In recent months, the international community has witnessed one of the most volatile geopolitical periods in our history since the end of World War II. Even before the current conflict in the Middle East, the risks posed by political violence and civil unrest had been intensifying, evolving into global challenges that impact companies, communities, and the wider economy.

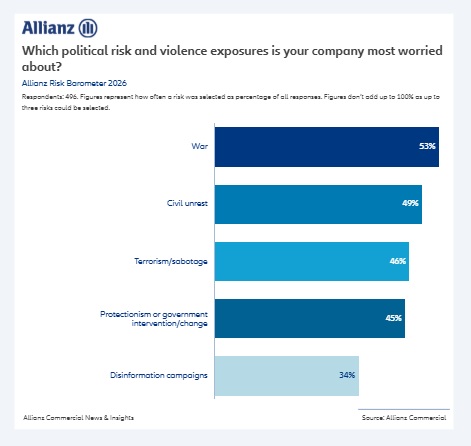

According to the latest edition of Allianz Commercial's annual political violence trends report, war has overtaken civil unrest as the political violence exposure companies fear the most, as conflicts in Europe and the Middle East disrupt global trade flows, strain political alliances, embolden adversarial powers, and heighten risks to business assets. Below are some of the main drivers and dynamics that are reshaping the global risk landscape. As we navigate this era of heightened uncertainty, understanding the implications of these risks and mitigating them in our interconnected business ecosystems has never been more critical.

Conflict impact in the Middle East

The repercussions of the U.S. / Iran conflict on the political violence and terrorism (PVT) risk landscape are significant. Notwithstanding the human toll of the conflict, the PVT insurance market in the Middle East has been severely impacted, with losses concentrated in key sectors like oil, gas, and transportation. Damaged infrastructure could take years to repair. The region's risk assessment has shifted to medium-to-high, with some industries now considered high to extreme. The loss quantum has the potential to result in a costlier event than PVT claims resulting from the war in Ukraine. Heightened risk of strikes, riots, and civil unrest may be expected, particularly in countries heavily reliant on Middle Eastern oil, gas and fertilizers.

Blurred lines in the gray zone

Meanwhile, in the 'gray zone' between peace and open warfare, threat actors are leveraging technology, criminal networks, and disinformation to attack critical infrastructure, businesses, and individuals, blurring the lines between state and non-state actors while undermining detection efforts. Since Russia's invasion of Ukraine in 2022, it is reported Europe had witnessed 145 incidents of sabotage up until the end of 2025, with high-profile brands and symbolic sites frequently the targets. Drone incursions have disrupted European airports, and undersea cables have been damaged in the Baltic and Red Seas, for example. Gray zone' activities carried out by Iran-sponsored perpetrators are expected to increase in the wake of the US / Iran conflict, including in the cyber space, where exposures are intensifying, particularly for businesses perceived to be supporters of the US.

Multiple drivers fuel civil unrest

Across the world, deteriorating social cohesion is fueling civil unrest, with protests triggered by economic, political, and social grievances. Allianz Research has tracked around 250 reported strikes, riots, and civil commotion (SRCC) events between 2020 and 2025 with active participation exceeding 1,000 people and lasting for more than one day. Pakistan experienced the most events, followed by Indonesia. Other countries that experienced higher numbers of events include the US, Greece, Tunisia, Hungary, Iran, and India. For businesses, strikes, road blockades, demonstrations, and localized violence can disrupt logistics and cause business interruption.

Terrorism falling but this trend could be reversed

Terrorism declined globally in 2025, but surged in the West, fueled by polarization, antisemitism, Islamophobia, and far-right activities. The war in Iran has intensified terror risks, with Iran-linked groups operating through the Islamic Revolutionary Guard Corps (IRGC), sleeper cells, and proxies. The impact of actions by Israel and the US in Iran and Gaza could further fuel radicalization, potentially translating into violence, while extremist groups in sub-Saharan Africa continue to exploit security vacuums.

Risk mitigation and insurance implications

The U.S. / Iran conflict is likely to have a significant impact on risk mitigation moving forward. Prior to the conflict, Allianz analysis showed that just over a third (35%) of companies were already exploring near-shoring and evaluating domestic manufacturing options, 32% were looking to improve inventory management, including storing inventory in Free Trade zones, and almost half (49%) were looking at renegotiating and diversifying supply chains, as strategies to adapt to shifting geopolitical risks. Such trends will likely be accelerated by the conflict. At the same time, demand for political violence insurance continues to grow.

To read the full report, please visit: Political violence and civil unrest trends 2026 | Allianz Commercial

By Srdjan Todorovic is Global Head of Political Violence and Hostile Environment Solutions at Allianz Commercial. This article is published with permission from Allianz Commerial and may not be reproduced.

(Featured image credit: Adobe Stock/Duncan Noakes)

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.