Reinsurers have let it be known that the reinsurance market would be prepared to take on some flood risk if Congress decides to pursue that option.

The comments by Frank Nutter, president of the Reinsurance Association of America, and Brad Kading, president and executive director of the Association of Bermuda Insurers and Reinsurers, came amid news that Rep. Judy Biggert, R-Ill., chairwoman of the Insurance, Housing and Community Opportunity Subcommittee of the House Financial Services Committee, is planning to sponsor legislation reauthorizing the National Flood Insurance Program.

Industry officials who asked not to be named confirmed that Rep. Biggert has agreed to sponsor a bill similar to the one that passed the House in July 2010 reauthorizing the program for five years.

Industry officials who asked not to be named confirmed that Rep. Biggert has agreed to sponsor a bill similar to the one that passed the House in July 2010 reauthorizing the program for five years.

Last year's legislation, H.R. 5114, the "Flood Insurance Reform and Priorities Act of 2010," passed the House 329-90. It was sponsored by Rep. Maxine Waters, D-Calif.

The Senate did not take up that bill.

The new legislation includes provisions designed to phase in market rates and reduce instances where a homeowner submits multiple claims, and is not expected to include an amendment added on the floor in July that would require write-your-own insurers to agree that they will not use "anti-concurrent causation" language to exclude coverage of wind damage simply because there is also flood damage to the property.

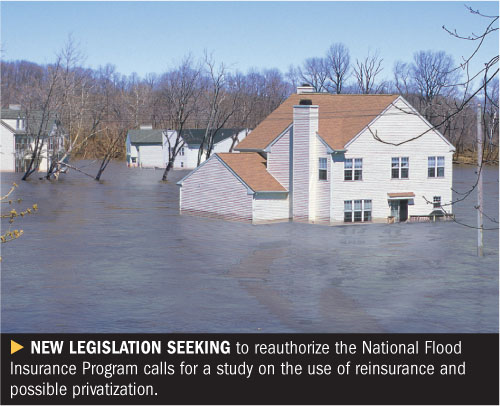

A provision in the draft legislation also calls for a study on the use of reinsurance and possible privatization of the NFIP.

Mr. Nutter said, "The RAA believes that the NFIP could address its volatility and extreme-event exposure and reduce the dependence of the program on taxpayers and federal debt through risk transfer to reinsurance from private-market capital providers."

Mr. Nutter also said the NFIP could use the reinsurance market to seek the placement of catastrophe bonds to supplement available reinsurance capacity.

"Both markets have significant excess capacity, and [I] believe that flood risk can be reinsured or transferred into capital markets," he said.

Mr. Kading noted that Congress is considering a range of options for the NFIP.

He acknowledged that there has been some pushback to proposals by offshore insurers to carve out part of the flood insurance risk but not to reinsure.

"Most of the industry trade groups have said they don't support privatization of direct writing of flood risk insurance," Mr. Kading said.

He said direct writing by offshore insurers would be "an experiment."

"We really can't agree to underwrite the risk until we look at FEMA data," Mr. Kading said. "We write flood risk elsewhere, we sell reinsurance on commercial flood risk in the U.S., and we sell direct insurance in other countries."

House To Consider Producer Licensing

Legislation that would provide agent-licensing standardization across state lines will be re-introduced in the House this week.

The bill, the National Association of Registered Agents and Brokers Reform Act (NARAB), has passed the House on voice vote twice within the last several years. It failed to win Senate support last March.

It will be sponsored by Rep. Randy Neugebauer, R-Tex., and Rep. David Scott, D-Ga.

In a statement, Rep. Neugebauer said, "This legislation will help reform and modernize a very important part of state insurance regulation: agent and broker licensing."

He added, "The legislation is straightforward: insurance agents and brokers who are licensed in good standing in their home states can apply for membership to [NARAB], which will allow them to operate in multiple states."

Disclosure that the bill will be re-introduced was made at the spring meeting of the National Conference of Insurance Legislators (NCOIL), held in Washington March 4-6.

Officials of both the Independent Insurance Agents and Brokers of America and the National Association of Professional Insurance Agents voiced support.

NARAB was originally established under the 1999 Gramm-Leach-Bliley Act to impose uniform regulation if a certain number of states did not agree to comply with its provisions. However, while the required number of states complied, large states that comprise most of the nation's population did not join, hindering the ability of agents to sell across state lines and rekindling interest in a federal law aimed at spurring licensing reciprocity.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.