The property and casualty insurance market continues to achieve single-digit rate increases but analysts maintain there is little indication drivers are in place for a shift to a hard market.

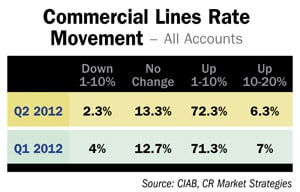

Towers Watson's Commercial Lines Insurance Pricing Survey, which compares second quarter prices this year to last year, shows that commercial-insurance prices in the aggregate increased by 6 percent during over that time. It is the sixth consecutive quarter aggregate prices rose for all commercial lines, says Towers Watson.

The consulting service says workers' compensation and commercial property experienced increases in the high-single digits, while directors and officers and employment practices liability price increases were in the mid-single digits—a “departure from the relatively flat pricing of the last two quarters.”

The consulting service says workers' compensation and commercial property experienced increases in the high-single digits, while directors and officers and employment practices liability price increases were in the mid-single digits—a “departure from the relatively flat pricing of the last two quarters.”

Recommended For You

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Breaking insurance news and analysis, on-site and via our newsletters and custom alerts

- Weekly Insurance Speak podcast featuring exclusive interviews with industry leaders

- Educational webcasts, white papers, and ebooks from industry thought leaders

- Critical converage of the employee benefits and financial advisory markets on our other ALM sites, BenefitsPRO and ThinkAdvisor

Already have an account? Sign In Now

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.