As Congress considers ways to resolve wind-versus-water damagedisputes, the U.S. House of Representatives for the second time intwo weeks opted not to act on a bill that would add windstormcoverage to the National Flood Insurance Program. But Congress maynot have seen the last of this controversial proposal.

|Indeed, Rep. Gene Taylor, D-Miss., who authored the bill, isinsistent on bringing it back to the House floor in September,according to Matt Brady, a representative for the NationalAssociation of Mutual Insurance Companies.

Mr. Brady said the House considered bringing the bill to thefloor on July 30, but ultimately opted to hold off until aftertheir summer recess. He said the lack of action on the bill showsthat Congress is listening to the measure's opponents and realizingthat H.R. 1264, the Multiple Peril Insurance Act, is not goodpolicy.

|The Property Casualty Insurers Association of America saidopponents to the bill include not just the insurance industry butenvironmental groups, consumer advocates, taxpayer watchdogs, thebusiness community and the White House, as well.

|"The fact that the Obama administration and so many consumer,taxpayer and business groups are united in opposition to this billspeaks volumes," said Tom Litjen, PCI's vice president for federalgovernment relations. "We are glad to see that the support was notthere for the bill at this time, and we hope that remains the caseafter the August recess."

|The latest delay marks the second time in as many weeks that thebill was not brought up for a vote, noted Mike Becker, director offederal affairs for the National Association of ProfessionalInsurance Agents. The bill made it to the House floor on July 22but was pulled after debate and before a vote could be held.

|"We think this indicates many House members are having secondthoughts, and support for this bill appears to be eroding,"according to Mr. Becker. "Rep. Taylor's bill would add a peril tothe program that does not belong there because coverage for winddamage is available in the private market and through state windpools."

|Mr. Becker said PIA supports H.R. 5114, the Flood InsuranceReform and Priorities Act of 2010, which extends the NFIP for fiveyears and contains some reforms. That bill passed the House on July19 and is awaiting action from the Senate.

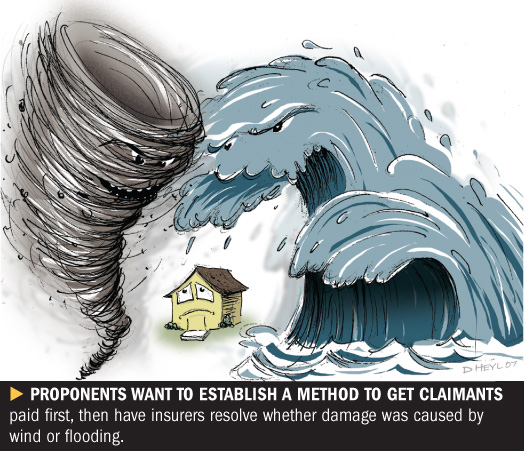

|A separate bill introduced in the Senate that seeks to addressfights over wind-versus-water damage following hurricane-drivenstorm surges–by having the wind insurer and the NFIP each pay thepolicyholder 50 percent of a disputed claim before settlingdifferences through arbitration–will also not be considered untilat least September, according to Mr. Brady. That bill is sponsoredby Sen. Roger Wicker, R-Miss.

|The Wicker bill appears to be generating little support withinthe property and casualty insurance industry.

|Moreover, Rep. Taylor doesn't appear to be accepting the Wickerplan as an alternative to his legislation to add wind coverage tothe NFIP.

|The warmest industry support came from PIA, as Mr. Becker saidthe bill "has some interesting possibilities." However, Mr. Beckersaid PIA has shared two areas of concern in our meetings with Sen.Wicker's staff about this bill.

|First, he said, there would need to be sufficient buy-in on thepart of carriers. "Second, if disputed claims are to be sent toarbitration panels, these panels should be set up by statedepartments of insurance, rather than by the federal government,"Mr. Becker added.

|Jimi Grande, senior vice president of federal and politicalaffairs at NAMIC, rejected the Wicker proposal, saying it "servesonly as a distraction from the fundamental problems facing theNFIP."

|"Instead of bringing actuarially sound rates or reducingsubsidies, this bill would only shift the expense of storm lossesand, ultimately, raise the cost of insurance for consumers in thegulf and elsewhere," according to Mr. Grande.

|"At NAMIC, we believe that any efforts to reform the programshould be focused on moving it toward financial sustainability andeasing the exposure of taxpayers," he said.

|He noted it has been nearly five years since Hurricane Katrina,"and we are still waiting for meaningful NFIP reform because ofpolitical bickering." Meanwhile, "the reliance on short-termextensions has led to an unacceptable number of lapses over thepast several months," he added.

|Blain Rethmeier, a representative for the American InsuranceAssociation, said the AIA's initial concern with the bill is theway in which it is constructed.

|"As currently drafted, the dispute mechanism is triggered by aloss event, and not by an actual dispute," he said. "This presumesthat the claims adjuster does not know how to determine whether, orthe extent to which, a loss was caused by wind versus water."

|In fact, he said, claims adjusters make these determinations allthe time and in the vast majority of cases, it's easy to determinewhich peril caused the loss.

|"And when the loss is caused by a combination of wind and water,the claims adjuster makes a determination as to how much of theloss was caused by each peril. They do this based on the bestscience available, and they use the NFIP's claims-handlingstandards as well as the claims adjusting procedures developed bytheir own company," Mr. Rethmeier explained.

|Brian Martin, policy director for Rep. Taylor, contradictedreports that his boss believes the Wicker bill is a good compromisebetween his legislation, which would add wind to the program, andthe bill recently passed by the House that doesn't add wind toNFIP.

|"[Sen.] Wicker's bill is not a substitute for Rep. Taylor'slegislation," Mr. Martin emphasized. He noted that Rep. Taylor'samendment to the flood bill passed by the House several weeks agolimiting the use of anti-concurrent causation provisions insettling wind/water claims is "slightly similar," in that whenthere is private wind coverage and a dispute arises over how muchdamage was caused by flood versus wind, the homeowner would bepaid, and then the wind and flood carriers would figure out how toallocate the loss.

|That bill–H.R. 5114, the "Flood Insurance Reform and PrioritiesAct of 2010″–passed the House on July 15.

|Mr. Martin said that in Rep. Taylor's amendment, "we have NFIPpay the homeowner, and then the insurer reimburses NFIP after theysort out who owes what," whereas Sen. Wicker's bill "would haveeach policy pay 50 percent and then sort it out inarbitration."

|"I thought we would have some state and [National Association ofInsurance Commissioners] issues if we tried to make the privateinsurer pay the homeowner, so that is why we propose in ouramendment that the NFIP pay the homeowner and then make the insurerreimburse NFIP after the allocation was decided," Mr. Martinadded.

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- All PropertyCasualty360.com news coverage, best practices, and in-depth analysis.

- Educational webcasts, resources from industry leaders, and informative newsletters.

- Other award-winning websites including BenefitsPRO.com and ThinkAdvisor.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.