Insurance is a hedge against uncertainty, but uncertainty also makes risk more difficult to measure. (Credit: lucadp/Adobe Stock)

Insurance is a hedge against uncertainty, but uncertainty also makes risk more difficult to measure. (Credit: lucadp/Adobe Stock)

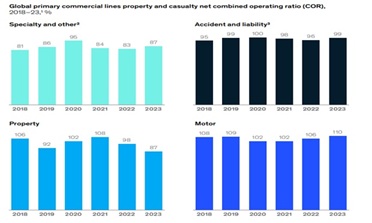

In decades to come, commercial property and casualty (P&C) insurers may look back on the past five years as the good old days: premiums increased an average of 8 percent of year, and profits rose.

There are signs, however, that the good times may be fading. Global composite rates were flat in the second quarter of 2024 for the first time in almost seven years.

Another shadow is the risk that the commercial P&C industry is losing relevance. One indicator is the widening protection gap. For natural catastrophes, the difference between global economic losses and insured losses grew from $181 billion in 2022 to $262 billion in 2023. For cyber threats, as much as 99 percent of costs are uncovered. Another indicator is that a significant number of entities are simply not signing up. In Britain, more than half of small businesses have stopped buying at least one insurance product; in the United States, 75 percent of small businesses are underinsured.

The implication is that insurers can no longer rely on continually rising premiums to prosper. In fact, the McKinsey analysis found no clear correlation between growth and profitability. Simply being in the right place is no guarantee, either. When McKinsey analyzed the performance of global commercial P&C insurers over the past decade, it found that 40 percent of performance is accounted for by the lines of business those carriers participate in.

How well companies operate determines the other 60% of performance.

In short, while portfolio management matters, and the secret to sustained success is to execute targeted strategies that deliver value at an acceptable level of risk. That is what investors want, and what the market rewards.

How, then, can insurers raise their game?

Here are three priorities.

- Modernize underwriting. The leaders in the peer set of insurers we reviewed, defined as the top 25 percent by combined ratio, had loss ratios six percentage points lower than the rest, in part because they simply invested more. Specifically, the leaders tap into a wide range of data sources, such as tax assessments and satellite imagery, and then apply artificial intelligence (AI) and machine learning to produce sophisticated risk models. The result is that they create distinctive, high-quality decision-making capabilities that can be readily adapted and scaled up. Generative AI is just getting started, but we expect the leaders will make swift progress to use it to automate algorithmic underwriting, improve the submission process, and streamline market intelligence.

- Drive down acquisition costs. The leading insurers cut their acquisition expense ratio by two percentage points since 2013; among the laggards, the ratio rose two percentage points. In this context, it is difficult to overestimate the importance of good relationships with brokers. Insurers should think about the value-added services they provide brokers, such as marketing and sales support, and invest in those capabilities. Digital connectivity is one such capability. Digital trading platforms are expanding across commercial lines, connecting clients with coverage solutions in a few clicks. Third-party providers are also joining in, equipping both brokers and insurers with new ways to find new business. Insurers who develop this expertise will find it easier, and cheaper, to acquire new customers.

- Invest in efficiency. Global insurers have cut their administration expense ratios over the past decade, but the leaders did better. That is one way of looking at it. Another is that, after normalizing for both rate increases and inflation, administration expense ratios are actually higher than they were in 2018. This could cause problems if rates soften, and expense ratios rise. Fortunately, technology exists to do much better, and more is coming. AI-enabled chatbots, for example, are already streamlining customer service, claims management, and the processing of broker submissions. Less commonly, AI engines are assessing claims and then assigning them to adjusters, in order of priority. Such use cases are certainly helpful. The greater potential, though, is from creating an efficient, flexible operating model that is designed to works in concert with the profitable growth strategy.

James Polyblank is a partner in McKinsey & Company’s London office. Holger Wilms is a senior partner in Washington, D.C. This article is published with permission from McKinsey & Company and may not be reproduced.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.