The composite rate for October was plus 4 percent as compared to plus 5 percent in September. Several significant adjustments were recorded in October.

The composite rate for October was plus 4 percent as compared to plus 5 percent in September. Several significant adjustments were recorded in October.

Small accounts and commercial property rates decreased from plus 6 percent to plus 4 percent.. Business owners' policies (BOP) rates decreased from plus 5 percent to plus 3 percent. The largest downward adjustment was in general liability coverage, which was down from plus 6 percent to plus 3 percent.

The market adjustments drew these comments from MarketScout's CEO, Richard Kerr, “The upward trajectory of rates certainly lost some steam in October. The general liability results are significant because this coverage is offered by a large percentage of both the admitted and non-admitted marketplace. We will watch closely to see if more aggressive pricing creeps into other lines of coverage through the end of the year.”

Five coverages measured rate reductions: property, BOP, general liability, D&O and EPLI. Commercial auto was the only coverage with a rate increase at plus 6 percent as compared to plus 5 percent the month before.

By industry class, contracting and habitational rates were lower than the preceding month.

Rates for accounts measured by size all remained the same as posted for the prior month with one notable exception. Small accounts ($0 to $25,000 premium) moderated from plus 6 percent to plus 4 percent.

The National Alliance for Insurance Education and Research conducted pricing surveys used in MarketScout's analysis of market conditions. These surveys help to further corroborate MarketScout's actual findings, mathematically driven by new and renewal placements across the United States.

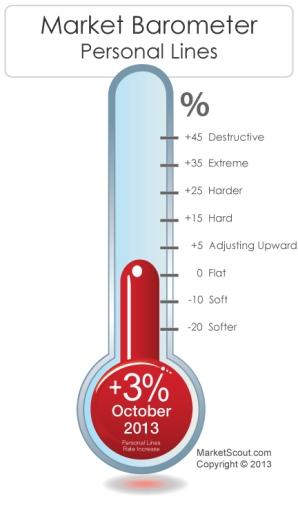

PERSONAL LINES

As the 2013 hurricane season comes to an end, US personal lines insurers are beginning to relax pricing. Homes under $1,000,000 and automobile exposures were assessed lower rate increases in October as the overall rate for October was plus 3 percent compared to plus 4 percent in September.

Kerr says, “Homeowners and auto coverages on traditional accounts are enjoying premium reductions largely due to little catastrophe activity, but the high value personal lines market actually assessed a month on month rate increase on their insureds. We expect the difference in pricing among traditional vs. high value accounts is due to the fact that high-net-worth insurers provide significantly broader coverages, which ultimately result in more claims. Many of these type of claims would not be covered by traditional markets. Thus, the need for a little higher rate.”

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.