent survey released by theReal Time/Download Campaign said that of the 3,100 insurance agentsand brokers surveyed, the number of agents using real-time tech isup six points to 63 percent of agency-management-system users forpersonal lines. Stu Durland, the Real Time/Download campaign'sco-chair, calls this an encouraging sign—and one "critical to thefuture viability of the independent agency system."

On the commercial side of the real-time issue, the LexisNexisInsurance Exchange, which aims to simplify submissions of midmarketcommercial-lines risks to multiple carriers, gained some realtraction in 2011. The Exchange, backed by the Council of InsuranceAgents & Brokers and Marketcore, saw the number of weeklysubmissions increase to an average of 1,000 per week and more than2,000 individual users.

|And while the large carriers and their captive agents have hadmobile apps for a few years now, 2011 saw Main Street producersstarting to create their own to offer better customer service totheir clients—who now expect to be able to execute routinefinancial transactions on their smartphones.

|Additionally, in a largely overcast year—where revenuereductions had agencies looking for ways to cut costs and boostproductivity—many began counting on cloud-computing solutions as ameans to both eliminate some IT expenses and increase access todata by employees.

|On the social-media front, personal-lines agents using Facebookand Twitter have begun to realize some tangible, if small, benefitsas they establish a presence where a growing number of theirclients and prospects are spending more time.

||

COVERAGE HIGHLIGHTS

|• Agents Look to the Cloud for Flexibility, Cost Savings

|• Data Star: At One-Year Anniversary, Strong Optimism But Slow Uptakefor LexisNexis Insurance Exchange

|• Agents in Apps: Main Street Producers Begin to Embrace MobileSolutions

|• Next Big Hurdle: Real-Time Processing for MidmarketCommercial

|• The Real-Time Divide: Small Agencies That Don't Cross It CouldDie

||

#8 ERM, SRM Gaining Ground with Risk Managers; ReinsurersLeading the Way

|

Enterpriserisk management continued to move more toward themainstream in Corporate America this year, with its implementationbeing driven by anxious boards and by CEOs more acutely aware thanever of the need to understand and mitigate existentialthreats.

|This increasing stature of the concept, especially at Fortune1000 firms, is good news for risk managers: It means greaterrecognition of the strategic contributions they can make, and ERM'sgrowing acceptance should open up more opportunities for riskmanagers to consult with a company's top decision-makers.

| In our own insurance industry,ratings agencies are helping push the practice of ERM further upthe C-suite "Must Do" list.

In our own insurance industry,ratings agencies are helping push the practice of ERM further upthe C-suite "Must Do" list.

In fact, reinsurance giants are not only leading the charge onERM within the insurance sector—they are so advanced that they canserve as models for almost any company considering a program.

|"Reinsurers are sophisticated when it comes to developing ERMsystems, and it's a cultural phenomenon at these companies," saysPeter Dickey, assistant vice president of A.M. Best's reinsuranceratings division. "It's accepted from the board to the lowestperson, and they make sure that message gets through toeveryone."

|While many small to midsize companies in the U.S. believe thereis something to be gained through ERM practices, they are stillmoving slowly toward building an infrastructure for it, says StefanHolzberger, A.M. Best's vice president of rating criteria andregulatory-policy development.

|One element of ERM, and an emerging discipline in 2011, isstrategic risk management (SRM), which was defined and recognizedby the Risk and Insurance Management Society at its annualconference this May.

|SRM, a central component of ERM, focuses on the biggest and mostlikely risks to shareholder value. This process helps risk managersidentify and assess those issues that could most severely impair anorganization's ability to execute its businessstrategies.

||

COVERAGE HIGHLIGHTS

||• RIMS Embraces Strategic Risk Management

||• SRM Can Take ERM to the Next Level

|• Case Study: Beginning a Global ERM Program at NYU

|• ERM Rodeo: Roping Risk with Effective Controls

|• Wolters Kluwer Expands ERM Consulting to Finance, InsurancePlayers

|||

#7 Bold-Faced Buyers Battle to Acquire Transatlantic

|

Ending a five-month, multiparty bidding war—with Warren Buffettas one of the belligerents—investment holding company AlleghanyCorp. recently reached a deal whereby reinsurer Transatlantic wouldbecome its independent subsidiary in a $3.4 billion deal.

| The battle for Transatlanticbegan on June 12 when the company and Swiss-based Allied WorldAssurance Co. Holdings announced a $3.2 billion merger deal thatexecutives said would create a global specialty insurer andreinsurer operating in 18 countries on six continents. But onemonth later, Bermuda-based Validus Holdings Ltd., led by CEO EdwardJ. Noonan, made an unsolicited, competing $3.5 billion offer of itsown to acquire Transatlantic. The companies sparred throughoutJuly, with Transatlantic filing a lawsuit in Delaware alleging thatValidus had made false and misleading statements to Transatlantic'sstockholders through tender-offer materials.

The battle for Transatlanticbegan on June 12 when the company and Swiss-based Allied WorldAssurance Co. Holdings announced a $3.2 billion merger deal thatexecutives said would create a global specialty insurer andreinsurer operating in 18 countries on six continents. But onemonth later, Bermuda-based Validus Holdings Ltd., led by CEO EdwardJ. Noonan, made an unsolicited, competing $3.5 billion offer of itsown to acquire Transatlantic. The companies sparred throughoutJuly, with Transatlantic filing a lawsuit in Delaware alleging thatValidus had made false and misleading statements to Transatlantic'sstockholders through tender-offer materials.

In August, yet another player entered the game as BerkshireHathaway's National Indemnity Co. put in a competing bid. Validusthen filed suit against Transatlantic and the board, arguing thatthe board had not given sufficient reason for refusing to considerValidus' offer.

|Days before a scheduled Sept. 20 vote on their planned merger,Transatlantic and Allied World announced they had ended theirattempted deal. Transatlantic was left to consider bids fromValidus, National Indemnity and an "undisclosed third party."Ultimately, in November, Alleghany and Transatlantic announcedtheir transaction, which is expected to be finalized during 2012'sfirst quarter.

||

#6 Cyber Liability Emerges as Key Coverage for Digital Age

|

While the words "sexy" and "insurance" seldom appear in the samesentence, cyber liability changed that in 2011.

| Speaking about coverage fordata-breach risk, Jake Kouns, senior director of technology and adata-privacy underwriting expert at property-and-casualty insuranceholding company Markel, said in October, "It's the new, sexy insurance. There are 30carriers now writing it."

Speaking about coverage fordata-breach risk, Jake Kouns, senior director of technology and adata-privacy underwriting expert at property-and-casualty insuranceholding company Markel, said in October, "It's the new, sexy insurance. There are 30carriers now writing it."

The reason for this inrush of underwriters, of course, is thatthe digital storage and transfer of data is a critical part ofdoing business today for a huge—and constantly growing—swath ofindustry sectors. Insurance companies, banks, asset managers,retailers and, as Sony reminded us this spring, even gamemakers—they all handle private financial data.

|And it's not just hackers, viruses and phishing emails that putdata at risk. Security breaches can just as easily be caused bylost or misplaced files or even mishandled waste. A breach thatresults in a client's data being stolen and used in a damaging waycan lead to substantial third-party liability claims—and governmentpenalties.

|A report from Lloyd's and technology company HP earlier this yearwarned that businesses becoming more reliant on technology willface more complex and damaging digital attacks as sophisticatedcriminals quickly adapt their methods to steal from, disrupt andspy on businesses.

| Larger companies have beenattuned to the risks of data-poaching and Web-site shutdowns for awhile now—and many have stopped inquiring about coverages and haveactually started buying policies. Why cyber liability could proveto be a major new business opportunity for agents, brokers andcarriers is that the risks of expensive data breaches very muchextend to small and midsize businesses as well.

Larger companies have beenattuned to the risks of data-poaching and Web-site shutdowns for awhile now—and many have stopped inquiring about coverages and haveactually started buying policies. Why cyber liability could proveto be a major new business opportunity for agents, brokers andcarriers is that the risks of expensive data breaches very muchextend to small and midsize businesses as well.

Indeed, it is companies outside the Fortune 1000 that could findit very difficult to recover from a data breach without the rightinsurance, says Kouns, who also serves as chairman/CEO of the OpenSecurity Foundation—a nonprofit public organization that seeks tohelp businesses minimize their information-security risks.

|While cyber coverage has moved from an afterthought to afront-burner issue for many risk managers this year, the types ofcoverages being offered are still all over the map. Policies cancover everything from helping reconstitute data to thepublic-relations expenses needed to repair a damagedreputation.

| Prices, too, are evolving—and areperhaps still too low. "Right now you can get a policy with a $1million limit for $1,500 in premium," notes Kouns. "That isworrisome. It's too cheap. Companies will buy the coverage andthink they don't need to do anything to secure their systems."

Prices, too, are evolving—and areperhaps still too low. "Right now you can get a policy with a $1million limit for $1,500 in premium," notes Kouns. "That isworrisome. It's too cheap. Companies will buy the coverage andthink they don't need to do anything to secure their systems."

Even though cyber risk is everyone's problem, the Zurich-sponsored survey "A New Era in Information Security andCyber Liability Risk Management" in October showed that ITpersonnel are the ones who are generally considered (by 73.2 of therespondents) to be responsible for protecting against such threats.Only 13.2 percent believed it is the risk-management/insurancedepartment's responsibility.

||

COVERAGE HIGHLIGHTS

|• Mind the Gap: Cyber Breaches Are Expensive, Exposures Wide

|• Vast Majority of Companies Not Covered for Cyber Attack

|• Safeguarding Client Info Is Life-or-Death Issue forAgencies

|• Cyber Liability Represents a New Frontier for E&S BrokerageHorizon

|• Cyber Risks Emerging as Top Concern for Attorneys

||

|

#5 In D.C., a Busy 2011 Saw Number of Major Moves That WillShape P&C Future

|

Politicians, bureaucrats and industry associations kept our D.C.bureau chief, Arthur D. Postal, plenty busy in 2011. Here are hisencapsulated reports on the quartet of congressional stories thatmattered most this past year—and which will continue to benewsmakers in 2012.

|

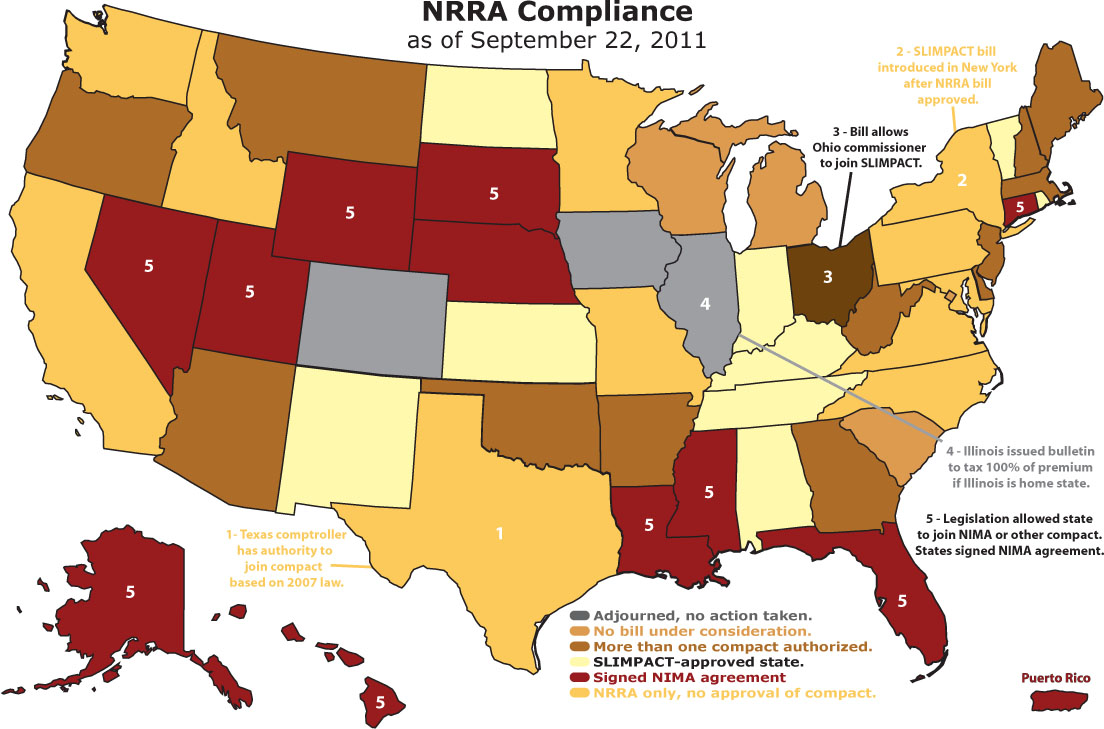

NRRA: Law to Modernize Surplus-Lines Regulation HitsImplementation Hurdles

|

In 2011, the insurance industry accomplished its goal ofmodernizing surplus-lines regulation when federal legislation—theNonadmitted and Reinsurance Reform Act (NRRA)—went into effect July22, establishing the insured's home state as the only one withjurisdiction over multistate surplus-lines transactions—andtherefore the only one that can require a tax be paid by thebroker.

|But sizable roadblocks remain toward establishing a uniformsystem for disbursing premiums owed to states where the actual riskexists. While most of the industry would prefertheKentuckyallocation system, there is no consensus among thestates about an allocation mechanism, nor any means of pressuringstates toward adoption of a uniform system.

|The how—and when—of NRRA implementation will remain a top storyin 2012.

||

FIO—Dodd-Frank Offspring—Sparks Some Concern AboutIncreasing Federal Oversight

|

In May, the Federal Insurance Office established under theDodd-Frank Act (DFA) became operational, with Michael McRaith, theformer insurance commissioner ofIllinois, as its firstdirector.

|McRaith is in the process of forming a staff, which will provideinformation about the insurance industry to the Financial StabilityOversight Council and the Treasury secretary. He has also formed anadvisory council of state insurance regulators and industryofficials to advise him on various issues the industry isfacing.

|There are two key concerns to watch out for: One is how FIO andthe entire Treasury Department works with the states, the Office ofthe U.S. Trade Representative and Congress on internationalsolvency and reciprocal trade issues.

|The second is the reaction of Congress and the states to FIO'spending report on how insurance regulation can be modernized andimproved. The report is mandated by the DFA and is due in lateJanuary.

|Any suggestion for a stronger federal role is likely to increasetension among states, state regulators and their supporters inCongress.

|

NFIP: Permanently Temporary?

|

The National Flood Insurance Program since Sept. 30, 2008 hasbeen operating on a series of temporary reauthorizations of a lawpassed in 2003. In an attempt to find a more permanent solution,bills have been passed by the full House and the Senate BankingCommittee extending the program until Sept. 30, 2016.

|Both bills call for greater private-sector involvement in theprogram and fewer subsidies for a program already more than $18billion in debt and with little likelihood that it can generate therevenues to repay it.

|However, it's unclear when the Senate will take up the versionpassed by its banking panel in September. The Senate passed ashort-term reauthorization until May 30, 2012, but the House hasnot acted on it yet as of this writing.

|At press time, Congress had a Dec. 16 deadline to either pass afive-year extension or work out another short-termreauthorization.

|House Republicans are also rolling a longer-term extension intoa controversial bill that would extend some tax cuts and offsetthem with budget cuts, but industry observers are not optimisticthe bill would get through the Senate. Additionally, PresidentObama has threatened to veto it.

|

Commission Mission: MLR Exemption

|

Insurance agents, both in property and casualty and life, areseeking an exemption of their commissions from the medical lossratio (MLR) provision of the Patient Protection and Affordable CareAct. The Department of Health and Human Services, led by KathleenSebelius, has refused to provide such an exemption, and legislationhas been pending in the House for six months without flooraction.

|Given that there is strong opposition to an exemption from theDemocratic majority in the Senate, agents appear to face an uphillclimb for relief, despite their pleas that they play a key role inthe health-care process and that they have lost significantrevenues as a result of the MLR provision.

||

|

#4 AIG: Industry Giant Generates Host of Headlines inRoller-Coaster Year

|

While dozens of insurance companies made big news in 2011, nonecould come close to matching the sheer quantity of headlinesgrabbed by AIG—the recipient of an $182 billion government bailoutand an industry giant whose Chartis division is one of the keyP&C players.

|The roller-coaster year started strong when in January AIG CEORobert Benmosche declared that despite its financial challenges,the beleaguered multinational insurance corporation could "see thefinish line" as it continued to pay down its debt to the FederalReserve and raised money from private investors.

|The comeback continued with more good news in Februarywhen AIGreported strong earnings of $11.2 billion for the fourthquarter of 2010.

| But that same month saw some badnews as well: The company announced it would recorda $4.1 billion charge for 4Q 2010 to bolster loss reserves forChartis. The decision was made after the company's year-end reviewof loss reserves.

But that same month saw some badnews as well: The company announced it would recorda $4.1 billion charge for 4Q 2010 to bolster loss reserves forChartis. The decision was made after the company's year-end reviewof loss reserves.

In March, Chartis shook itself up with a reorganization of thestructure of its management team, with Peter Hancock replacingKristian Moor as CEO (Moor would become vice chairman).

|Hancock, who designed the bailed-out company's recapitalization plan, earned a slot on the cover ofNU's Sept. 19 issue when he gave his first in-depthinterview about his vision for the company.

|In August, Benmosche appeared on CNBC and declared "missionaccomplished"—or something close to it. AIG posted 2Q net income of$1.8 billion (compared to a net loss of $2.7 billion for the secondquarter a year before), and he announced AIG had "turned thecorner, and our crisis is over.

|"We're independent of government support," he added during the2Q earnings call. "It's all been collateralized. And we'redone."

|Currently, the U.S. Treasury, as part of the recapitalizationplan, owns about 77 percent of AIG, but the company has nooutstanding debt to the government.

|But by 3Q, AIG had reporteda loss of $4.1 billion (the company's worst since 2009), drivenby declines in equity markets, widening credit spreads and lowerinterest rates.

|Still, AIG remains at least a 780-pound, if not 800-pound,P&C gorilla. While the company slipped to the sixth position inNU's annual ranking of the Top 100 insurance groups bynet-premium written (from fourth the year before and second in2007), Chartis, despite the hurdles faced by its parent company,has found a way to maintain market-leadership positions in multiplelines.

||

COVERAGE HIGHLIGHTS

|• AIG, Feds Agree to Repayment Date

|• AIG to Take $4.1 Billion Reserve Charge

|• Chartis Sees $5 Billion Underwriting Loss on Reserve Charge

|• AIG Pays $6.9B Toward TARP Loan

|• Chartis Names New CEO After Management Shakeup

|• AIG Sued for Hundreds of Millions by Former Head of Global RealEstate

|• Benmosche: AIG "Still a Very Strong Company"

|• $450M AIG Workers' Comp Settlement Gets Judge's Approval

|• Benmosche Says Crisis Is Over as AIG Posts $1.8B 2Q Income

|• Starr International Sues U.S. for $25B Over AIG Bailout

|||

#3 RMS Cat Model Revision Ignites a Windstorm

|

One of the biggest gusts of change that blew through theindustry in 2011: The revisions that catastrophe-modeler RiskManagement Solutions made to its U.S. Hurricane Model.

|Loss results for portfolios that RMS analyzed, based on therevisions, increased from 20 percent to as much as 100 percent.

|"We didn't want to be an event," says Ryan Ogaard, senior vicepresident of model management for RMS. "But these were big changes.We understand that."

| The updates to the model,incorporated into RMS Version 11.0 and based on a deep analysis ofbillions of dollars in claims and reams of other data, increasewind-related loss estimates for noncoastal areas and even inlandstates.

The updates to the model,incorporated into RMS Version 11.0 and based on a deep analysis ofbillions of dollars in claims and reams of other data, increasewind-related loss estimates for noncoastal areas and even inlandstates.

The changes—which actually have lowered some risk estimates forcoastal areas in Florida and elsewhere—prompted one reinsurancebrokerage executive to observe: "Basically, this makes Ohio acoastal state."

|As the changes have filtered through risk portfolios, the impacton reinsurance rates for property exposures has been significant,especially for those with significant risk concentrations in Texasand the Gulf States.

|Pina Albo, president of the reinsurance division for MunichReinsurance America, says June and July rates went up in the10-plus percent range for large U.S. property renewals—a bump shebelieves was due in no small part to RMS Version 11.0.

|Numerous other insurance executives also have mentioned themodel changes during quarterly earnings calls and variousconferences, citing it as an important part of the equation (whichincludes higher catastrophe losses, lower investment gains and adecrease in favorable prior-year reserve releases) that is leadingto both rate increases and a likely turn in the soft market.

|It was a busy year for RMS: The modeler also updated its windmodel in Europe. Ogaard says RMS "hasn't heard too much" about theEuropean adjustments, but the company is still explaining nuancesof Version 11.0, including its medium-term rates for hurricaneoccurrence and new storm-surge projections that could result inflood losses, even on a wind policy.

|"It was harder than we expected for the industry to understandthese aspects," says Ogaard. "The baseline aspects of the model arelargely put to bed, but we are still talking about these specificissues."

|Ogaard says RMS has no definite plans to make any changes toVersion 11.0.

|"You can't tone [the findings] down [simply] because they arehard to deal with," he says. "We have to stay true to our missionto give the best possible view of risk."

|To further enable the industry's use of RMS' new data, themodeler plans to develop tools around the model to "open the blackbox" and make it "easier to dig into.

|"We seek to be more transparent than ever and allow our clientsto fully get the benefits of our products," Ogaard adds.

||

COVERAGE HIGHLIGHTS

|• Bermuda Exec: RMS Model Change, First-Quarter Cats Could TurnMarket

|• Cat Modeling: Ingrained in the Industry, Embroiled inControversy

|• Billions for Bermuda: Cat-Model Changes Could Drive $20-$60 BillionSurge in Reinsurance Demand

|||

|

#2 The P&C Pricing Picture: Rates Edge Up in Year ofStaggered, Unsteady Transition

|

Two steps forward, one step back: For every couple of eventsthat augured a definitive swing to a hard market this year—a majorcatastrophe here, increasing combined ratios there—some otherfactor contributed to helping keep prices soft, whether it was fearover the eurozone debt crisis or underwriters willing to heavilydiscount new business.

|But while the pace of change has been staggered and unsteady—andis still by no means universal across all lines—there is littledoubt that the market has undergone a significant transition in2011.

| In January, market conditionscould be summed up as mostly soft, with pockets of flatteningprices. By September/October, the consensus was the overall markethad finally hit bottom. And by November, the pricing picture couldbe described as upward bound, if barely so, for the first time ineons—or at least since 2005.

In January, market conditionscould be summed up as mostly soft, with pockets of flatteningprices. By September/October, the consensus was the overall markethad finally hit bottom. And by November, the pricing picture couldbe described as upward bound, if barely so, for the first time ineons—or at least since 2005.

In the pages of NU and on our PropertyCasualty360.comWeb site, we wrote this year literally hundreds of articles—daily,sometimes hourly—on the soft/flat/(maybe) hardening market, asanalysts, CEOs, the occasional soothsayer and others offered theirassessments of the current state of the market and gave theirpredictions about when (or if) the market would turn, and whatwould cause it.

|But perhaps nothing better conveys what happened on the pricingfront in 2011 than the MarketScout pricing barometers we publisheach month. As they show, it wasn't a swift shift—but climb pricesdid, from an average decrease of 5 percent last December to thelatest report: a 1 percent gain in November.

||

|

#1 A Disastrous 2011 Sees Epic Losses Across the Globe

|

If one could use only a single word to sum up 2011,"catastrophes" best captures what this year was all about.

|January started on a soggy note with large pockets of Australiaunder water, as floods caused insured losses of up to $3 billion.Just the next month, the Southern Hemisphere suffered again, as NewZealand saw a 6.3 earthquake that toppled buildings in Christchurchand led to claims north of $10 billion (part of a nightmarish,12-month stretch where Kiwis experienced multiple quakes, includingone in September of 2010 and another one in June of this year).

| Then, for a few unforgettableweeks in the late winter and spring—from the massive Japaneseearthquake and devastating tsunami that followed through the spateof tornadoes that ravaged the U.S. in April and May—it seemed likea major disaster struck every other day.

Then, for a few unforgettableweeks in the late winter and spring—from the massive Japaneseearthquake and devastating tsunami that followed through the spateof tornadoes that ravaged the U.S. in April and May—it seemed likea major disaster struck every other day.

Indeed, the first half of the year wound up being one for therecord books. Global reinsurer Munich Re counted 355 significantloss events in quarters one and two—which caused an all-time highof $265 billion in economic losses. In the U.S. alone, 100 eventsled to more than $18 billion in insured losses.

|The second half, fortunately, did not see a Katrina-like event,but Mother Nature hardly let us off the hook. While Florida onceagain escaped the hurricane season unscathed, Irene underscored thedegree of damage that can occur deep inland as it pounded, of allplaces,Vermont, and ultimately could lead to $4.3 billion ofinsured property losses.

| And the first half's floods,quakes and tornadoes were joined by summer wildfires in Texas—andthen a freak October snowstorm in the Northeast, severe enough thatMoody's labeled it a "major capital event" for insurers.

And the first half's floods,quakes and tornadoes were joined by summer wildfires in Texas—andthen a freak October snowstorm in the Northeast, severe enough thatMoody's labeled it a "major capital event" for insurers.

The conversation around the importance of supply-chain insurancethat the Japanese quake helped spark only intensified when fallfloodwaters inundated much of Thailand—including nearly 10,000factories that play a critical role in supplying parts to theautomotive and computer industries.

|The collective toll on underwriters was terrible. First-half netincome for U.S. property-and-casualty insurers, for example,plummeted 67 percent compared to the same period in 2010. Thesecond quarter was particularly brutal for domestic carriers with aheavy concentration in personal lines, as the twisters in Alabama,Arkansas, Oklahoma and, most memorably, Joplin, Mo., flattenedhomes and crushed cars.

| Allstate experienced more than$2.3 billion in catastrophe losses from 30 events in thatApril-June timeframe. Liberty Mutual also topped the billion-dollarmark in 2Q, with $1.3 billion in catastrophe losses. By September23, home-and-auto giant State Farm had processed just under onemillion claims—970,000—for the year and had paid policyholders $5billion.

Allstate experienced more than$2.3 billion in catastrophe losses from 30 events in thatApril-June timeframe. Liberty Mutual also topped the billion-dollarmark in 2Q, with $1.3 billion in catastrophe losses. By September23, home-and-auto giant State Farm had processed just under onemillion claims—970,000—for the year and had paid policyholders $5billion.

Not surprisingly, the cumulative hit of all these catastrophesdid cause an overall hardening for property exposures—withAustralia, New Zealand and Japan seeing prices increase bydouble-digit percentages.

|And while none of the events in the singular were enough to endthe soft market, the aggregate effect of the losses does have themarket poised for a general hardening as we enter 2012.

||

COVERAGE HIGHLIGHTS

|• New Zealand Quake Loss Estimates: $3.5B-$12B

|• Devastation in Japan: Will the Magnitude 9.0 Quake Shift theMarket?

|• Cruel Twist: Tornadoes Leave Trail of Devastation & Death FromOklahoma to North Carolina

|• On the Ground in Joplin as State Farm Responds

|• Catastrophes Take Their Toll on Insurers' 2Q Results

|• Hurricane Irene Strikes East Coast; Floods Worse Than Winds

|• Insurers Report More Billion-Dollar Weather Losses as DisastersContinue

|• U.S. P&C First-Half Net Income Dives 67%

|• Thailand Floods Could Cost Insurers Billions

|• 3Q Earnings: Catastrophes Continue to Plague Insurers'Results

|

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- All PropertyCasualty360.com news coverage, best practices, and in-depth analysis.

- Educational webcasts, resources from industry leaders, and informative newsletters.

- Other award-winning websites including BenefitsPRO.com and ThinkAdvisor.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

{kind=link}