The Labor Market Insights report is a direct result of stakeholder feedback — carriers are looking for a steady stream of timely and relevant insights on the labor market and what it means for workers' compensation. We deliver economic insights through a workers' compensation lens. Credit: leszekglasner/Adobe Stock

The Labor Market Insights report is a direct result of stakeholder feedback — carriers are looking for a steady stream of timely and relevant insights on the labor market and what it means for workers' compensation. We deliver economic insights through a workers' compensation lens. Credit: leszekglasner/Adobe Stock

Monthly employment reports are typically quite volatile, and it is better to look at longer-term trends to assess the direction of employment gains. The general trend for 2023 showed solid but slowing job growth, and the March report reinforced this pattern.

December and January were initially reported as stellar months of job growth, but they were revised back to reality in the March report. Net employment growth over the past three months averaged 265,000 jobs, well above the estimated 100,000-150,000 jobs needed to match the growth in the working-age population. The March report also saw encouraging signs at the industry level, with a broader range of employment growth than what was seen in 2023.

Strong private sector employment growth combined with still solid wage growth and a tick up in average hours worked led to a reacceleration of payroll growth in February after the slowdown in January.

Average hourly earnings growth remained in line with the recent trend, as average hours worked ticked up and lifted average weekly earnings growth. Strong wage growth and strong employment growth in February helped boost payroll growth over the past 12 months back above 5%. Credit: NCCI

Average hourly earnings growth remained in line with the recent trend, as average hours worked ticked up and lifted average weekly earnings growth. Strong wage growth and strong employment growth in February helped boost payroll growth over the past 12 months back above 5%. Credit: NCCI

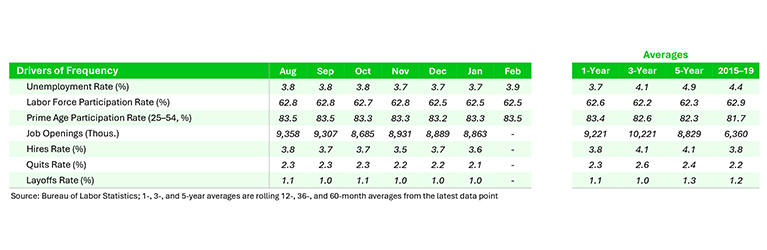

The March labor report was not all positive, though. The unemployment rate ticked up to 3.9%, while the labor force participation rate was unchanged.

The unemployment rate is derived from the household survey, while employment growth comes from the establishment survey. In March, the household survey reported a net loss of jobs, leading to an increase in the unemployment rate. It is not uncommon for the two surveys to move in opposite directions, and they have meaningfully diverged twice in the past four years.

The unemployment rate moved higher while labor force participation was unchanged. Despite strong employment gains reported from the establishment survey, the household survey has started to diverge, instead reporting a small loss of employment. Credit: NCCI

The unemployment rate moved higher while labor force participation was unchanged. Despite strong employment gains reported from the establishment survey, the household survey has started to diverge, instead reporting a small loss of employment. Credit: NCCI

Both previous divergences were eventually resolved with the household survey of employment moving higher to match the establishment survey. While this is not a concern yet, it is an area to watch in the coming months.

An evolving economy

We've talked for a while about the labor market dynamics in the wake of the pandemic as a "Great Reshuffle," with more job turnover and a smaller labor force due to reduced participation and immigration. This period has mostly come to an end. The quits rate returned to 2019 level in July 2023 and has trended near that level since.

Despite frequent media headlines, the layoffs and discharges rate has trended near historical lows in 2023, a trend that has continued into 2024. While hiring has slowed this year, workers leaving jobs both voluntarily and not have also dropped. Normalization of turnover and higher labor supply will likely put some downward pressure on wage growth in 2024.

Looking through a workers' compensation lens

The current labor market has several dynamics that the workers' compensation industry can consider positive. While employment growth has slowed, wage growth has remained elevated, boosting payroll growth and premiums for most industries.

Additionally, rising participation has increased labor supply, reducing the struggle for companies to find workers that fit their needs.

High turnover and fast hiring lead to a greater share of low-tenured workers, who tend to have higher injury frequency than longer-tenured workers. Slower turnover and a lower rate of hiring are reducing low-tenured workers as a percentage of the labor force over time. Further, an increased pool of available workers can increase the quality of hires, both of which can reduce frequency.

Moving towards balance

An optimally balanced labor market is one in which labor supply and labor demand are more closely aligned, compared to the extreme dislocation the pandemic caused.

Many people may think a rising unemployment rate is bad news for the economy, but that is not always the case. The unemployment rate can rise if people who have officially been out of the labor force start looking for a job again. Rising labor force participation was a key theme of 2023, particularly for prime-age (25- to 54-year-old) workers. This is why we saw a slight increase in the unemployment rate even as overall job numbers steadily increased.

As discussed above, employment and wage growth moderated in 2023 and job turnover fell close to 2019 rates. If these trends continue, then labor market indicators for 2024 will look more similar to pre-pandemic averages than to the recession and recovery periods that started in 2020.

Stephen Cooper joined National Council on Compensation Insurance in August 2023 as executive director & senior economist, leading the economic research and communications team, which focuses on economic developments impactful to the workers' compensation system. Prior to joining the NCCI, Cooper was vice president, senior economist, for Hartford Investment Management Company, a subsidiary of The Hartford. In this role, he oversaw economic research developing insights to drive alpha generation for portfolio management.

A version of this article originally appeared on the NCCI website.

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.