Politicians, bureaucrats and industry associations kept our D.C. bureau chief, Arthur D. Postal, plenty busy in 2011. Here are his encapsulated reports on the quartet of congressional stories that mattered most this past year—and which will continue to be newsmakers in 2012.

Politicians, bureaucrats and industry associations kept our D.C. bureau chief, Arthur D. Postal, plenty busy in 2011. Here are his encapsulated reports on the quartet of congressional stories that mattered most this past year—and which will continue to be newsmakers in 2012.

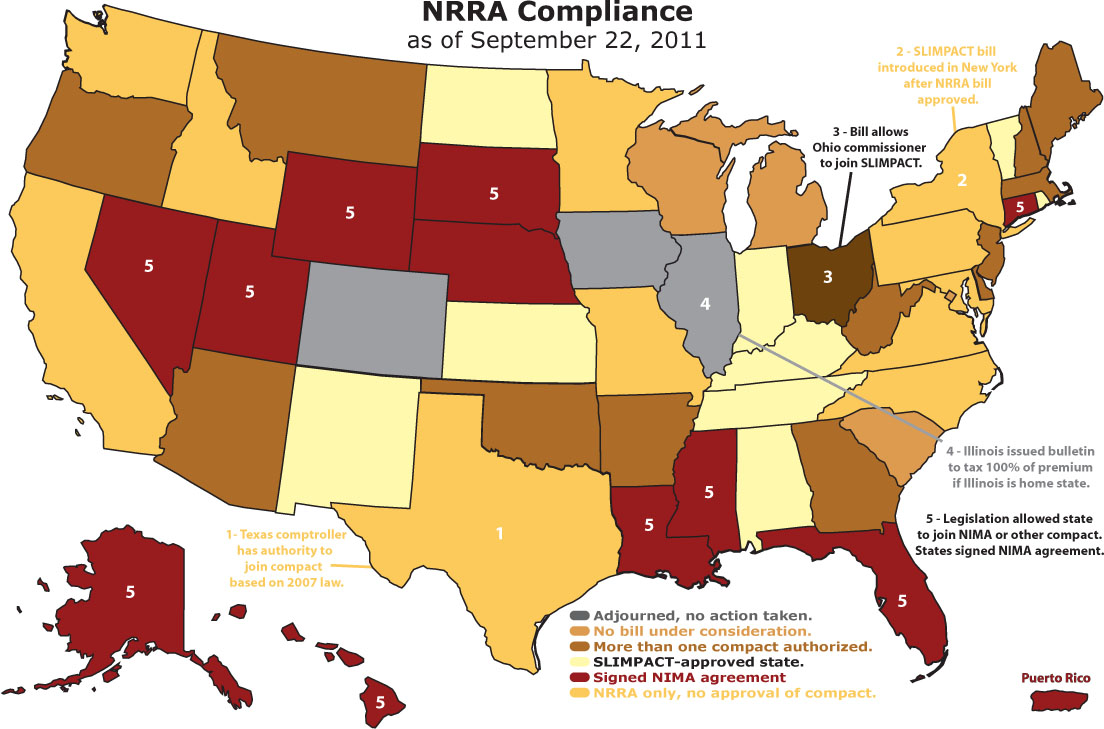

NRRA: Law to Modernize Surplus-Lines Regulation Hits Implementation Hurdles

In 2011, the insurance industry accomplished its goal of modernizing surplus-lines regulation when federal legislation—the Nonadmitted and Reinsurance Reform Act (NRRA)—went into effect July 22, establishing the insured's home state as the only one with jurisdiction over multistate surplus-lines transactions—and therefore the only one that can require a tax be paid by the broker.

But sizable roadblocks remain toward establishing a uniform system for disbursing premiums owed to states where the actual risk exists. While most of the industry would prefer the Kentucky allocation system, there is no consensus among the states about an allocation mechanism, nor any means of pressuring states toward adoption of a uniform system.

The how—and when—of NRRA implementation will remain a top story in 2012.

FIO—Dodd-Frank Offspring—Sparks Some Concern About Increasing Federal Oversight

In May, the Federal Insurance Office established under the Dodd-Frank Act (DFA) became operational, with Michael McRaith, the former insurance commissioner of Illinois, as its first director.

McRaith is in the process of forming a staff, which will provide information about the insurance industry to the Financial Stability Oversight Council and the Treasury secretary.He has also formed an advisory council of state insurance regulators and industry officials to advise him on various issues the industry is facing.

There are two key concerns to watch out for: One is how FIO and the entire Treasury Department works with the states, the Office of the U.S. Trade Representative and Congress on international solvency and reciprocal trade issues.

The second is the reaction of Congress and the states to FIO's pending report on how insurance regulation can be modernized and improved. The report is mandated by the DFA and is due in late January.

Any suggestion for a stronger federal role is likely to increase tension among states, state regulators and their supporters in Congress.

NFIP: Permanently Temporary?

The National Flood Insurance Program since Sept. 30, 2008 has been operating on a series of temporary reauthorizations of a law passed in 2003. In an attempt to find a more permanent solution, bills have been passed by the full House and the Senate Banking Committee extending the program until Sept. 30, 2016.

Both bills call for greater private-sector involvement in the program and fewer subsidies for a program already more than $18 billion in debt and with little likelihood that it can generate the revenues to repay it.

However, it's unclear when the Senate will take up the version passed by its banking panel in September. The Senate passed a short-term reauthorization until May 30, 2012, but the House has not acted on it yet as of this writing.

At press time, Congress had a Dec. 16 deadline to either pass a five-year extension or work out another short-term reauthorization.

House Republicans are also rolling a longer-term extension into a controversial bill that would extend some tax cuts and offset them with budget cuts, but industry observers are not optimistic the bill would get through the Senate. Additionally, President Obama has threatened to veto it.

Commission Mission: MLR Exemption

Insurance agents, both in property and casualty and life, are seeking an exemption of their commissions from the medical loss ratio (MLR) provision of the Patient Protection and Affordable Care Act. The Department of Health and Human Services, led by Kathleen Sebelius, has refused to provide such an exemption, and legislation has been pending in the House for six months without floor action.

Given that there is strong opposition to an exemption from the Democratic majority in the Senate, agents appear to face an uphill climb for relief, despite their pleas that they play a key role in the health-care process and that they have lost significant revenues as a result of the MLR provision.

{kind=link}

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.