For Tony Morgan, a propertyunderwriter specializing in earthquake coverage, the spark for hisfirm's latest specialty-insurance program idea was nothing morethan an interesting newspaper article that really had nothing to dowith earthquakes—or even insurance.

For Tony Morgan, a propertyunderwriter specializing in earthquake coverage, the spark for hisfirm's latest specialty-insurance program idea was nothing morethan an interesting newspaper article that really had nothing to dowith earthquakes—or even insurance.

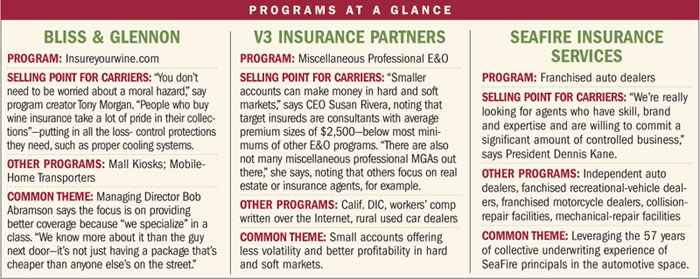

Morgan, a senior vice president for Bliss & Glennon, aRedondo Beach, Calif.-based wholesale brokerage and managinggeneral agent (MGA), recalls reading a few years ago a WallStreet Journal article about wine collectors—in particular,the marital squabbles that develop between husbands who collectrare vintages and wives who don't understand why they can't drinkfrom the prized bottles.

|The article stressed that these men spend so much money on theircollections that when some marriages end in divorce (presumably notover the question of wine consumption), battles over ownership ofthe collection become a problem.

|The need to protect such valuable property from other perils,such as fire and theft, wasn't lost on Morgan.

|“There must be an insurance angle here,” he remembers thinking.Online research into insurance offerings turned up very little—apositive development. “This is a niche nobody has explored yet,” herecalls saying to himself.

| Eventually Morgan did come acrossa few insurers offering coverage to wine collectors, but only aspart of a homeowners policy, “never on a standalone basis.” Morganwas convinced there was opportunity in the standalone niche, but herealized he didn't have the background to know all the underwritingquestions to ask. The Wall Street Journal provided help onthat score, too, pointing him in the direction of Marc Lazar, a St.Louis-based appraiser of wine collections.

Eventually Morgan did come acrossa few insurers offering coverage to wine collectors, but only aspart of a homeowners policy, “never on a standalone basis.” Morganwas convinced there was opportunity in the standalone niche, but herealized he didn't have the background to know all the underwritingquestions to ask. The Wall Street Journal provided help onthat score, too, pointing him in the direction of Marc Lazar, a St.Louis-based appraiser of wine collections.

The two teamed up to develop online coverageavailable today through www.insureyourwine.com. Morganexplains that either the broker or collector can go to the websiteto obtain a policy covering traditional perils like fire, theft andvandalism, as well as special options like international transitcoverage.

|“A lot of collectors are shipping wines—buying it in Europe andsending it home,” Morgan says, explaining the popularity of theoptional cover for damage or loss in transit. He says collectorsstoring wines in third-party warehouses, rather than their ownin-house wine cellars, can also buy coverage under the program.

|Infographic: Programs At A Glance

“We cover you for earthquake and flood—and also if you drop abottle or if your high school kids invade your wine cellar whileyou are on vacation,” he says, noting that sublimits may apply inthat case. Losses arising from the breakdown of a cooling systemare also covered, he notes.

|Premiums start at $250 for $30,000 of coverage, and the websiteallows collectors and brokers to bind coverage for values as highas $500,000. “They go online, fill out an application and get apremium. We double-check the information and then send a formalquote by e-mail,” Morgan says, explaining that Bliss & Glennonalso specifically underwrites submissions for collections valuedover $500,000.

|Asked if there are any uninsurable risks, Morgan couldn't thinkof any situation that would mean turning away a customer. The onlyproblematic risk would be one located in a 100-year flood zone.“They'd have the coverage, but they wouldn't have the coverage forflood,” he says.

|Morgan says the program has 150 clients now—with only a fewsmall losses. With the program recently getting more exposure, 50customers were added in just the last two months, and heanticipates getting to 1,000 over time.

|Morgan knew he had a winning concept, but carriers didn't jumpat the chance to write the coverage when he and Lazar first pitchedit three years ago; the program is currently written in the Londonmarket.

|Insurers “love programs, but tend to go to those already inplace, where they can take them over,” Morgan says, explaining thatthe success rate is historically low for new programs. His wine onehad the added obstacle of relatively small premiums working againstcarrier desires to add large volumes to their books.

|“They want to be able to analyze the history,” he adds. “We hadno history”—just a great idea and long-term vision.

|GETTING PAST GO: DATA, EXPERIENCE KEY

|Even MGAs with less novel ideas for turning collections ofinsureds into brand-new programs meet with carrier resistance,other market participants say.

|“One of our big challenges was we didn't have any data,” saysDennis Kane, president of Overland Park, Kan.-based SeaFireInsurance Services, an MGU launched in March with programs tailoredto the insurance needs of auto dealers and repair shops. “It's hardto go to a carrier and ask them for the underwriting pen withoutdata,” Kane says.

|So how does a great program idea get turned into a businessreality?

|Working to offset the no-data disadvantage is the combinedexpertise of Kane and two other principals, who collectively have57 years of sales and underwriting experience in the business, hesays, noting that the trio all hail from Zurich North America'sUniversal Underwriters Group, which has a history in insuringautomobile dealerships dating back to 1922.

|Like Kane, Susan Rivera, president and CEO of V3Insurance Partners, has staffed her Philadelphia-based MGA withveterans from the carrier side, also launching an auto- dealersprogram (for small used-car dealers in rural locations), as well assmall-account programs for miscellaneous professional liability,California earthquake/difference-in-conditions (DIC) and workers'compensation written over the Internet.

|“The carriers would tell me right out, 'We don't likestartups,'” says Rivera, recalling initial meetings over programideas that had all been successfully done by carriers she workedwith before. “That is their general feeling because it is taking achance,” she says, going on to explain that V3 has gotten pastobjections since launching in 2008 by doing a lot of homework tovalidate the opportunities in submissions to potential carrierpartners.

|“Where we could, we pulled and analyzed competitor rate filings.We pulled [Insurance Services Office] data, so we could look at theloss experience” on the proposed portfolio.

|“We spent hours evaluating industry workers' comp data” for theInternet-comp program. “We put together the policy form. We had theunderwriting guidelines. We had the applications all complete,” shesays.

|Rivera says the timing of her well-documentedand passionately presented proposals—during a soft market—alsoworked to the MGA's advantage. “If an insurance company reallywants to get into the niche you're talking about, they're happy tohave you take on the risk,” she says, referring to the risk ofpouring money into people, technology and infrastructure. During asoft market, “they're not investing” in any of those things, shesays.

|Simple economics, then, moves some carriers to take a chance. Ifthe program doesn't work, what have they lost? They only providedpaper and did a little bit of work, opening the door for a quickexit if program goals aren't achieved, she reasons.

|THE PARTNERSHIP APPROACH

|Kane says SeaFire has the advantage of support from PreferredConcepts, a privately held national program administrator set up in1989, now backed by private-equity investment from Stone PointCapital. He reports that a conversation with Preferred Concepts'principals Stuart Farber and Chris Treanor about “best practicesfor program administrators” turned into an offer to join thePreferred Concepts family, allowing SeaFire to leverage existinginfrastructure.

|“We didn't have to go out and spend $1 million on IT investment.We didn't have to hire a CFO. We could bolt onto their platform,”he says.

|Farber and Treanor, with deep relationships in the industry,introduced SeaFire entrepreneurs to at least 10 potential carrierpartners. Even without historical data to demonstrateprofitability, they used their expertise to understand the uniquerisks of auto dealers—like open-lot exposure to weather-relatedclaims—as a selling point to entice the carriers.

|Another valuable talking point is the use of alimited-appointment distribution that stresses expertise as well.“We're really looking for agents who have skill, brand andexpertise and are willing to commit a significant amount ofcontrolled business,” Kane says.

|Carrier interest was high, and only two of 10 didn't want tomove forward with backing the management team. “The selectioncriteria for us then became time to market, systems, economics andchannel conflicts,” he says, reporting that Chubb ultimately signedonto the deal as the primary carrier.

|At V3, Rivera says the DIC program was the biggest struggle interms of getting carrier support. “It always takes a longer time toget catastrophe capacity, especially as an MGA,” she says.

|For all four niches she works with, she says she did some extraupfront work the summer before V3 actually started hiring to ensureultimate carrier buy-in. “I probably visited 30-40 companyexecutives to validate my niches before I actually built them,” shesays.

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- All PropertyCasualty360.com news coverage, best practices, and in-depth analysis.

- Educational webcasts, resources from industry leaders, and informative newsletters.

- Other award-winning websites including BenefitsPRO.com and ThinkAdvisor.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

{kind=link}