Over two decades ago, when insurers first began using credit score formulas to underwrite personal auto and homeowners' coverage, the public backlash was palpable—and so was the ire of many independent insurance agents, who were forced to explain its use to customers.

Today, although still not universally embraced by independent agents, credit-based insurance scoring has come to be accepted and in many cases, respected by the same producers who once were vocal opponents.

Even the lackluster economy has failed to unseat its use. "All evidence is that insurance scores, because they're different from lending scores, have not spiked down the way that some people predicted because of the down economy," said David F. Snyder, AIA vice president and associate general counsel. "Instead, they have played a positive role in the market, providing most people with lower rates and supporting broad availability of coverage. "

Observers who track the issue cite increased use by insurers (from a "handful" 20 years ago to more than 90 percent today, according to AIA), consumer education, legislative safeguards, competitive insurance markets and favorable policy pricing as the primary drivers of the increasing acceptance of credit scoring.

"The critics are still out there, but markets are healthy, rates declining, and there's lots of competition—the major reason we're not seeing more effective opposition to any issues in auto now, including credit scoring," Snyder said. "Regulation on the issue of credit has been fairly balanced and we have a well-functioning market."

And in many cases, credit scoring has made life easier for agents, who recognize its usefulness in keeping premiums low and shifting many consumers away from assigned risk pools and into the standard market. "In 2002, my phone would ring off the hook all the time with agents saying they hated it," said Wes Bissett, senior vice president of government affairs, IIABA. "I haven't received such a call in several years."

A little history

Insurers began using credit scoring for personal lines auto and homeowners' insurance in the mid-1990s. In developing their formulas, insurers use either the consumer's Fair, Isaacs & Co. (FICO) three-digit credit score alone; an "insurance score" from FICO; or create their own proprietary score using FICO credit scores or FICO insurance scores and adding in their own underwriting criteria.

"In the old days, most companies had three rate levels: very good, average and bad. If you were bad, you often went into an assigned risk plan because the company was unsure of the risk exposure," Snyder said. "Credit scoring allows insurers to move to a rating system that has hundreds of variables combined in thousands of ways to more effectively align price to risk. This not only means more accurate pricing, but also gives companies the confidence to write every applicant who comes to them because they have a rate that matches the risk."

The new practice came under immediate attack from consumer groups, which claimed that credit scoring was discriminatory, objected to the sole use of credit scoring for placing new business and renewals and questioned the legitimacy of some of the studies cited by the insurance industry in support of the practice—including ones conducted by the University of Texas, the Michigan Office of Financial and Insurance Services, the Federal Trade commission and St. Ambrose University.

With the passage of the Fair and Accurate Credit Transaction Act in 2003, the federal government interceded. Under the act, the Federal Trade Commission (FTC) was mandated to study the credit scoring practices of the biggest homeowner and auto insurers and the impact on pricing and availability. The FTC's 2007 examination of credit scoring in auto insurance upheld the validity and impartiality of credit scoring as a legitimate tool in predicting risk. FTC is conducting a similar study on the impact of credit scoring on homeowners' insurance, which is due for release sometime this year.

Part of the problem was confusion between the variegated, proprietary, weighted systems unique to each insurer with straight-out financial credit scores as supplied by Equifax, Experian or TransUnion that financial institutions use in lending. Insurers argued that using credit scores actually made for more accurate underwriting and ultimately included more insurance buyers than the old system.

All the while, insurance agents were stuck in the middle of the firestorm, having to understand and explain the practice's rationale to confused customers—and many of them voiced their opposition to the practice to agent groups and insurers.

In recent years, however, much of the sting involving the use of credit scoring has been removed by state and federal regulations that have modified its use.

Impact of the NCOIL model

One of the primary turning points in the growing acceptance of credit scoring could be attributed to the National Conference of Insurance Legislators (NCOIL) model law, adopted in 2002 and amended most recently in 2009 to address the economic challenges of the recession.

In essence, the NCOIL model regulates the use of credit information for personal insurance to protect consumers. Among its basic provisions:

- Insurers can't use insurance scores calculated using income, gender, address, ZIP code, ethnic group or other personal information as a factor

- Insurers can't deny, cancel or non-renew coverage solely on the basis of credit information

- Insurers can't use only credit information in basing renewal rates

- Insurers can't take adverse action based on credit information without using a current credit score and without notifying the consumer

- Insurers can't consider an absence of credit information or an inability to calculate an insurance score in underwriting or rating insurance.

The 2009 amendments recognize the impact of the recession with the introduction of an "extraordinary life circumstances" provision. This requires insurers using credit information to provide "reasonable exceptions" to consumers whose credit information may have been directly influenced by a federal catastrophe, serious illness, death of a family member, divorce, identity theft, loss of employment resulting from involuntary termination for three months or more and military deployment overseas.

In the past, the National Assn. of Insurance Commissioners (NAIC) has conducted hearings on the topic, and the NAIC Consumer Liaison Committee has considered developing a model law regulating credit scoring vendors and "they continue to follow the issue," an NAIC spokesperson said. However, a proposed NAIC credit scoring data was opposed last year by insurer groups on the ground that the NCOIL model already adequately addresses the issue.

"We have worked closely with agent groups on the NCOIL model; they are familiar with it, it's being used carefully and subject to more regulation," Snyder said. "This doesn't mean everybody loves it, but it's a good example of innovation in a market that has benefited everyone."

The NCOIL model, along with other state regulations of credit use, have fine-tuned the practice and quieted many critics—including agents, Bissett said. "A decade ago, companies were using credit as the sole factor in underwriting; as a result of this regulation, that's no longer the case," he said. "We're in a different position than 10 years ago. I've talked to agents who were the biggest vocal opponents and even testified against credit scoring who have turned completely around. They see the benefits: that it allows them to be more competitive, write risks that before they might not have been able to write at all."

One of these is Randy Lanoix, owner of Lanoix Insurance Agency in Brusly, La., whose business has seen more people benefit from the use of credit scoring that any being adversely affected.

"When it first came into widespread use, a lot of people, including me, had concerns that it might not properly reflect insurance risk," he said. "But when you explain to people that if they have good credit it could lower their premiums, you don't get that much pushback. The better risks are paying less and those with more claims who in a lot of cases have low credit scores are paying more."

Each of his agency's companies has a different credit scoring model, and agents themselves don't see a customer's actual credit score; they simply enter the parameters and come back with a rate, Lanoix said.

Because his agency is located in a rural area, many of his customers don't have or don't use credit cards, and he was initially concerned that this would adversely affect their insurance scores. But the "no hit" issue is addressed in the NCOIL model defused that complaint.

Most of Lanoix's customers are on board with the practice. "When I tell some that they have to do a credit score, they don't want to, but you could count those on one hand."

States that ban

Although well-crafted regulations like the NCOIL model have helped tame opposition to credit scoring, they haven't eliminated it. In 2011, 23 states introduced more than 50 bills to ban or severely restrict insurers' use of credit scoring, said Neil Alldredge, senior vice president, state and policy affairs for NAMIC.

However, only two passed: in Nevada, where a bill establishing a set of extraordinary life events that applicants or policyholders can ask insurers for exception was enacted into law; and Montana, where the legislature included military deployment as an extraordinary event in underwriting or rating.

"Although some state legislators continue to introduce proposals to ban or restrict the use of this valuable underwriting tool, when educated, most legislators come to realize that insurance scoring benefits the vast majority of insurance consumers," he said.

To date, only four states have enacted outright ban on the practice:

- California—bans the use of credit information for both homeowners and auto

- Hawaii—bans the use of credit information for auto insurance

- Maryland—bans the use of credit information for homeowners and severely restricts its use for auto

- Massachusetts—bans the use of credit information for both homeowners and auto.

By the numbers

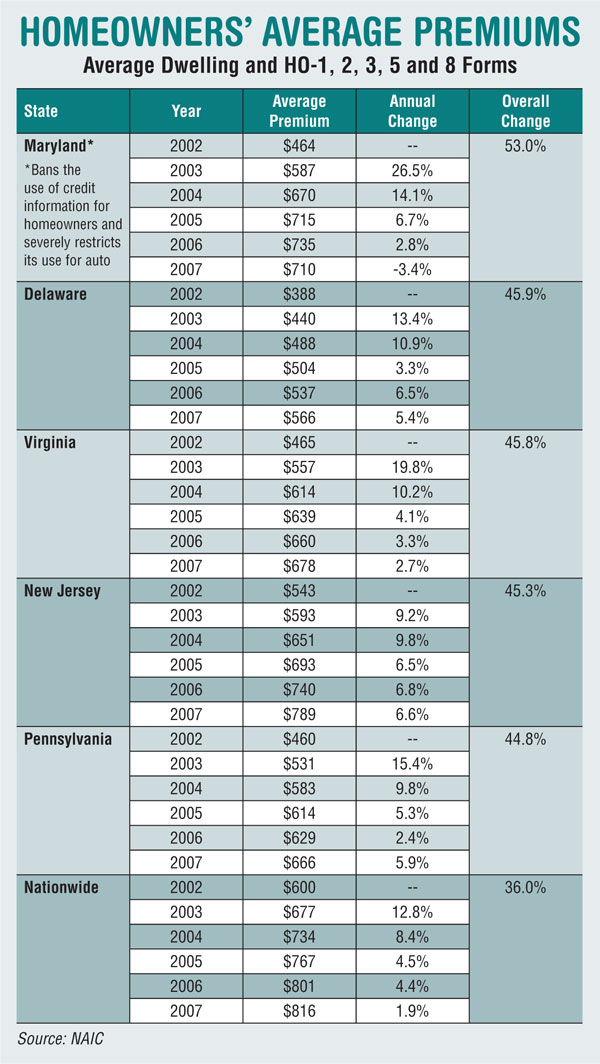

Even credit scoring's most vociferous critics can't dispute that pricing, availability and market competition are robust in the auto and homeowners area, even in the current bad economy. Conversely, states that ban credit have experienced rate increases (see chart). According to PCI, after Maryland introduced a ban in 2002, homeowners' insurance rates went up at a faster rate than the rest of the country (53 percent versus 36 percent) between 2002 and 2007, and at a faster rate than they did in neighboring states. At least one insurer stopped writing in Maryland because of the ban.

{kind=link}

However, when there is a legislative change, sometimes the market impact isn't felt until 5 or 10 years later, especially on homeowners, said Alex Hageli, personal lines manager at PCI. "Because there's not much policy turnover in homeowners, you don't get the full impact of a ban until the whole book of business in the state has been rewritten without any residual impact of credit information," he said.

Based on this evidence, you can make the case that credit scoring benefits consumers more than insurers, Snyder said. "We looked at loss ratios between Pennsylvania and California for auto liability, and they are virtually the same," he said. "I don't think the real benefit is increased profitability to the industry but the ability to price for accurately for risk, which means more companies can be in the market and more people can have choices and find coverage."

Continuing education

Credit score proponents still need to promote education among consumers, legislators and producers, and for the most part, insurers have made strides in training agents on the use of credit, Snyder believes. "Some companies have special numbers for agents to call if they have a person who doesn't fit or if there are unusual circumstances," he said.

However, although they're more accepting of credit scoring, some agents can still be a tough sell, Hageli said. "Opposition over the last one or two years has lessened, but there's still a lot of ambivalence about it," he said. "Sometimes I think we're making better progress with legislators than agents."

Still, the image of agents opposing credit scoring is a "residual concept…a lot has changed over the last 9 or 10 years," Bissett said. "Agents came around on credit because it provided more competition and enabled independent agencies to get more in the game, especially in the auto market, as they become more comfortable with pricing and underwriting. It's good for agents."

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.