Insurance companies and trade groups continue to appeal to state regulators over the decision made by nine jurisdictions to prevent insurers from imposing hurricane deductibles for losses suffered from Superstorm Sandy.

Insurance companies and trade groups continue to appeal to state regulators over the decision made by nine jurisdictions to prevent insurers from imposing hurricane deductibles for losses suffered from Superstorm Sandy.

New York, Rhode Island, New Jersey, Delaware, Massachusetts, Connecticut, Pennsylvania, Maryland and the District of Columbia declared the hurricane deductibles invalid after the National Weather Service (NWS) reclassified Sandy as an “extra-tropical cyclone” before the storm made landfall in the Garden State on Oct. 29.

But representatives of the trade groups and carriers are telling state regulators that they based their rates on the contract language they negotiated with those states and that they are concerned about Sandy's potential to threaten their solvency.

“Insurers are committed and ready to help our policyholders recover from this terrible disaster,” says Willem Rijksen, vice president of public affairs for the American Insurance Association. But, he adds, “let's remember that it's absolutely essential that we support certainty and a robust, competitive private-insurance market for coastal residents in the years to come.

“Political manipulation of private markets weakens those markets—and that's the last thing coastal residents need,” Rijksen adds. “We want to work with regulators to help our policyholders recover.”

Donald Griffin, vice president of personal lines for the Property and Casualty Insurers Association of America, says insurance companies and their trade groups have been working with regulators to establish the rules when settling claims on Sandy.

“Whether windstorm, hurricane or standard, we want to make sure the deductibles are applied fairly and according to the terms of the contract,” Griffin says. He adds that insurance-policy contracts may differ by state and whether the contract calls for a deductible based on a windstorm or hurricane trigger.

Neil Alldredge, senior vice president of state and policy affairs for the National Association of Mutual Insurance Companies (NAMIC), says the ultimate impact from the decision will likely be higher insurance rates for everyone—and another rethinking by carriers as to how much coastal risk they can afford to underwrite.

“These deductibles are important risk-management tools,” he says. “An insurer makes decisions on the coastal property it will underwrite based on these practices.

“These deductibles are important risk-management tools,” he says. “An insurer makes decisions on the coastal property it will underwrite based on these practices.

“We acknowledge that it will change the out-of-pocket costs for a person with a loss,” Alldredge adds, but “insurance companies need to rely on the certainty of the policy language. To determine, after the fact, that the language is not enforceable alters the economic decision-making that a company can make.”

Post-Sandy, the risk profile for certain areas now changes substantively—and that impacts the costs an insurer anticipates it will absorb if an event takes place.

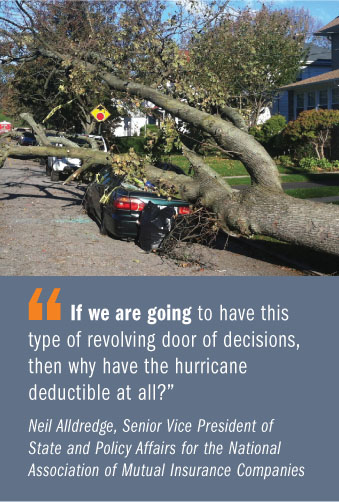

“That is the situation we are dealing with now,” Alldredge says. “If we are going to have this type of revolving door of decisions, then why have the hurricane deductible at all?”

Alldredge notes that the issue first arose last year, when Hurricane Irene came ashore. “This is what spawned the controversy, in most cases, in the same states,” he says.

The difference is that Irene was a hurricane, and the NWS did not change the designation before it hit land. In Sandy's case, he adds, “you have this phantom decision just before landfall that all of a sudden this was not a hurricane, even though it walked like a duck and quacked like a duck.”

The only state to classify Sandy as a hurricane was North Carolina, because the NWS was still considering it a hurricane when the state sustained damage.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.