Thanks to the ever-increasingpopularity of youth sports—and the desire of kids of all ages tostay fit and have fun—the amateur-athletics market is a relativelyhealthy segment of the property/casualty arena, providing areas ofopportunity for agents experienced in this field to grow theirbusiness.

Thanks to the ever-increasingpopularity of youth sports—and the desire of kids of all ages tostay fit and have fun—the amateur-athletics market is a relativelyhealthy segment of the property/casualty arena, providing areas ofopportunity for agents experienced in this field to grow theirbusiness.

Despite a slight dip in some sports due to the economy—insurershave seen a drop in paintball players and the frequency of play,for example—business is good for the most part, say experts thisniche.

|“We're seeing a little bit of erosion, but there's a largeuniverse for this [insurance type] out there,” says Tony Pulgine,president of MIC Insurance Brokerage Inc. in Naperville, Ill. “Evenwith the economic downturn, we have not seen a significant drop insports clients. Parents want to do whatever they can to keep theirchildren active.”

|James Decker, assistant vice president, Commercial LinesDivision, for the Bala Cynwyd, Pa.-based Philadelphia InsuranceCos., agrees: “People still want anything for their kids. Peoplewill cut in other areas.”

|Decker identifies one social trend as a key driver that iskeeping parents spending despite the still-difficult economy:getting their offspring into a competitive college. “People want toget their kids involved at a younger age in sports that collegessee as an extracurricular activity,” Decker says. “There's intensefocus on training at younger ages and year-round training. Soccerand baseball are now year-round.”

|This push by parents to pad their kids' resumes is one reason“we are seeing growth in [this segment] of the industry,” saysDecker, whose company writes sports-league and sports-campinsurance in every state except Louisiana.

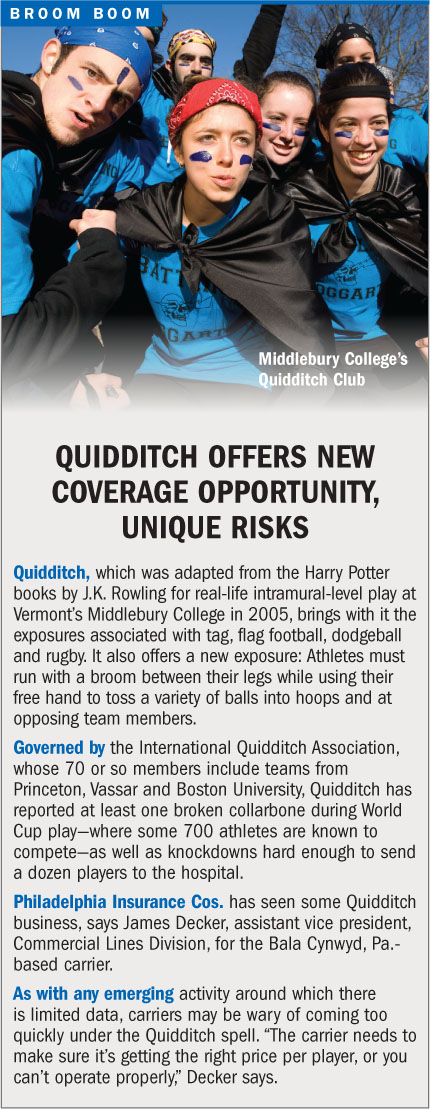

|Other amateur-athletic areas also seeing nationwide growth arecamps for gymnastics and competitive cheerleading. Personal-fitnesstraining, rock climbing and Quidditch [see sidebar] are otherburgeoning sports, Decker says.

|THE PERILS OF PLAY

|The three biggest exposures in the amateur-sports niche areparticipant injury, spectator injury and sexual abuse ormolestation, says Mark Nichols, managing director, Accident andHealth Unit, for Markel Corp. of Richmond, Va. Among the many waysa player can get hurt—in addition to the risks inherent to theactivity—are negligent coaching or a faulty playing field.Spectators can be injured falling out of bleachers or getting hitwith errantly thrown or batted balls.

|And serious injuries aren't just limited to rougher team sportssuch as football or hockey. “You do run into neck fractures andthose types of things with gymnastics,” Pulgine says.

||

In terms of sexual-abuse and molestation exposure in youthleagues, some states allow hold-harmless waivers, says Nichols, inwhich the insured have participants sign a waiver releasing theinsured of any liability. Not-for-profits, such as governmentalagencies or charitable organizations, also may have immunitydefenses against claims for sports leagues that are run bymunicipalities or churches.

|But the potential for abuse claims is always there. “You'regoing to have a lot of one-on-one exposure between adults andkids,” Decker says, whose Philadelphia Insurance is a longtimewriter of abuse & molestation coverage for non-profitsocial-services entities that include athletics camps. Overall,sports camps and leagues don't have a huge number of injury claims,but when they do, they're large: The sports niche is really abusiness for catastrophic claims, Pulgine says.

|That was devastatingly apparent earlier this month, when aplayer in the Winslow (Arizona) Little League was fatally injuredwhen he took an inside pitch to the chest as he tried to bunt; theball hit him just above the heart. Hayden Walton, 13, collapsed atthe scene and died in a local hospital the followingmorning.

| The Winslow Little League did participate in groupinsurance from Chartis Insurance Group offered through LittleLeague International, says Dan Kirby, director of risk managementfor the Williamsburg, Pa.-based baseball and softball organization.Covers for membership in Little League International are generalliability and accident & medical; the program death benefit is$10,000 and is covered under the accident policy, he says.

The Winslow Little League did participate in groupinsurance from Chartis Insurance Group offered through LittleLeague International, says Dan Kirby, director of risk managementfor the Williamsburg, Pa.-based baseball and softball organization.Covers for membership in Little League International are generalliability and accident & medical; the program death benefit is$10,000 and is covered under the accident policy, he says.

About 96 percent of Little League members take advantage of thegroup program, which can offer substantially lower rates thanprivate insurance. Leagues in the program also receive a D&Opolicy along with their GL policy, Mr. Kirby says. The limits are aGL minimum requirement of $1 million per occurrence with a $2million aggregate and a $1 million D&O policy.

||

THE PRICING PICTURE

|Rates for GL and participant-accident insurance (PAI) fell alongwith the economy and have remained flat since, according toPulgine. “But we don't see it continuing to drop,” he says.Occasionally, a new player will come into the PAI market and lookto compete with lower pricing. “There seems to be more interest inthat line than any other,” he says.

|“Clients are concerned about price, and you have to be on yourtoes,” he says.

|Decker observes that insurers looking to get into the sportsfield may do so without knowing the business—and so may not becharging enough per participant.

|For its part, Philadelphia Insurance provides coverage for some3,000 athletic leagues and camps across the nation, with premiumsaveraging about $5,000; smaller camps and clinics pay $1,000 orless.

|AMATEUR NICHE—FOR PROS ONLY

|Sports insurance can be profitable for insurers who know thefield, even in a year where the P&C market has already sufferedtremendous cat losses, says Decker.

|But while there's money to be made in sports camps and amateursports leagues, success in this niche requires specialization—thosediving in with little or no experience may find themselves in overtheir heads.

|“You have to know what you're doing. There are little nuances toeverything,” says Pulgine, whose MIC sells two main linesof insurance—GL and PAI—to clientele such as youth baseball andsports camps for gymnastics and cheerleading. It also sells packageand umbrella policies for accounts that might need additionalcover, like a marine or equine policy. MIC is licensed in all 50states and has some 2,500 sports clients countrywide.

|Markel's Nichols agrees that this product type requires aspecialized knowledge—and tends to attract a certain type of agentor broker.

|“The people who typically specialize in it are generallyathletes themselves—guys who have been [involved] in sports,” saysNichols, whose company has been writing GL and PAI cover foramateur sports nationwide since 1995.

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- All PropertyCasualty360.com news coverage, best practices, and in-depth analysis.

- Educational webcasts, resources from industry leaders, and informative newsletters.

- Other award-winning websites including BenefitsPRO.com and ThinkAdvisor.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.