NU Online News Service, June 13, 1:57 p.m. EDT

While the reinsurance sector contended with one of its biggest loss years ever in 2011, capital levels remain strong, 2012 has started off on a better note than last year, and quoting volatility for Florida renewals appears to be moderating compared to 2011's quoting behavior, recent reports say.

A June 5 report by Standard & Poor's states that severe catastrophes have challenged the reinsurance sector for the past 10 years, but reinsurers have maintained strong capitalization. S&P says reinsurers' enterprise risk management capabilities have provided the foundation for the sector's strong footing. “Careful risk selection has also enabled reinsurers to manage the soft cycle well, and contain the record catastrophe losses seen in un-modeled areas in 2011.”

A June Guy Carpenter briefing on reinsurance notes that despite the 2011 losses, the reinsurance sector ended the year with a dedicated capital position that was slightly up, at around $178 billion.

Due to reinsurers' ERM capabilities and conservative investment strategies, S&P says the 2011 losses amounted to an “earnings event rather than a capital event.”

That earnings event led to a net loss of $100.6 million in 2011's first quarter alone for a group of 19 U.S. reinsurers that comprise the Reinsurance Association of America. But RAA companies have, as a whole, reversed their fortunes in 2012's first quarter thanks to fewer catastrophes, according to results released by the association. The companies posted a combined net income of $1.5 billion for the first three months of this year. The group's combined ratio dropped from 129.3 in the first three months of 2011 to 95.6 this year.

Regarding reinsurance pricing trends, S&P says the sector has seen rate increases, but not to the point to declare that a hard market has arrived. S&P says the increases have “disproportionately favored the property segment in general, specifically the regions that experienced severe catastrophe losses during 2011.”

S&P says catastrophe-exposed areas that did not see losses in 2011 have seen rate increases of around 5 percent to 10 percent. But areas that experienced losses have seen “substantially higher rate increases and tighter terms and conditions, although these vary greatly by region.”

Guy Carpenter, though, notes that although January 2012 renewals showed global property-catastrophe rates up by 9.5 percent, reflecting 2011 losses, benign cat activity to start 2012 has led to an improving capital position that is “likely to contain any attempt at price increases throughout the year.”

Concentrating on Florida reinsurance renewals for June, Guy Carpenter adds, “The more significant Florida renewal price increases indicated by some in the industry earlier this year did not materialize, although pricing was up slightly on average.”

This does not mean that pricing in Florida is inadequate though. Speaking to PC360, Lara Mowery, head of global property specialty for Guy Carpenter, says, “Florida has been well priced. You don't see the diversification benefit and the degree of softening in the pricing that you've seen in some other global catastrophe zones.”

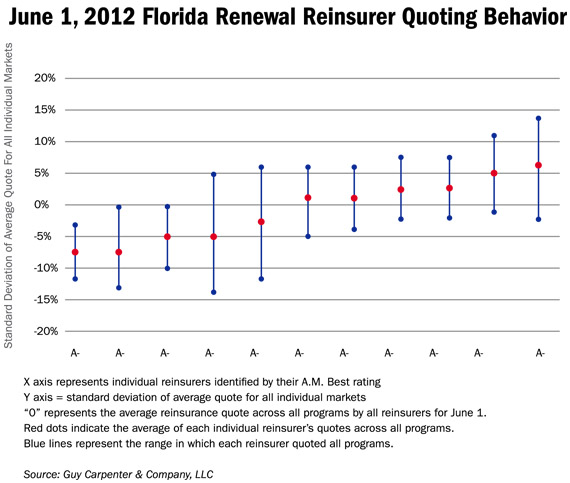

Furthermore, a Guy Carpenter analysis of quoting behavior for 11 reinsurers rated between A- and A+ by A.M. Best shows that quoting volatility has moderated for the June 2012 renewals compared to 2011, indicating a more tailored approach by many reinsurers to each individual renewal (see chart).

“In 2009 and 2010, variation from the average quote for Florida renewals was consistently within a range of down-3 percent to up-3 percent from the average,” Guy Carpenter says. In 2011, that volatility increased five-fold. Guy Carpenter says the volatility in 2011 was due to reinsurers being forced to respond in a very shortened timeframe to conditions impacting their view of risk and capacity deployment tolerance.

For the June 2012 renewals, the range in quotes has moderated to down-7 percent to up-6 percent from the average, Guy Carpenter says.

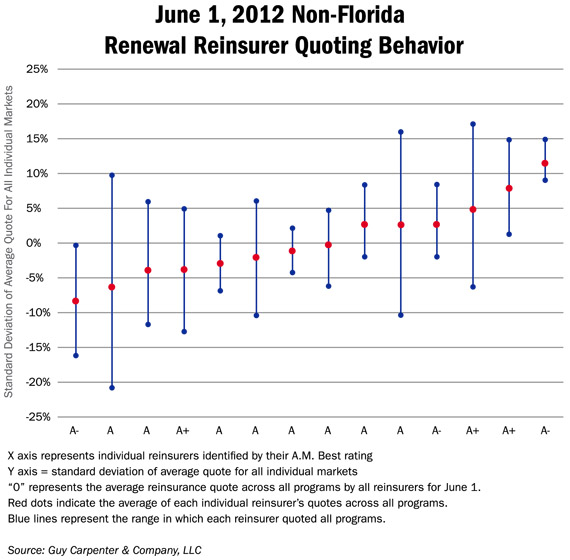

Interestingly, the moderation seen in the Florida renewals has not translated to non-florida renewals, where reinsurers' quotes ranged from down-8 percent to up-12 percent from the average renewal quote (see chart at bottom of page). Guy Carpenter says the volatility in non-Florida renewals likely reflects the difference in reinsurer appetites across a group of renewals exposed to a broader geographic base and diverse business focuses. “The change in pricing on these renewals was heavily dependent on the particular circumstances of the individual account and showed a wide degree of variation,” Guy Carpenter notes.

Mowery says the pricing trends for non-Florida renewals are not toward a hard or soft market, but rather a trend to more individualization.

Looking ahead, S&P says it expects some reinsurers to limit their exposure to regions that experienced heavy losses in 2011, particularly in Asia-Pacific regions where cat models do not adequately reflect exposures.

S&P notes that reinsurers have also shown interest in non-cat-exposed short-tail classes of business, such as accident and health, crop and surety insurance. “As a result, we could see some margin compression in those classes of business due to increasing competition,” the ratings agency says.

Additionally, while the reinsurance sector as a whole remains well capitalized, S&P says not all reinsurers exhibit the same level of surplus capital, and the ratings agency says it expects there will be “clear winners and losers from both an earnings and capital perspective.

Additional reporting by Mark E. Ruquet

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.