As the insurance industry embraces the use of social media as a marketing tool, it must consider risks that are unique to the insurance industry. The degree of insurance regulation and the industry's reliance upon agency distribution channels combine to create special regulatory and legal risks for both insurance companies and agents.

If insurance companies and agents do not use Facebook and Twitter carefully, they may find themselves not only in violation of insurance laws, but also with an increased risk of errors and omissions claims. Insurance companies may find themselves responsible for the actions of their agents in both civil and regulatory arenas.

If insurance companies and agents do not use Facebook and Twitter carefully, they may find themselves not only in violation of insurance laws, but also with an increased risk of errors and omissions claims. Insurance companies may find themselves responsible for the actions of their agents in both civil and regulatory arenas.

State insurance regulators recently began discussions about social networking and regulatory compliance. At the winter meeting of the National Association of Insurance Commissioners, regulators held a meeting on the "Use of Social Networking Sites in Insurance," but no formal guidance has been issued.

Insurance regulators were similarly slow to react when the insurance industry began developing websites and advertising on the Internet. Back then, a few states promulgated specific regulations, others announced that existing advertising rules applied, and some took no action.

We can expect a similar response to the use of social networking.

Financial services regulators are ahead of insurance regulators. In January of this year, the Financial Industry Regulatory Authority (FINRA) issued Regulatory Notice 10-06. Although the notice leaves some technical questions unanswered, it provides a significant amount of guidance that is instructive in the insurance regulatory world.

For example, FINRA distinguishes static material from the interactive functions of social networking sites. According to FINRA, the static material on a Facebook page (profile, background and wall) is advertising and subject to prior approval. Interactive posts, however, are subject to different rules.

Whether insurance regulators will make the same distinction remains to be seen.

Under any definition of "advertising" in the insurance laws, the offering of services or products or statements made to promote interest in an insurance company or agent is advertising. Insurance companies and agents are using social networking in these ways but not necessarily in compliance with the insurance advertising laws.

Insurance advertising is highly regulated and regulators have cited insurance companies in market conduct examinations for non-compliant advertising practices and for failing to have procedures and controls over agent advertising.

ADVERTISING SCRUTINY

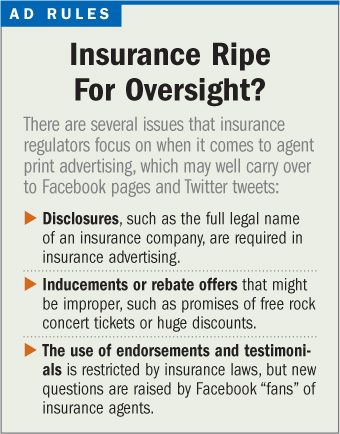

Disclosures are commonly required in insurance advertising yet often are absent on Facebook pages and in Twitter tweets. One common requirement is that the full legal name of the insurance company as well as the location of the home or principal office must be disclosed.

Some states require a disclaimer that products may not be available in all states and may require a listing of the states in which the insurer is licensed.

Some states require a disclaimer that products may not be available in all states and may require a listing of the states in which the insurer is licensed.

One state requires the license number to be displayed. Regulators have insisted that these disclosures be displayed directly or via a link on websites and are likely to insist the disclosures be used in social networking.

There are agents who make statements on Facebook and Twitter such as "Save up to 25 percent on all your insurance policies," or "I just saved Nancy $500 on her auto insurance." Sometimes, specific insurance companies are identified.

There are insurance laws that restrict the use of such statements, and an agent or insurance company always runs the risk that a competitor will contact the insurance department and challenge the accuracy of such statements.

The age-old question of what constitutes an improper inducement or rebate surfaces when an agent's Facebook page contains a posting that states, "We have free tix [sic] to 'Guns & Roses'!!!!!….first come, first serve…call Dave."

Another Facebook comment on an insurance agency page recently announced, "New programs for the week of Jan. 4, 2010!!! See what kinds of discounts I have for you."

If these offers would be improper inducements or rebate offers in print advertisement, they are probably improper inducements on a Facebook page or in a Twitter tweet.

The use of endorsements and testimonials in insurance advertising presents another compliance challenge. Insurance laws restrict the use or content of endorsements and testimonials, particularly for life insurance.

If a person posts a comment about an agent's status on Facebook, or "likes" something the agent does in his or her professional life or becomes a Facebook "fan," all other Facebook friends will know about it. Are those postings considered testimonials?

If a person posts a comment about an agent's status on Facebook, or "likes" something the agent does in his or her professional life or becomes a Facebook "fan," all other Facebook friends will know about it. Are those postings considered testimonials?

If an agent asks a customer to become a "fan" of the agent on Facebook, is that a testimonial? If the agent gives the person a gift for becoming a fan, it might be considered a "paid testimonial" for which an additional disclosure is required under the laws of many states.

These issues have not been addressed by regulators. One can hope that regulators will take a reasonable view of emerging social norms in the face of advertising regulations designed for other media.

INSURER RISKS

The failure of insurance agents to comply with advertising requirements presents a regulatory risk for insurance companies whose names or products are mentioned. Under the insurance laws of many states, particularly those applicable to life and health insurance, insurance companies must approve agent advertising before it is used. Even if approval is not required, insurance regulators will hold insurance companies responsible for the content of agent advertising when the advertising is on behalf of the insurer.

Mundane regulatory requirements like record retention requirements for insurance marketing and advertising records present special challenges for the quick-paced and ever-changing communications in social networking. It remains to be seen what records of social media advertising insurance regulators will expect the industry to maintain and whether a copy of every tweet on Twitter or comment on Facebook will have to be kept.

Apart from regulatory compliance concerns, however, insurance companies should be concerned about protecting their brand when their agents use Twitter or Facebook and hold themselves out as an agent of the company. Insurance companies already have guidelines in place for agent advertising. Those guidelines should specifically include the use of social networking and the associated challenges.

Insurers should also be concerned about social networking communications that may be considered consumer complaints. Regulators may consider tweets or posts to be consumer complaints and therefore subject to complaint handling regulations. This raises a question about whether the anonymity of a sender will be sufficient to exempt a communication.

Third-party postings should not be ignored. Agents and insurance companies should monitor the content of third-party postings whether on Twitter, a blog or a wall posting on Facebook.

FINRA indicated that forwarding a post and even responding to a post may constitute "adoption" of the contents of the post, thus making the firm responsible for the content. The same could hold true in the insurance world.

State insurance laws prohibit untrue, deceptive or misleading representations made about a person in the conduct of the person's insurance business. If a "fan" of an insurance agency or company posts a false or derogatory comment about another insurance company or agent, regulators could attribute that to the company or agent on whose page the statement appears.

This may be an area in which different rules for static information and interactive communications is warranted.

E&O RISKS

Insurance companies and agents must also be aware of potential errors and omissions exposures that may result from the use of social networking. These exposures are most likely to result from a failure to procure coverage, a failure to process a service request, or reliance upon incomplete or misleading information about a product.

One risk comes from the display of insurance information on social networking sites. General information that is provided for educational purposes is one thing, but statements that purport to explain the benefits of a particular product or the product of a particular insurance company could be relied upon by a consumer in deciding to purchase insurance.

A recent posting on an agent's Facebook page includes a promise that "there will be no premium increase if you have an at-fault accident." When a premium increases or a claim is not covered because promotional information did not disclose coverage exclusions, the agent may face an errors and omissions claim.

Courts generally decline to alter the terms of a policy when an agent has misrepresented coverage, but that will not prevent a consumer from asserting a claim or from including the insurance company in a lawsuit.

Social networking for insurance business should be used consistently or not at all. The failure to regularly monitor social networking sites may result in missing important communications coming from policyholders.

It does not take much to imagine a consumer using social networking to ask an agent to increase policy limits, bind coverage or add a car to a policy. Unless an agent is diligent about checking regularly for such communications, an agent may end up with an E&O claim for failing to procure insurance and the insurance company that issued the policy could be vicariously liable for the omission.

Social networking sites are not private. Allowing consumers to use social networking sites to submit information related to insurance transactions should also raise privacy and data security concerns.

If a consumer submits personal information to an insurance company or agent in conjunction with an insurance transaction, does the company or agent have a duty to limit public access to that information? How is the security of that data protected when the company or the agent is not the host of the site?

It may turn out that in those situations the consumer will be deemed to have voluntarily released his or her information to a public site with no expectation of privacy, but this has yet to be determined by regulators.

As the insurance industry's use of social networking increases, insurance companies and agents need to be cognizant of the compliance and legal risks. Mitigation of those risks begins with treating social networking as a formal business communication.

Susan T. Stead is a partner and vice chair of the Insurance Regulatory and Transactional Practice Group at Nelson Levine de Luca & Horst, a national law firm focused on the insurance industry. She may be reached at the firm's Columbus, Ohio office at sstead@nldhlaw.com.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.