It's clear that social media usage has risen in all age groups, and the largeswaths of information posted by individuals reflect preferences,lifestyles, habits, and, in some cases, neuroses. Insurers can usethis mounting social data to create a real-time risk profile whileshaping more effective claims and underwriting operations, Celent explains in its newreport, "Using Social Data in Claims and Underwriting."

It's clear that social media usage has risen in all age groups, and the largeswaths of information posted by individuals reflect preferences,lifestyles, habits, and, in some cases, neuroses. Insurers can usethis mounting social data to create a real-time risk profile whileshaping more effective claims and underwriting operations, Celent explains in its newreport, "Using Social Data in Claims and Underwriting."

Although there has been much buzz about the potential fullimpact of harnessing social data, until fairly recently fewstrategic solutions had surfaced. But Celent is leading thediscussion on broader applicability, presenting a five-step modelto operationalize social data. The model outlines the majordecisions that should be addressed in implementation: what datashould be used, what technical strategy should be adopted, how toacquire the data, how to analyze it, and how to integrate socialdata with existing operational systems. Standard Inputs into RiskEvaluation

Integrating these data inputs into insurers' existing process andautomation environment will drive more optimal results in bothclaims and underwriting, assert Celent Analyst Craig Beattie andSenior Analyst Mike Fitzgerald, authors of the report. They stressthat one of the keys to successful implementation will be temperingenthusiasm with the reality that social data is still in itsformative stages.

"This [social data] implementation will not be without challenges,"Beattie says. "Key techniques must be developed or enhanced,including reliable authentication methods, improved data extractiontools, and more advanced analysis tools."

|"It must also be remembered that, at one time, previousinnovations such as multi-tiered automobile pricing, predictiveanalytics, and the use of tele-underwriting in place of attendingphysician statements, were viewed as optional changes tolong-standing insurance processes," he adds. "This transition willnot be without challenges."

|P&C insurers will need to develop techniques or augmentexisting ones. "Additionally, regulation concerning the use ofsocial data is evolving more slowly than the technology andpotentially will significantly impact the use of informationcollected from these public forums," the authors explain.

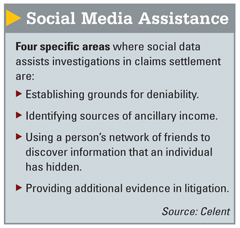

|In the report, Beattie and Fitzgerald provide a more in-depthoverview of current and future uses of social data in coreinsurance operations. By identifying the policy decisions thatshould shape an insurer's social information strategy while raisingtechnical issues and possible solutions related to the uniquecharacteristics of social data, Celent intends to equip insurerswith practical considerations to unlock the true value of socialnetworks. Pervasive Fraud

Among other topics, the Celent analysts discuss how stagedautomobile accidents and "soft" fraud— over-reporting damagedvalues after a fire, for example—pose a significant drain on theindustry, citing some troubling statistics from the NationalInsurance Crime Bureau (NICB), including: an estimated 10 percentof all U.S. P&C insurance claims are fraudulent; and workers'compensation fraud may cause insurers as much as $5 billion on anannual basis.

As such, Celent stresses that it is in the collective interestof both insurers and insureds (at least the honest ones) to reducethe amount and cost of fraud. Social networking data is alreadyhaving an impact in this area, and the potential benefits aresignificant.

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- All PropertyCasualty360.com news coverage, best practices, and in-depth analysis.

- Educational webcasts, resources from industry leaders, and informative newsletters.

- Other award-winning websites including BenefitsPRO.com and ThinkAdvisor.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.