What makes an IT executive stand out as one of Tech Decisions' Insurance IT All-Stars? For six years we have been handing out these accolades and the single factor that binds all of our all-stars over the years is their ability to address problems and—through collaboration—bring people, and processes, and technology together to determine the best solution.

The 2012 group is no different. Some have similar backgrounds; others do not. We have personal lines carriers, specialty lines, and even a life insurer. What makes this particular group stand out alongside any of the previous groups of all-stars we've selected is they are unafraid to admit they don't have all the answers, but they do have the inner strength, talent, and expertise to find the best possible solutions and initiate them into their corporate environment.

This year's list includes Rich Pedersen, senior vice president and CIO of National Life Group; Rick Roy, senior vice president and CIO of CUNA Mutual; Bryan Fowler, vice president and CIO of Oregon Mutual Group; Thad DeBerry, senior vice president and CIO of Western World Insurance Group; and Peter Moreau, vice president and CIO of Amica Insurance.

We believe you will find they all have interesting stories to tell about their experiences in insurance IT and that you'll agree they deserve the title Insurance IT All-Star

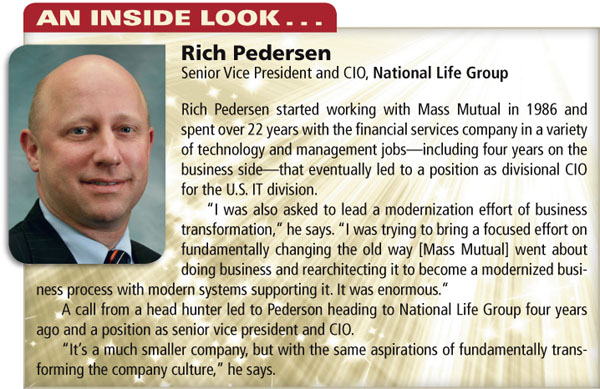

RICH PEDERSEN

RICH PEDERSEN

Senior Vice President and CIO, National Life Group

Rich Pedersen started working with Mass Mutual in 1986 and spent over 22 years with the financial services company in a variety of technology and management jobs—including four years on the business side—that eventually led to a position as divisional CIO for the U.S. IT division.

"I was also asked to lead a modernization effort of business transformation," he says. "I was trying to bring a focused effort on fundamentally changing the old way [Mass Mutual] went about doing business and rearchitecting it to become a modernized business process with modern systems supporting it. It was enormous."

A call from a head hunter led to Pederson heading to National Life Group four years ago and a position as senior vice president and CIO.

"It's a much smaller company, but with the same aspirations of fundamentally transforming the company culture," he says.

In defining an insurance company's culture, Rich Pedersen, senior vice president and CIO of National Life Group, believes it is important to understand what the existing culture is, what are the norms of the people working for the company, and what are the structures those employees work within.

Coming to National Life four years ago, one of Pedersen's mandates was to change the culture around IT within the carrier. There were some sidesteps brought on by forces more powerful than he, but Pedersen is progressing toward that goal.

"You can't just transform any one area alone, whether it is process, culture or systems," he says. "You have to create a unifying message of transformation to get people to understand there is a larger purpose for which you are about to lead them through—including a bunch of painful changes—and then lay out the steps."

It's a slow process in the beginning, but Pedersen believes it builds momentum through constant communication about the rallying call. It helps that Pedersen has spent time on the business side and has worked to share that knowledge within IT and with his business partners.

"The ability to relate to the business—how money is paid, how distribution works, and following the dollar—is imperative," he says. "IT, in a financial services organization, isn't for the sake of IT. It's to help bring value to the business so you can go to market more efficiently and service your client more effectively. It is fundamental to being successful as a CIO."

Pedersen came on as CIO at National Life just as the financial crisis played havoc with the life insurance industry. Looking back on 2008 and 2009, Pedersen today can reflect on what a valuable learning experience it was for him and the industry.

Pedersen came on as CIO at National Life just as the financial crisis played havoc with the life insurance industry. Looking back on 2008 and 2009, Pedersen today can reflect on what a valuable learning experience it was for him and the industry.

"To think I had the opportunity to be at the helm with a peer executive group to navigate probably the most tumultuous time since the Great Depression was an opportunity of a lifetime," he says. "You can only call it an opportunity in hindsight, though. When I was brought on it was to deal with the strategic initiatives that we were going to build on for the next three to five years. We were going headlong down that path, assessing the strategic competitiveness and the strategic differentiation of our organization, creating a vision mission statement, creating the overall three-year strategy for the corporation."

When the crisis hit, though, it was "all hands on deck" throughout the financial services industries, points out Pedersen.

"At that point it was a time to be supportive of the new mission over the short run," he says. "We made as much progress as we could on the legwork. We knew we were going to come out of the crisis and we actually turned a profit in all years—including 2008 and 2009."

It was not a time to focus on new IT initiatives, but it was a time to focus on the IT division, which hadn't been functioning at the highest level, according to Pedersen.

"We instilled a lot of rigor knowing the pace of execution was going to go up in the coming years," he says. "Many of the things we knew we needed, we started building at the end of 2008 and through 2009. We launched into strategic initiatives in 2010. These last three years have been the build-out from a much more solid foundation within IT."

Pedersen believes the industry hasnow reached an extraordinary time in the insurance business.

"We're at an inflection point," he says.

Insurers have an aging, imbedded base of insurance producers and a buying public that is younger and savvier about technology.

"The up-and-coming middle class and the emerging affluent—younger people making money and buying houses—have grown up around a technology-oriented lifestyle," says Pedersen. "They are people that have never known anything else but to have a computer and information at their fingertips. The whole notion that insurance is sold and not bought is in flux right now."

Pedersen describes the insurance world today as at a pivot point where these young information gatherers are beginning the sales process themselves. They are doing the research on financial services and what they should be doing at life-cycle points and they are not interested in having sales people conduct a transaction in their house.

"You need to prepare your IT organization and your operations centers for that change and how the transaction life cycle will be conducted using technology such as social media, multimedia, information sharing, browsing technology, search engine optimization, and Skype for the interview process," he says.

Cybersecurity is Pedersen's biggest worry for the future.

Carriers need to remain diligent and try to stay in front of what the bad guys are thinking. He points out that the more information that becomes available, the more bad guys want to get their hands on it.

The trend today is for insurers to conduct more business through electronic transaction, which calls for far more security.

"When business was done with a handshake and a pen and submitted to the back office, the availability of the financial transaction wasn't as great," says Pedersen. "The opportunity didn't exist as much for it to be corrupted. The more business is conducted in a public medium, the more you have to be diligent about how you secure it. Ensuring you have the appropriate built-in redundancy, fault tolerance, and disaster recovery is always a challenge."

RICK ROY

RICK ROY

CIO, CUNA Mutual Group

After graduation from the University of Wisconsin–Milwaukee, Rick Roy spent the first 20 years of his career building, selling, and deploying software and processing solutions for companies serving the banking industry.

Eight years ago, Roy made the switch to a corporate IT role with CUNA Mutual Group as the carrier sought to add business focus to its IT operation. Roy has served two stints as CIO for CUNA Mutual, sandwiched around a three-year stint running the carrier's operations.

"About three-and-a-half years ago they asked me to come back to the CIO seat," he says. "I was able to come back and get some things right that I hadn't gotten right the first time. That's a rare opportunity."

CUNA Mutual serves the credit union industry and its members.

"We have a broad product portfolio, but we're very focused on a certain market," says Roy.

Roy oversees about 500 employees—most of them in the insurer's home office in Madison, Wisc.—and another 300 or so contractors on any given day.

"Between here and our offshore partners we have about 800 people doing something with IT every day," he says.

After two decades working on the vendor side, the opportunity to run an IT shop for himself was a big part of the attraction Rick Roy found in joining CUNA Mutual Group nine years ago. Roy, the carrier's senior vice president and CIO, is running IT again after a three-year stint as director of operations and he's happy to be back.

"The company was looking to elevate IT to more of a shared service as it has grown," he says. "It's an interesting time [to be in IT] with all the mobility and consumerization going on in the technology world. It's also been fascinating being back in the CIO seat."

CUNA Mutual Group serves credit unions and its members. The carrier has a B-to-B side with products and services provided to credit unions, according to Roy, and a consumer side with products provided directly to the members of credit unions.

With so many products and business lines to offer, Roy maintains the top challenge he faces is maintaining a critical eye on what's scalable and what isn't.

"It's not that everything has to have huge scale, but there are a lot of things that aren't going to get to a scale and you have to ask yourself if you are OK with that," he says. "It's a continuous process because we manage complexity that is larger than our company size would lead one to believe."

Keeping costs in check is part of the challenge, but so is getting his arms around the number of products CUNA Mutual offers.

"It's difficult to become an expert in all of them, but the premium for me is having a strong senior staff," Roy says. "Their ability to develop a deeper expertise is important. There's just no way from the CIO seat that you are going to learn all those different businesses with any level of depth. It affects how you think about organization, structure, and leadership roles."

The financial crisis of 2008 was challenging for the banking industry and credit unions were also impacted in much the same way the community banking business was hurt, according to Roy.

"The core mission for credit unions is to make good loans to members of the credit union," says Roy. "When the economy stumbles as hard as it did in 2009, the lending volume dries up. That's a huge source of their income and a big part of their value proposition."

Fortunately, CUNA Mutual Group is a well-capitalized company and the struggles its core market faced didn't cause major damage.

"We're a mutual at a time where it's nice to have a mutual structure so you can keep your long-term mission in mind," says Roy. "Nonetheless, we were not immune. We have a large investment portfolio like all insurance companies do and we had some challenges. We've bounced back and some of that is the power of having a diversified product portfolio."

CUNA Mutual was forced to reduce IT spending in 2009.

"How do you do that in an intelligent way and balance that with the fact the technology world was changing dramatically," he says. "We stepped back to do a hard assessment of where we could take our costs without creating bigger, longer-term issues for ourselves and by the same token create some investment money because the world was changing and we couldn't stand still or the user community would blow right past us."

Roy believes the set of choices CIOs have today is exciting as well as challenging. How the carrier supports some of the cloud-based solutions that enable internal customers to get a new solution faster is among those challenges.

"Cloud-based solutions present new and different ways for us to get solutions and business value quicker," he says. "Over 30 years now, I've watched IT add tremendous value to business but it also can become a drag to business. If it is too slow a solution or the quality isn't there, the negative impact on the business trying to execute strategy is enormous. You have to get it right."

Figuring out what solutions can work is hard—but rewarding—work.

"I think trying to piece together where we are headed over the next five years is where it gets interesting," says Roy. "How do you view your application portfolio? Does 50 percent of more of it go into the cloud? It could be higher for some organizations. It also has big implications for talent. What do you need in house? How do you cultivate that through the system?"

Finding IT talent is a worry Roy shares with many technology leaders.

"There's almost a perfect storm in terms of finding IT talent that's hitting the U.S. right now," he says. "You have a lot of the Baby Boomers starting to think about retirement. On the other hand, we don't have enough new graduates in IT coming up through the U.S. educational system. The third part of the storm is you have immense change going on in technology. That isn't new—the field is always changing—but game changers like consumerization, cloud options, and certainly the way we all run data centers today is quite different from what many of us used to do."

For mid-tier insurers such as CUNA Mutual, the vendor landscape and consolidation in the vendor world is problematic and Roy believes it will continue in that direction.

"When you don't have enormous scale in terms of buying power, it makes negotiating contracts very tricky," he says. "We have a large vendor ecosystem that we use to deliver IT. We watch those dynamics very closely. I came from that world, but as the guy that signs those contracts, I'm mindful of where you have leverage and where you don't. In the past five or six years there has been substantial consolidation. That's nice for the vendor cash flow, but not necessarily a strong value proposition for the buyer."

THAD DEBERRY

THAD DEBERRY

Senior Vice President and CIO, Western World Insurance Group

Thad DeBerry went to college to study business and it was his father that convinced him that computers were the way of the future. So DeBerry went to the Chubb Institute to learn the IT ropes.

"It was a great place to go to get started with a career," he says.

DeBerry ended up in the insurance sector for all but two years of his business career. He was with Everson National when the CIO of Western World Insurance Group retired and DeBerry was selected as his replacement in May of 2003.

Western World is an E&S insurer operating in 48 states. The carrier also has a commercial auto book of business that it writes in 28 states.

"It was an interesting opportunity with an interesting organization," said DeBerry.

Thad DeBerry is excited about the future of insurance technology because of the many opportunities that exist.

"There is so much untapped opportunity right now to improve the business," says DeBerry, senior vice president and CIO of Western World Insurance Group. "Maybe more than anything else in the last couple of years, technology has the ability to transform an organization and change its future like nothing else. Having the ability to make and see that kind of impact and drive a company forward through growth and reach a new level of profitability is pretty exciting."

Technology also brings with it huge challenges, according to DeBerry.

"Things are changing rapidly, so taking that rapid technological change and applying it to real-world insurance solutions is a huge challenge," he says. "There are cultural issues as well. Some segments of the industry are staid and steeped in tradition, so it's a challenge to break through that."

"Things are changing rapidly, so taking that rapid technological change and applying it to real-world insurance solutions is a huge challenge," he says. "There are cultural issues as well. Some segments of the industry are staid and steeped in tradition, so it's a challenge to break through that."

A carrier's integration of third-party data and services is the next big frontier in terms of the competitive space for excess and surplus lines (E&S) insurers such as Western World, explains DeBerry.

"We're trying to make a transaction seamless and encompass all the functions to make the transaction complete—from inspections to getting third-party data for vehicles or property, all the way through auto processing," he says. "There is a lot of opportunity to make things more seamless and bring all the data onto one platform."

Surplus lines typically falls behind the curve when it comes to technology, which DeBerry attributes to the nature of the business.

"It's not easy to plug something in and have it work," he says.

Western World has been around for nearly half a century, but it was only four years ago that the carrier determined that change was in order.

"In 2008 we looked at the surplus lines marketplace and Western World's place in it," says DeBerry. "What was fascinating about the detailed report we prepared was that one of the biggest drivers for where people place business through a wholesale distributor is ease of use. That's something that was never really considered, certainly for Western World and by and large for the entire surplus lines industry."

Western World started on a technology upgrade and integration was one of the major keys to the project, according to DeBerry. In 2010, the carrier implemented the Western World Integrated Platform, a full-functioning underwriting guide with rules, rates, rate-quote-bind-issue, endorsements, renewals, and a portal for wholesale agents, which allows some of the functionality to be extended to their retail agents and even to insureds.

"When we built this, integration was the key," he says. "We've got hooks into every underwriting function where we can expose our functionality through web services. It's seamless where our rating or our policy issuance can be dropped into an MGA's environment so they can leverage the maintenance we are doing and the logic that we've put together."

The carrier also built in some upload/download of data into some of the common agency management systems, which DeBerry points out is more typical for admitted lines carriers than for those operating in surplus lines.

"Straight-through processing is something that admitted carriers have been much further along with for years," he says. "We were able to bring a lot of that functionality and ease-of-use into the non-admitted world."

Flexibility is the key to the new system, explains DeBerry. Western World built in the ability for MGA underwriters or Western World's underwriters to customize by risk and built the workflow around that.

For the most part, Western World built the new platform internally. A key to the platform's success was the amount of time DeBerry and the company's lead underwriter spent upfront talking with MGAs and working on the design.

"We did a fairly extensive look at the vendor marketplace and there just wasn't anything that had the specific needs we were looking for," said DeBerry, citing integration, underwriting, and the flexibility that the carrier required.

DeBerry, like many in IT, is concerned with the future of the operation.

"Are there enough people to assume seats at the head of the table when it comes to technology and the insurance industry?" he asks "There are tremendous opportunities and a big need for us to prepare the next generation. Finding people who have enough of that technology experience and marry it with the business is hard to do. We're forced to change our resource pool a bit where the business analyst role is growing out of necessity. A lot of organizations are going that way."

PETER MOREAU

PETER MOREAU

Vice President and CIO, Amica Insurance

Peter Moreau started with Amica out of college, 26 years ago. He began his career in the technical services area, doing jobs such as mainframe systems support and networking.

"I focused more on technology and less on business applications early in my career," he says.

Moreau moved into various levels of management—project management, team management, overseeing development areas—right up to his current role of CIO, where he landed two years ago.

Amica Insurance is a mutual company and a direct writer of personal lines products, licensed in 49 states. Moreau oversees 290 people in the IT department. The company operates 39 branch offices around the country, but all of the IT operations are run out of the carrier's home office in Lincoln, Rhode Island.

Peter Moreau, vice president and CIO for Amica Insurance, has risen through the technical ranks in an IT career that started following his graduation from college. His technical background made new technology initiatives exciting for him, but as he has matured into an IT leader so has his focus.

Today, Moreau's excitement comes from creating a shared vision with Amica's business leaders and developing a plan that will fulfill that vision.

"Laying out the roadmap and seeing that plan come to fruition is exciting," he says. "It changes your focus because most of what I need to do as CIO is coordinate resources and use them in a fashion that will benefit our policyholders. As a mutual company, we're in business to serve our policyholders. Everything we do—the timeframes we take to do it, how much we spend—is focused on making sure it is beneficial to our policyholders."

Amica built its policy system from scratch using mainframe technology, and the system has been in place for over 30 years.

Amica built its policy system from scratch using mainframe technology, and the system has been in place for over 30 years.

"It is a highly functional system," says Moreau, "but has become more difficult to manage from a skill-set perspective. Universities are not producing Assembler or COBOL developers these days."

Amica's business leaders also sought increased functionality that, Moreau explains, would be best served from some of the newer systems available in the software solution marketplace. Amica chose the Guidewire systems, first with ClaimCenter, which they began with in 2005, and now with PolicyCenter.

"We completed a project called the Electronic Claims File which took a paper-driven claims process and automated the flow of information as well as the documents," says Moreau. "That was our first major modernization project. Following that we began to assess our policy systems to see where we would go with those."

The older Amica systems had been continually enhanced over the years, according to Moreau.

"Typically, we would add new function without taking a holistic view of the whole application flow," he says. "The system has become difficult to use and it is hard to train people, so some of the drivers from the business view were to shrink training time and improve the ease-of-use of the system. From an IT perspective, the goals are related to skills advancement and systems knowledge transfer. Moving our staff from legacy languages and processes to modern languages and agile methodologies better positions us to support these systems going forward where training and new skills are being driven. It's given us a chance to take a fresh look at the applications and skill sets—build them out on a modern technology framework."

The newer systems give Amica a better perspective on the future, explains Moreau.

"Our older systems served us well but had the potential to hamper us from going forward," he says. "Now we are putting foundational pieces in place that not only support our internal customers, but also support our customers on the website and mobile applications. We are putting things in place that will take us where we need to go in the next five to 10 years."

As for future business plans, Moreau explains Amica is still formulating its mobile strategy. The initial focus of the carrier's mobile apps was on claims reporting with a few side benefits.

"We also launched a mobile website enabling some key transactions such as bill pay and ID cards formatted for the smaller user interface of a smartphone," he says. "A key thing is that we are still tying back to our existing systems to support [mobility]. We do the integration work so the data and functionality go back into the core system. That positions us well going forward to support what our customers are expecting. They want the same level of service whether on the phone or on the web or on a mobile device."

With a strong technology background, Moreau felt he needed a better grasp of the business side to be able to participate and add value to the conversations as he moved up in the management ranks. He achieved the CPCU designation to get a better understanding of how insurance companies operate and earned an MBA to obtain general business knowledge that went deeper into finance and leadership skills.

"Amica supported me throughout those efforts," he says. "The company puts a heavy focus on developing employees. If you have a good employee base and treat them well, customer service is born out of that, especially for a direct writer."

The concern Moreau has for the future involves where Amica—and other carriers—are getting future IT workers.

"If you look at the universities and who is graduating in the disciplines we focus on—more of IT with a business slant—the number of students has shrunk over the years." he says. "And the competition between businesses for those students has been and will continue to be heavy. We are feeling it a little bit now, but I don't see it clearing for the future. That's a concern shared by many CIOs."

In recent years, Amica has addressed the issue by working with local schools and running an internship program, which is how the carrier traditionally gets many of its new hires. Amica brings in students in the summer before their senior year and works with them throughout the year.

The concern is heightened by what Moreau and others are calling the greying of IT.

"It will be a challenging time, but I believe we have the right management team in place, and our staff is receptive to the variety of alternative staffing options we are deploying to support all the projects we have on our plate," he says.

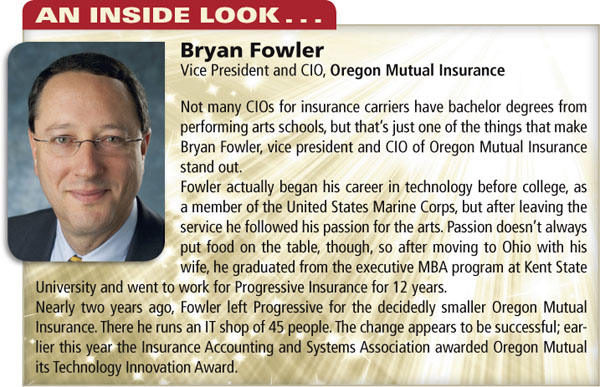

BRYAN FOWLER

BRYAN FOWLER

Vice President and CIO, Oregon Mutual Insurance

Not many CIOs for insurance carriers have bachelor degrees from performing arts schools, but that's just one of the things that make Bryan Fowler, vice president and CIO of Oregon Mutual Insurance stand out.

Fowler actually began his career in technology before college, as a member of the United States Marine Corps, but after leaving the service he followed his passion for the arts. Passion doesn't always put food on the table, though, so after moving to Ohio with his wife, he graduated from the executive MBA program at Kent State University and went to work for Progressive Insurance for 12 years.

Nearly two years ago, Fowler left Progressive for the decidedly smaller Oregon Mutual Insurance. There he runs an IT shop of 45 people. The change appears to be successful; earlier this year the Insurance Accounting and Systems Association awarded Oregon Mutual its Technology Innovation Award.

For many people in IT—particularly those in the insurance industry—a job with Progressive Insurance is considered a dream opportunity because of the value the carrier places on technology.

Bryan Fowler, who spent 12 years with Progressive before moving to Oregon Mutual Insurance, described the experience as like working for a start-up company within a successful business.

"It was a lot of fun; a lot of energy and a lot of high-tech talent and focus," he says. "Especially the start-up of the Internet business. That was my gig for a long time."

Nearly two years ago, though, Fowler left his position, having been a director of IT at Progressive, to try something new.

"I had a good 12 years at Progressive, but when you are with a big company like that—even if you rise up to a high level—it's still a niche job," he says. "The culture changed and it wasn't as rewarding as it used to be."

Fowler went from being part of a respected IT department—with 3,000 people—to an Oregon Mutual IT shop that has 45 people and didn't have a good reputation within its own four walls.

Fowler went from being part of a respected IT department—with 3,000 people—to an Oregon Mutual IT shop that has 45 people and didn't have a good reputation within its own four walls.

"IT did not have a very good relationship with the business because we weren't delivering," says Fowler. "Part of the problem was we said 'yes' to everything and when you do that you're really saying yes to nothing because you can't deliver everything."

Fowler didn't believe Oregon Mutual's IT personnel were the source of the problem, but he felt IT had to become more responsive and a better partner with the business. The business also had to recognize that they are part of the equation, he adds.

"You can't keep changing priorities," he says. "There's also a thing called supply and demand. No one had ever talked about that because IT kept saying yes, but there are only so many people working in IT. We introduced prioritization, supply and demand, transparency, and began business conversations. It's not all fixed but it's a lot different than it was."

One of the first steps was to envision and start laying down an enterprise data architecture, according to Fowler, something that is being accomplished with the help of a vendor partner, Millbrook. Fowler believes this will be the foundation of everything the carrier does going forward.

"Data is at the center of our business. We will have an enterprise data architecture now so we won't have tangled systems; they will talk through data and services," he says. "Whenever we want to do something new, we have a buy vs. build vs. cloud vs. outsource decision to make and using data as our connector makes those decisions flexible. We will have more choices, more agility, and faster speed-to-market. We have to be more agile so if we don't like a certain technology or want to get into a new line of business we can make changes because the data allows us to."

Fowler explains that Millbrook and Oregon Mutual developed a plan to get important data into the hands of Oregon Mutual's marketing staff so when they visit the offices of their independent agents, the discussion turns to how the two sides can improve business for each other.

The Oregon Mutual marketing staff is now armed with iPads and a mobile app called MiAgents that puts agent performance data into their hands and highlights key action items.

"We never had true business conversations with the agency channel," says Fowler. "We sell exclusively through independent agents and they don't want us to waste their time. MiAgents puts the business partnership with our agents front and center. On the flip side, we take what were formerly known as trip reports and turn them into quantifiable analytical information."

As Oregon Mutual and Fowler look at the technology tools they need, Fowler admits he has become a fan of cloud computing.

"My first order of business when I look at the next thing we need to take on is what is out there on the cloud," he says. "A lot of companies are nervous about the cloud and for good reasons. I recognize the same land mines, but I have seen how it can work very effectively. It takes a lot of detailed work and planning, but it can work. I have less angst about the cloud."

The issues can be worked out if carriers have the right partners, technologies, and controls, points out Fowler.

"It's an interesting challenge for companies our size. We don't have much in the cloud now, but we will going forward."

What lies ahead for Oregon Mutual is executing its plans, finding innovative ways to execute them, and going beyond modernization to what Fowler calls "futurization."

"It's too late to catch up," he says. "We must leapfrog. MiAgents is the beginning, but there's some great stuff still to do."

Oregon Mutual also is making some investments in the IT staff.

"When I came here, no one had the word 'test' or 'quality' in their job title. We never had real project management," says Fowler. "I'm investing in some key positions in IT."

Oregon Mutual is located in McMinnville, Ore., 35 miles southwest of Portland, and Fowler explains that finding talent is one of the biggest challenges he faces.

"It's not just getting people to McMinnville that's a problem," he says. "It's finding strong talent to begin with. I've got a lot of résumés across my desk, but because we're small we can't just hire an average player."

Making the adjustment is also a factor when selecting technology partners as well.

"At Progressive, vendors clamored to get on my dance card," he says. "Big budgets attract vendors, of course. Now I call and tell them I'm from Oregon Mutual and they say, "Huh?"

Fowler is joking there.

"It's not that bad," he says. "We've had some good luck in selecting partners, but we have to be creative about it."

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.