In recent years, the specialty market for solo practitioner and small group lawyers professional liability–LPL–insurance has posted strong and stable financial results. However, the operating results of these companies were hurt in 2008 by higher claims expense and lower investment returns.

Reduced expectations for future investment returns and the possible increase in claim costs due to the broader economic slowdown will pressure the future operating results for this market.

Additionally, premium growth in this specialized sector has been flat for the last four years. Softer rate levels in recent years may put upward pressure on both the loss ratios and underwriting expense ratios of these companies.

Additionally, premium growth in this specialized sector has been flat for the last four years. Softer rate levels in recent years may put upward pressure on both the loss ratios and underwriting expense ratios of these companies.

This article highlights the recent financial results for a group of sixteen companies that specialize in providing LPL insurance coverage. Collectively, these companies had about $440 million of surplus at year-end 2008 supporting approximately $280 million of gross written premium.

Using annual statement data from Highline Data (a data affiliate of National Underwriter), we reviewed key financial metrics for these LPL specialty companies. The results show the overall financial health of this group is very strong, but also suggest pressures on future profitability. Specifically, we have reviewed the top-line premium growth, operating results and capitalization level of this composite.

TOP-LINE PREMIUM GROWTH

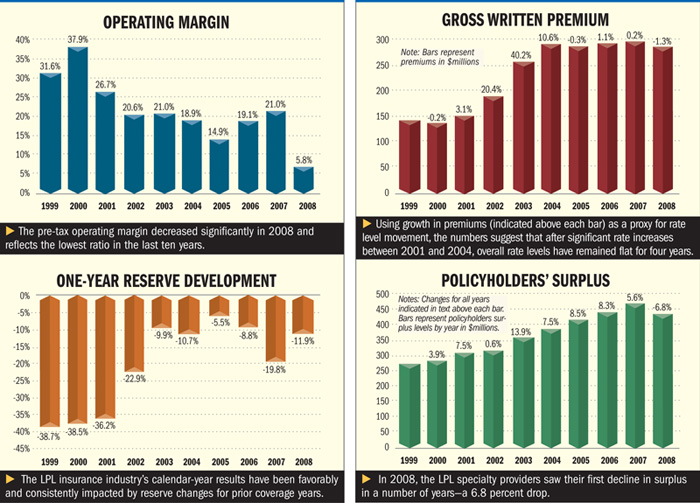

The accompanying bar graph displays the growth in gross written premiums between 1999 and 2008 for this composite of LPL coverage specialty writers.

{kind=link}

Using growth in premiums as a proxy for rate level movement, the chart would suggest that after significant rate increases between 2001 and 2004, when several states experienced a fair amount of market disruption, overall rate levels have remained flat for four years.

It should be noted that although, in general, significant rate increases were seen between 2001 and 2004, a portion of the growth in premium for this composite stems from increased market share for several of the companies in our composite.

OPERATING RESULTS

As a second graph of operating margins between 1999 and 2008 shows, the LPL specialty insurance market has enjoyed strong profitability over an extended period of time. However, the pre-tax operating margin decreased significantly in 2008 and reflects the lowest ratio in the last ten years.

To explore what is driving these results, we reviewed the major components of the operating results–loss and loss adjustment expense costs, underwriting expense costs, and investment returns. The results presented are net of ceded reinsurance.

• Loss and loss adjustment expense ratios

The largest component of the operating results is the loss and loss adjustment expense (LAE) provision. After several years of fairly consistent claim costs, with an average loss and LAE ratio of 68.8 for the five-year period ended 2007, the composite showed a significant jump in 2008. The loss and LAE ratio climbed nearly 11 points to 79.8 in 2008, compared to 69.2 in 2007.

Calendar-year loss and LAE ratios are influenced by changes in loss reserve estimates for coverage provided in prior years. The one-year development chart, displaying yearly loss reserve developments relative to net earned premium for the composite, reveals that the industry's calendar-year results have been favorably and consistently impacted by reserve changes for prior coverage years.

• Underwriting expense ratios

The underwriting expense ratio of these companies has been stable for a number of years with only a minimal uptick–from 22.8 to 23.9–in 2008. This is most likely the product of fixed overhead expenses relative to a slightly lower premium volume, which is at least somewhat a result of the softer rate environment.

• Investment gains

The investment gain ratio for 2008 was the lowest in recent history for this LPL composite as well as the broader p&c industry. The lower return in 2008 reflects the broader economic and investment climate of late. Furthermore, with U.S. Treasury yields at their lowest level in history, insurance companies will probably have to get by with lower returns for a number of years to come as they try to determine where to invest this year's premium and investment returns.

CAPITALIZATION LEVELS

In 2008, the LPL specialty providers saw their first decline in surplus in a number of years–a 6.8 percent drop. This was primarily driven by unrealized capital losses and asset impairments that impact the policyholders surplus but are not accounted for in the operating margin.

However, as a whole the composite continues to be well capitalized, as reflected in the risk-based capital (RBC) ratio promulgated by the National Association of Insurance Commissioners (NAIC).

RBC is the theoretical minimum amount of capital needed, from a regulatory perspective, to absorb the various risks involved in an insurance operation. In essence, the NAIC model compares one-half of the required capital produced by the model to the company's statutory surplus in determining the RBC ratio. An RBC ratio of less than 200 percent triggers various levels of regulatory action; a ratio above 200 percent results in no regulatory action, all else equal.

The composite RBC ratio for the sample of specialty companies has been 750 percent or higher for the entire 10-year period we reviewed, with 2008 coming in at 755.9 percent.

Our review of the key financial metrics for LPL specialty companies suggests the overall financial health of this group remains strong. Going forward, however, these companies may face a number of challenges.

First, softer rate levels in recent years will continue to pressure both the loss ratio and underwriting expense ratio. Second, lower investment income yields will also put pressure on the operating results for all insurance carriers.

In addition, a third factor is the economic slowdown, which may lead to an increase in the frequency and possibly severity of claims, particularly in certain areas of practice. For example, the surge in complicated bankruptcy filings could become more prone to error as they are handled by overworked or less experienced attorneys.

In order for this niche market to continue to produce superior financial results, increased attention will need to be placed on the ratemaking and underwriting processes to ensure rates appropriately reflect higher costs and reduced investment return expectations.

Charles W. Mitchell, FCAS, MAAA is an actuary for Milliman in Milwaukee, Wisc. He may be reached at chuck.mitchell@milliman.com. Chad C. Karls, FCAS, MAAA, is a principal and consulting actuary for Milliman in Milwaukee. He may be reached at chad.karls@milliman.com.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.