At a time when greater transparency in financial services is called for and many are suffering from the collapse of financial institutions and other key sectors through no fault of their own, the insurance industry seems committed to greater opacity, and indeed, compounding the hardship of working families.

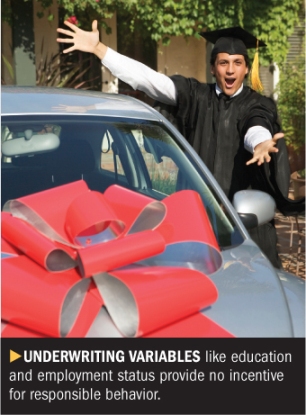

The advent of education and employment status as underwriting criteria for property insurance, particularly automobile, is just the latest manifestation. This "innovation" by the industry also undercuts a core underwriting objective.

Use of education and employment in the underwriting of property insurance undermines a key function of insurance–discouraging irresponsible behavior and incentivizing responsible loss prevention. It also exercises an adverse disparate impact on racial minorities, despite protestations to the contrary by some within the industry. Consequently, some of the most vulnerable segments of the population are hurt.

The issue is NOT whether risk or cost-based pricing and underwriting tools should be utilized.

Robert Hartwig of the Insurance Information Institute appropriately asserted in testimony before the Florida Office of Insurance Regulation in February 2007: "Society also benefits from risk or cost-based pricing. High auto insurance premiums offer poor drivers a significant financial incentive to improve their driving behavior, thereby reducing accidents, injuries and fatalities. These are socially desirable outcomes whose benefits are diminished when restrictions on actuarially valid underwriting criteria result in premiums that are less than accurate messengers of risk."

In other words, he said, "when the message itself is statutorily redacted–in some way blurred, garbled or lost–the consequences for society are unambiguously negative because the incentive to improve driving behavior is diminished."

But statistical correlation is only one part of sound underwriting. If the variable associated with loss has no intuitive relationship to the actual cause of loss, particularly if that variable is something over which the insured has no control, then there is no incentive for responsible behavior.

In fact, just the opposite might be the case. If a driver believes his or her rates will be determined, even just in part, by education, occupation, credit score, or some other factor that has no common sense relationship to the cause of loss–and is something they cannot readily control anyway–no additional positive incentive is provided.

It is precisely the use of such factors that sends a blurred, garbled and perhaps lost message to most policyholders.

Use of such criteria is particularly problematic in the current economy, with many people losing their jobs. Now in addition to losing their income, health insurance and often their very sense of identity, they will also suffer the indignity of higher property insurance premiums.

Does the industry really want to be viewed as piling onto vulnerable populations, particularly at a time when they are most vulnerable?

There are racial implications as well. Even assuming education and occupation predict loss, there cannot help but be an adverse disparate impact. In 2007 among people 25 or older, 28 percent of whites were college graduates compared to 17 percent of blacks and 12 percent of Hispanics. And any other education level or occupational index will yield a similar pattern.

This current debate reflects longstanding controversy over the question of race, ethnicity and socio-economic status in the pricing, underwriting and marketing of property insurance. It is long past time for the industry to provide a level of transparency that the mortgage lending industry has provided for more than 30 years.

Insurers should be required to publicly disclose the race, gender and income of applicants and the disposition (such as approved or denied) of those applications. Given the importance of location in most underwriting schemes–and the close association between race and place as well as poverty and place–the geographic location of where insurers are writing, renewing, nonrenewing and cancelling policies should also be disclosed.

Through the Home Mortgage Disclosure Act mortgage lenders have been doing this for decades without revealing the identity of any individuals or families or any trade secrets of any lender. Confidentiality has been maintained. And it has worked.

Douglas Duncan, senior vice president for research and business development and chief economist with the Mortgage Bankers Association, recently told the House Subcommittee on Financial Institutions and Consumer Credit: "MBA uses HMDA data to assist its members in analyzing the industry's performance in serving the nation and identifying new markets and investment opportunities…The data fairly present a picture of the industry's work, offering information to further effective investment and, where appropriate, provide flags for further regulatory review."

Federal Reserve Board Governor Mark Olson told that same subcommittee: "The data prompt discussion, investigation, analysis and research that may deepen our understanding of why these patterns occur and allow us to increase fairness and efficiency in the home loan market."

Loss costs, of course, are central determinants of the pricing and underwriting of insurance. Loss information should also be publicly disclosed so it is clear for all to see why insurance availability and pricing take the patterns that they do.

Simply asserting that risk, and risk alone, accounts for the pricing and underwriting of insurance is not sufficient.

It is time for the property insurance industry to finally step out of the shadow and let the sun shine in.

Gregory D. Squires is a professor of sociology and public policy and public administration at George Washington University.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.