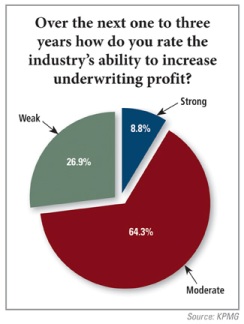

At KPMG's insurance conference held in late September, attendees were surveyed on various issues facing the industry, including their views on underwriting profitability. The lack of confidence in their ability to underwrite profitably was striking (see accompanying chart).

“I think it reflects the fact the soft cycle that people are experiencing is being driven by factors that aren't in most people's experience,” says Scott Marcello, the leader of KPMG's insurance practice in the U.S.

Among the factors insurers dealt with this year are depleted capital because of high catastrophe losses in 2008; higher 2009 reinsurance renewal rates; investment portfolios losses; and declining prices in recent years.

“You add all that up and you would think the market would be turning,” says Marcello. “All the fundamentals we've seen in the past would suggest there would be a shift to more favorable pricing, but then you add the macro-economic issues that have contributed to holding prices down and are affecting the profitability of companies.”

So, Marcello believes, insurers have had to come to grips with the fact there are broader economic issues in play and companies are concerned about their financial well-being to the point they are not willing to chase higher prices.

“If we were not in the economic environment we've been in for this long period of time, people would say the market is going to turn and underwriting profitability will shoot back up. But I think [insurers] in this marketplace are wondering how fast the economy will recover,” says Marcello. “What are they going to do to make sure they are [achieving] growth, and will [growth] be conducive with increasing underwriting profits?”

The KPMG survey also showed there is a mixed bag of areas insurers see as being important to future growth. The carriers were asked to consider factors such as underwriting, technology, customer focus, product innovation, distribution, mergers and acquisitions, international expansion, and redeploying capital–yet none of those options garnered more than 17 percent (product innovation) nor less than 7.5 percent (M&A) among the insurers surveyed.

“It does reflect there are a lot of different opinions as to what is important for growth,” says Marcello. “But even more important, based on what I know about some of the players in the industry, I think this links up with both their strategic imperative and what they view their current position to be.”

Some companies, according to Marcello, would say they've grossly underinvested in technology over the last several years. If a big part of their growth strategy is to get closer to their customers and the biggest barrier to that goal is technology, they have to fix that issue.

Other companies have made those technology leaps and feel closer to their customer from a technology standpoint but are saying they still haven't figured out all their customer habits and need a better read on those habits, adds Marcello.

“What you are seeing is companies are in a lot of different places today in terms of their maturity in [various] areas of the business, and I think you are going to see a differentiation of strategies as people come out of this market,” he says. “[Companies] have had to scale down people and get back to the core of their business. They are going to have to make some important decisions about what they want to focus on. What you are seeing is a different view, depending on where they view themselves positioned and what they think will be the most important things in the marketplace going forward.”

From his conversations with insurers, Marcello contends the industry recognizes there are a number of places where it underinvested in technology for an extended period of time. As a result, insurers have multiple disparate system capabilities, not all of which are linked together.

“Insurers have a difficulty in seeing the world, in many cases, through a customer lens as opposed to their different products and capabilities,” says Marcello. “You could have a company that [communicates] to the same customer from different parts of the enterprise but may not have a clear vision of how that all comes together and how profitable that is.”

Marcello is seeing a significant desire among insurers to achieve future growth and profitability through a better understanding of their customers, streamlining their finance capabilities so they can analyze their performance faster, and operating with fewer manual interventions to the extent they can do more with less.

“I am seeing a growing recognition among the companies I talk to that there is a need for significant [technology] investment,” he sums up.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.