New York City

Maurice R. Greenberg spent last week on the witness stand sparring with the attorney for American International Group over competing claims to AIG stock held by Starr International Company that had allegedly been ticketed as bonus compensation for top company employees.

Mr. Greenberg, former chair and chief executive officer of AIG, was forced out in 2005 following an accounting scandal involving the misuse of finite reinsurance to artificially boost the company's balance sheet. However, he remained chair of AIG's affiliated company–SICO–which holds a large block of AIG stock that the company is suing to have returned.

Mr. Greenberg, former chair and chief executive officer of AIG, was forced out in 2005 following an accounting scandal involving the misuse of finite reinsurance to artificially boost the company's balance sheet. However, he remained chair of AIG's affiliated company–SICO–which holds a large block of AIG stock that the company is suing to have returned.

SICO split from AIG shortly after Mr. Greenberg left the conglomerate.

Some of the stock held by SICO had been placed in trust to fund bonuses in a deferred compensation program for top AIG employees–a program that was ended when SICO split from AIG.

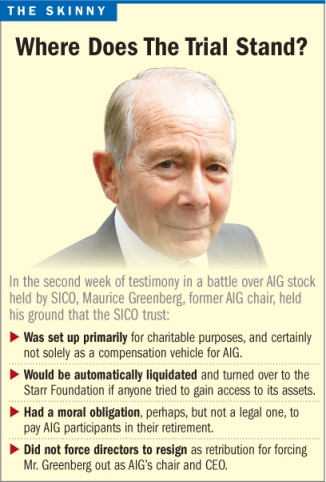

During questioning in U.S. District Court in Manhattan, AIG attorney Theodore Wells sought to cast doubt over Mr. Greenberg's assertion that if anyone tried to gain access to the assets of SICO's trust–consisting primarily of AIG stock–it would automatically be liquidated and turned over to the Starr Foundation.

In the case being heard by Judge Jed S. Rakoff, AIG is alleging that SICO is guilty of breach of trust in its handling of the shares used for deferred compensation.

The suit also seeks to force SICO to transfer the AIG shares it holds back to AIG, which were worth a total of $4.3 billion in 2005 when the deferred compensation program with AIG was severed by SICO.

At issue is whether the trust was set up for the benefit of AIG or, as Mr. Greenberg contends, for charitable purposes.

The pace of the questioning picked up after Judge Rakoff put both Mr. Wells and SICO attorney David Boies on the clock in an effort to complete Mr. Greenberg's testimony and keep the trial moving.

Earlier in the proceedings, Mr. Wells had asked Mr. Greenberg to find language in any documents to substantiate his claims concerning the protection of the trust. Mr. Greenberg said he believed the document that protected the trust was the "Deed of Trust" from the 1970s.

He cited one section that said should the SICO trust be found to be "frustrated, by a court of competent jurisdiction, then the entire trust fund shall be transferred unconditionally to the [charitable] Starr Foundation Inc."

However, Mr. Wells argued that the language does not imply any automatic condition of liquidation and award to the Starr Foundation.

His remarks at one point provoked Mr. Greenberg to respond: "I disagree with that comment one hundred percent."

"If someone was killed, all the others knew what [to do with the trust]," according to Mr. Greenberg.

Mr. Wells also introduced a memo from one of the founding shareholders, Ernie Stemple, from 1989 that raised questions about whether "the triggering mechanism" could be counted on in the future to move the trust into the Starr Foundation.

But Mr. Greenberg would not relent in his assertion that the trust was always intended for charitable causes.

At one point in the trial, to accommodate a scheduling problem, Carla A. Hills, who served on the board of directors and the audit committee of AIG from 1993 to 2006, testified on behalf of SICO. She said that AIG was considering expensing the SICO deferred compensation program in 2005, something Mr. Greenberg opposed, and may have ended the awards at that time.

She also revealed that a succession plan had been discussed, and Martin Sullivan was chosen to replace Mr. Greenberg when he retired. Mr. Sullivan took over as CEO at AIG when Mr. Greenberg left in 2005.

In his testimony, Mr. Greenberg refused to acknowledge the SICO trust had a legal obligation to AIG employees. He said SICO's only obligation was a moral one, not a legal one, to pay participants in their retirement.

On the third day of questioning by Mr. Wells, Mr. Greenberg dismissed assertions that there was a definite legal requirement for SICO to provide deferred compensation to AIG employees after the companies severed ties with one another. "I don't know whether there was a legal obligation or not," he said. "We would honor what we feel is a moral obligation to pay."

The response came as Mr. Wells continued to hammer at Mr. Greenberg over what he continued to suggest were the legal connections developed through a long relationship between SICO and AIG.

Mr. Wells exhibited a letter to AIG employees participating in the SICO program issued in April 2005–almost two weeks after Mr. Greenberg left the company and the bonus program ceased.

The letter told participants that contrary to rumors, those shares already promised to them prior to the severing of the relationship with AIG would be paid to them. Mr. Wells focused on a portion which stated SICO considered its obligation to pay the bonuses "a sacrosanct commitment that we will honor above all other obligations."

Despite Mr. Wells' insistence that the letter alluded to a legal obligation, Mr. Greenberg steadily denied that assertion, testifying that SICO's payment of the claims to participants would be honored because SICO made a promise to them.

Since the separation from AIG, Mr. Greenberg said SICO has expanded so it does not rely on the profitability of AIG stock. The firm has set up a managing general agency writing on paper provided by Berkshire Hathaway, with a business concentration in Asia and China.

The company has also sought other capital investments, invested in real estate and created other insurance companies–all of which was the founding intent of SICO, according to Mr. Greenberg. "We are satisfied with the progress we have made today," he said.

Mr. Wells concluded his questioning of Mr. Greenberg by playing an interview from 1995 with an author, Walter Guzzardi, who was researching a book and discussed SICO and its relationship with AIG.

In the interview, Mr. Greenberg repeated what he had said on a number of occasions–that the program was created to provide incentives for AIG employees, and called it a unique program that no other company had ever done.

That afternoon session saw a more relaxed Mr. Greenberg as his attorney, David Boies, began his examination.

Questioning Mr. Greenberg, Mr. Boies had the 84-year-old insurance executive detail his career in the Army during World War II and the Korean War, where he won a Bronze Star, as well as his start in the insurance industry after leaving the service, joining C.V. Starr Company in 1960.

Mr. Boies went over the complicated development of SICO and AIG through various mergers and acquisitions after Mr. Greenberg took over the company in 1969, a few years after the death of founder C.V. Starr. His introduction of a series of documents sparked a variety of objections from Mr. Wells, which led to lengthy legal arguments and conferences between attorneys and the judge.

Mr. Boies said there was no written record that SICO was created for the express purpose of benefiting AIG or was intended to be a compensation vehicle for employees.

Despite this, "there was no misunderstanding on the purposes and goal of the objectives of what the intent [of SICO] was," Mr. Greenberg testified.

Indeed, looking at documents that established SICO, Mr. Greenberg testified they contained nothing to show that it was created to benefit AIG.

The companies have their roots in C.V. Starr Insurance Company, for which Mr. Greenberg became the CEO in the late 1960s. Eventually, two groups of companies were formed–C.V. Starr and SICO, which were private companies, and a group of publicly held insurance companies that would eventually be brought together as AIG.

As part of the evidence he introduced, Mr. Boies presented the 1970 contract establishing AIG and what would become SICO. Mr. Greenberg, smiling, remarked that it was "a very valuable old document."

Using the reorganization and other documents of acquisition, Mr. Boies laid out a relationship between SICO and AIG where Mr. Greenberg testified that there was nothing in the language of any documents establishing that SICO (originally called American International Underwriters Overseas) was set up for the benefit of AIG.

SICO, said Mr. Greenberg, was established primarily as a trust in Bermuda that was ultimately intended to benefit a charitable organization, The Starr Foundation. However, it was also a business vehicle designed to make investments and create other companies.

According to Mr. Greenberg, it was at the discretion of the voting shareholders of SICO that a small portion of the profits from the company would be used as a deferred compensation program for outstanding AIG employees. The idea was to provide an incentive to AIG employees to remain with the company until their retirement in order to receive the rewards.

Earlier in the week, Mr. Wells produced copies of speeches, an interview Mr. Greenberg gave and correspondence in which he had touted the merits of the bonus program.

It was revealed that on one occasion, in 2004, there was discussion of a PricewaterhouseCoopers report that contemplated the merger between SICO and AIG. Mr. Greenberg said he opposed the plan primarily because doing so would cost SICO $78 million annually. No action was taken to merge the two.

The trust, Mr. Greenberg said, would eventually be dissolved and turned over to the Starr Foundation or other charitable organizations. Only the trustee of the charitable trust could change the designee, he said, assuring no future generation of SICO directors could change its intent. The trust, he insisted, was never contemplated to become the property of AIG.

Mr. Boies turned to the issue of AIG's directors who Mr. Wells contended were forced to leave SICO so that Mr. Greenberg and his associates would have total control of the trust after he left AIG.

Mr. Wells established that nine AIG executives–including Martin Sullivan–were removed as directors of SICO on March 28, 2005, the same day Mr. Greenberg left AIG. Mr. Wells contended the action was taken as retribution, while Mr. Greenberg said the move was because a hostile relationship had developed between AIG and SICO.

Mr. Boies produced letters of resignation dated April 4 and 5, 2005, from Mr. Sullivan and nine other AIG executives who were board members of C.V. Starr Insurance Company. Three AIG executives remained as directors on the SICO board until resigning on April 14 and 15, 2005.

Mr. Greenberg said he had conversations with a few of the executives he called "friends and colleagues," who said they had no choice but to resign. "They said AIG was going its own way," according to Mr. Greenberg. "They were all told to resign."

The trial is expected to continue into mid-July.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.